Estratégia de Negociação de Reversão com Ruptura de Canal

Visão Geral

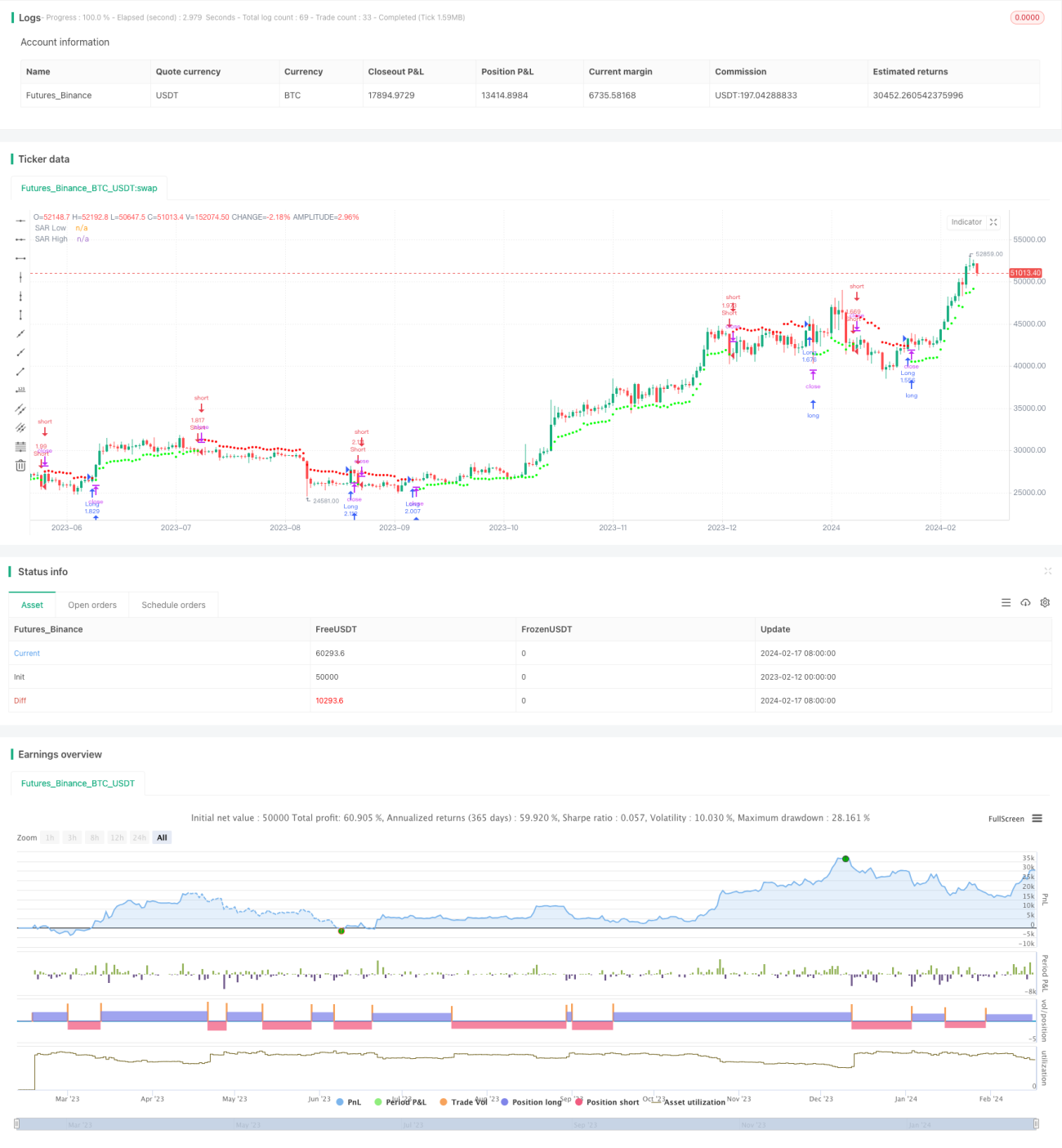

A Estratégia de Negociação de Reversão com Rompimento de Canal é uma estratégia de reversão que rastreia os pontos de stop-loss e take-profit móveis de um canal de preços. Ela utiliza o método de média móvel ponderada para calcular o canal de preços e estabelece posições compradas ou vendidas quando o preço rompe o canal.

Princípio da Estratégia

A estratégia primeiro calcula a volatilidade do preço usando o indicador ATR (Average True Range) de Wilder. Em seguida, com base no valor do ATR, calcula a Constante de Amplitude Média (ARC). A ARC representa metade da largura do canal de preços. Então, calcula as bandas superior e inferior do canal, que são os pontos de stop-loss e take-profit, chamados de pontos SAR. Quando o preço rompe a banda superior, a posição é vendida; quando rompe a banda inferior, a posição é comprada.

Especificamente, primeiro calcula-se o ATR das últimas N velas. Em seguida, multiplica-se o ATR por um coeficiente para obter a ARC. A multiplicação da ARC pelo coeficiente controla a largura do canal. A ARC é adicionada ao ponto mais alto de fechamento das últimas N velas para obter a banda superior do canal, ou SAR superior. A ARC é subtraída do ponto mais baixo de fechamento para obter a banda inferior do canal, ou SAR inferior. Se o preço de fechamento romper a banda superior, a posição é vendida; se o preço de fechamento romper a banda inferior, a posição é comprada.

Vantagens da Estratégia

- Utiliza a volatilidade dos preços para calcular um canal adaptativo, permitindo acompanhar as mudanças do mercado.

- Negociação de reversão, adequada para mercados com reversão de tendência.

- Stop-loss e take-profit móveis, permitindo travar lucros e controlar riscos.

Riscos da Estratégia

- A negociação de reversão pode facilmente resultar em posições presas, sendo necessário ajustar adequadamente os parâmetros.

- Em mercados com grandes oscilações, as posições podem ser facilmente fechadas.

- Parâmetros inadequados podem causar negociações excessivamente frequentes.

Soluções:

- Otimizar o período do ATR e o coeficiente da ARC para que a largura do canal seja razoável.

- Combinar com indicadores de tendência para filtrar os momentos de entrada.

- Aumentar o período do ATR para reduzir a frequência de negociações.

Direções de Otimização da Estratégia

- Otimizar o período do ATR e o coeficiente da ARC.

- Adicionar condições de abertura de posição, como combinar com o indicador MACD.

- Adicionar estratégias de stop-loss.

Conclusão

A Estratégia de Negociação de Reversão com Rompimento de Canal utiliza um canal para rastrear as mudanças de preço, construindo posições reversas quando a volatilidade aumenta e configurando stop-loss e take-profit adaptativos e móveis. Esta estratégia é adequada para mercados laterais com foco em reversões e, desde que os pontos de reversão sejam identificados com precisão, pode gerar retornos de investimento razoáveis. No entanto, é necessário ter cuidado para evitar pontos de stop-loss excessivamente largos e problemas de otimização de parâmetros.

- 1