Estratégia de Trailing Stop com Duas Médias Móveis

Visão Geral

Esta estratégia calcula duas médias móveis com parâmetros diferentes, gerando um sinal de compra quando a média rápida cruza acima da média lenta. Simultaneamente, utiliza o Average True Range (ATR) para calcular um nível de stop loss trailing, e quando o preço cai abaixo desse nível, gera um sinal de venda. A estratégia consegue acompanhar eficazmente a tendência do mercado, realizando o stop loss assim que ocorre lucro.

Princípio da Estratégia

- Média Móvel Rápida (EMA): Média Móvel Exponencial de 12 períodos, que responde rapidamente às mudanças de preço.

- Média Móvel Lenta (SMA): Média Móvel Simples de 45 períodos, que representa a tendência de médio a longo prazo.

- Quando a média móvel rápida cruza acima da média móvel lenta, gera-se um sinal de compra.

- Calcula-se o Average True Range (ATR) de 15 períodos como base para o stop loss.

- Define-se a amplitude do stop loss trailing com base no valor do ATR (por exemplo, 6 vezes o ATR) e atualiza-se o nível de stop loss em tempo real.

- Quando o preço cai abaixo do nível de stop loss, gera-se um sinal de venda.

Esta estratégia combina as vantagens do acompanhamento de tendência e da gestão de stop loss, podendo tanto seguir a direção de médio a longo prazo quanto controlar as perdas individuais através do stop loss.

Análise de Vantagens

- A combinação de médias móveis pode identificar efetivamente a tendência, aumentando a confiabilidade dos sinais.

- O stop loss trailing dinâmico permite realizar o stop loss a tempo, evitando prejuízos ao capital.

- A utilização do ATR para o stop loss torna os níveis razoáveis, evitando excessiva sensibilidade.

- A lógica da estratégia é clara e fácil de entender, com parâmetros ajustáveis de forma flexível.

Análise de Riscos

- As médias móveis apresentam atraso, podendo perder oportunidades de curto prazo.

- Um stop loss muito amplo pode prejudicar a rentabilidade.

- Um stop loss muito sensível aumenta a frequência de negociações e os custos com comissões.

- A volatilidade das ações pode afetar a estabilidade do parâmetro ATR.

É possível otimizar adequadamente os parâmetros das médias móveis ou ajustar o múltiplo do ATR para equilibrar a amplitude do stop loss. Também é possível adicionar outros indicadores como filtros para melhorar a entrada.

Direções de Otimização

- Testar mais combinações de parâmetros para encontrar a melhor média móvel.

- Ajustar o múltiplo do ATR de acordo com as características de cada ação.

- Adicionar filtros como indicadores de volume e preço para evitar negociações desnecessárias.

- Acumular mais dados históricos para testar e verificar a estabilidade dos parâmetros.

Resumo

Esta estratégia combina com sucesso o acompanhamento de tendência das médias móveis com o stop loss dinâmico baseado no ATR. Através da otimização de parâmetros, pode adaptar-se às características de diferentes ações. A estratégia estabelece limites claros de compra e stop loss, tornando a lógica de negociação simples e clara. No geral, esta estratégia de stop loss trailing com duas médias móveis é estável, simples e fácil de otimizar, sendo adequada como estratégia base para negociação de ações.

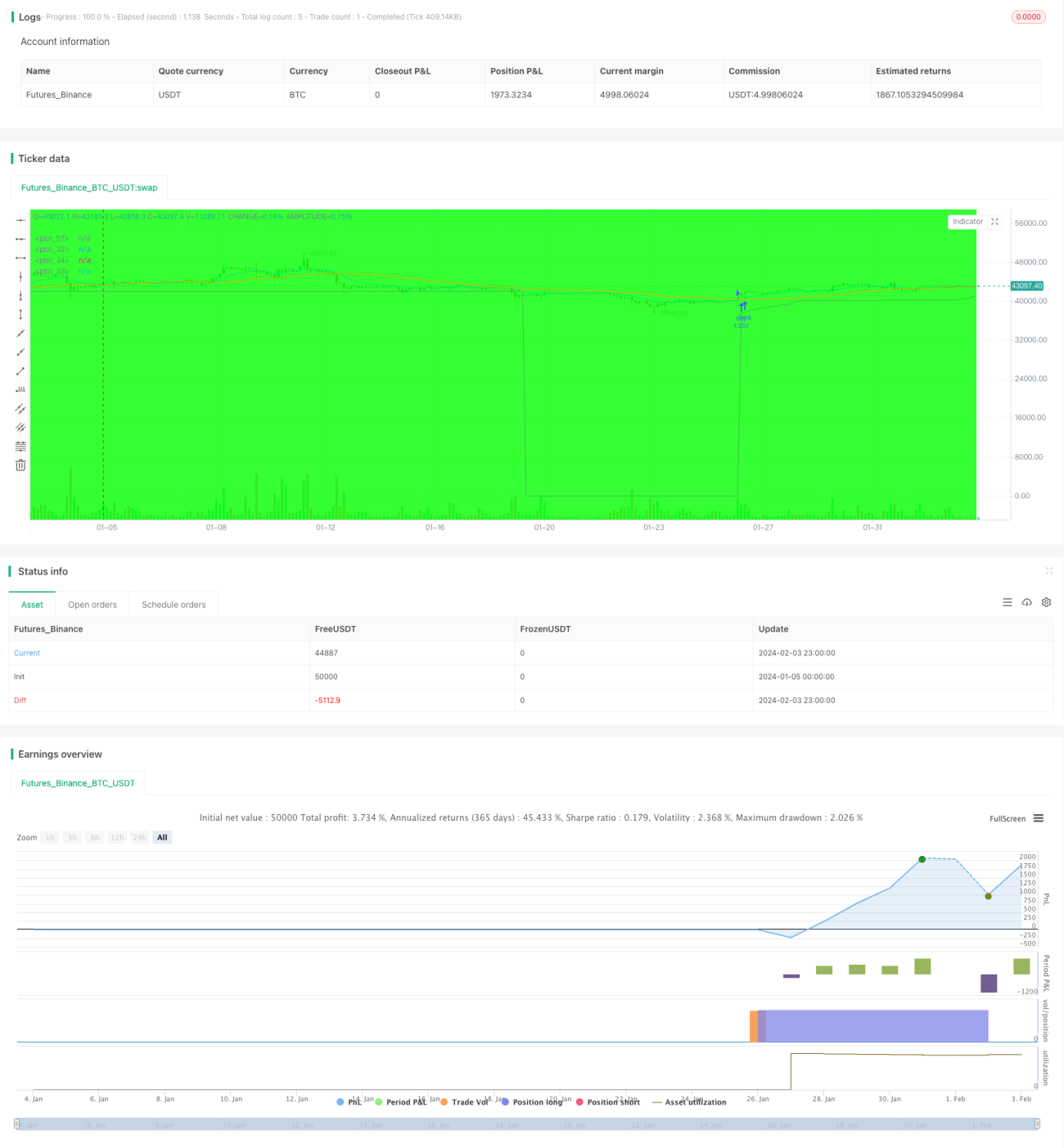

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

//created by XPloRR 24-02-2018

strategy("XPloRR MA-Buy ATR-MA-Trailing-Stop Strategy",overlay=true, initial_capital=1000,default_qty_type=strategy.percent_of_equity,default_qty_value=100)- 1