Estratégia de curto prazo combinando o indicador RSI e a ruptura de preço

Visão Geral

Esta estratégia combina o indicador RSI com rompimentos de preço, buscando oportunidades de rotação dentro de uma faixa de consolidação formada sob uma certa tendência, realizando assim operações de curto prazo para obter lucros rápidos e de alta eficiência.

Princípio da Estratégia

- Julgamento do RSI: Quando o RSI fica abaixo da linha de sobrevenda (30), gera-se um sinal de compra, atuando como um ponto potencial de reversão de compra; quando o RSI ultrapassa a linha de sobrecompra (60), gera-se um sinal de venda para realizar lucros;

- Restrição de Janela: Só é ativado dentro da janela de tempo especificada para o backtest, limitando assim a eficácia da estratégia e evitando arbitragem global;

- Julgamento de Rompimento: Combinado com a ação do preço, busca oportunidades de rompimento, aumentando o efeito prático da estratégia e prevenindo movimentos laterais desnecessários.

Portanto, a estratégia integra lógicas de julgamento de múltiplas dimensões. Sob uma certa tendência e oportunidade de rompimento, utiliza os sinais de compra e venda gerados pelo RSI para realizar operações de rotação visando lucros de curto prazo. Consegue capturar eficazmente oportunidades de reversão de sobrevenda e retorno de sobrecompra no curto prazo do mercado.

Análise de Vantagens

- Combinando múltiplas lógicas de julgamento, é mais rigorosa em comparação com estratégias RSI simples, evitando eficazmente perdas desnecessárias causadas por movimentos laterais em ambas as direções;

- Utiliza o indicador RSI para identificar zonas extremas locais, buscando oportunidades de reversão para obter lucros;

- Define uma janela de tempo para o backtest, permitindo a validação e otimização para condições específicas de mercado, aumentando a aplicabilidade prática da estratégia;

- Busca lucros de curto prazo, não exigindo a previsão de mudanças de tendência, sendo mais fácil de executar e reduzindo riscos.

Riscos e Soluções

- Não é possível determinar diretamente a direção da tendência geral, exigindo análise manual do contexto macro;

- O indicador RSI reage com atraso às mudanças de preço, podendo perder os melhores pontos de compra e venda;

- É necessário compreender profundamente o ambiente macro de mercado adequado para a estratégia;

- Podem ser introduzidos mais indicadores técnicos para avaliar a tendência principal, otimizar os parâmetros da estratégia e aumentar a sua flexibilidade.

Direções de Otimização

- Adicionar avaliação da tendência principal para evitar manter posições perdedoras por longos períodos;

- Ajustar os parâmetros do RSI e otimizar as linhas de sobrecompra e sobrevenda para melhorar a eficácia;

- Incluir lógica de stop loss;

- Otimizar o alcance da janela de backtest para tornar a estratégia mais alinhada com as condições reais do mercado.

Resumo

Esta estratégia utiliza o indicador RSI para identificar oportunidades de reversão de curto prazo em condições de sobrecompra e sobrevenda, combinando-as com rompimentos de preço para realizar operações de rotação visando lucros de curto prazo. Caracteriza-se pela busca de eficiência no curto prazo, simplicidade operacional e risco limitado, sendo ideal para traders de curto prazo em condições específicas de mercado. É necessário prestar atenção à tendência geral e otimizar parâmetros, entre outros aspetos, para obter melhores resultados.

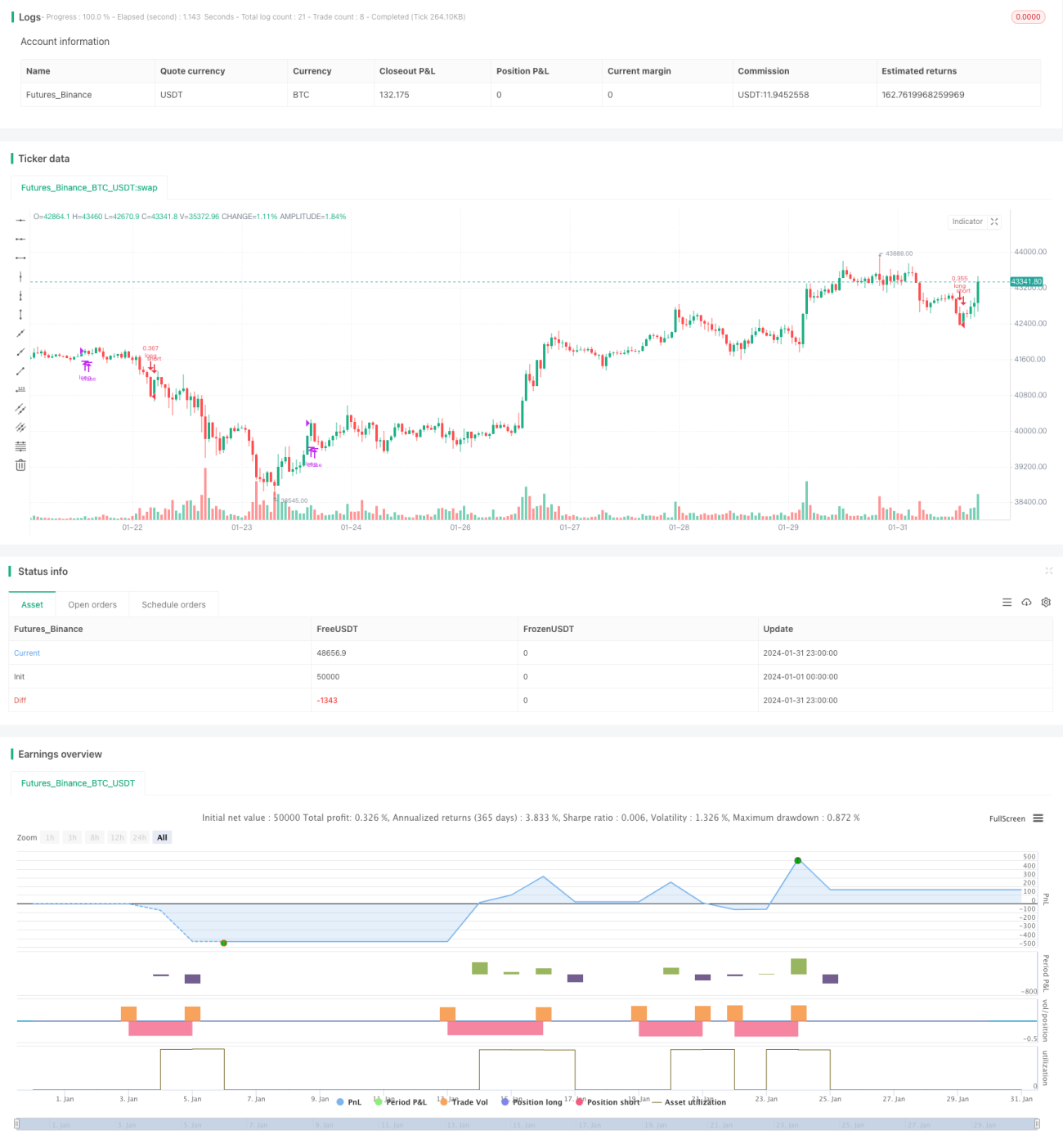

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © relevantLeader16058

//@version=4- 1