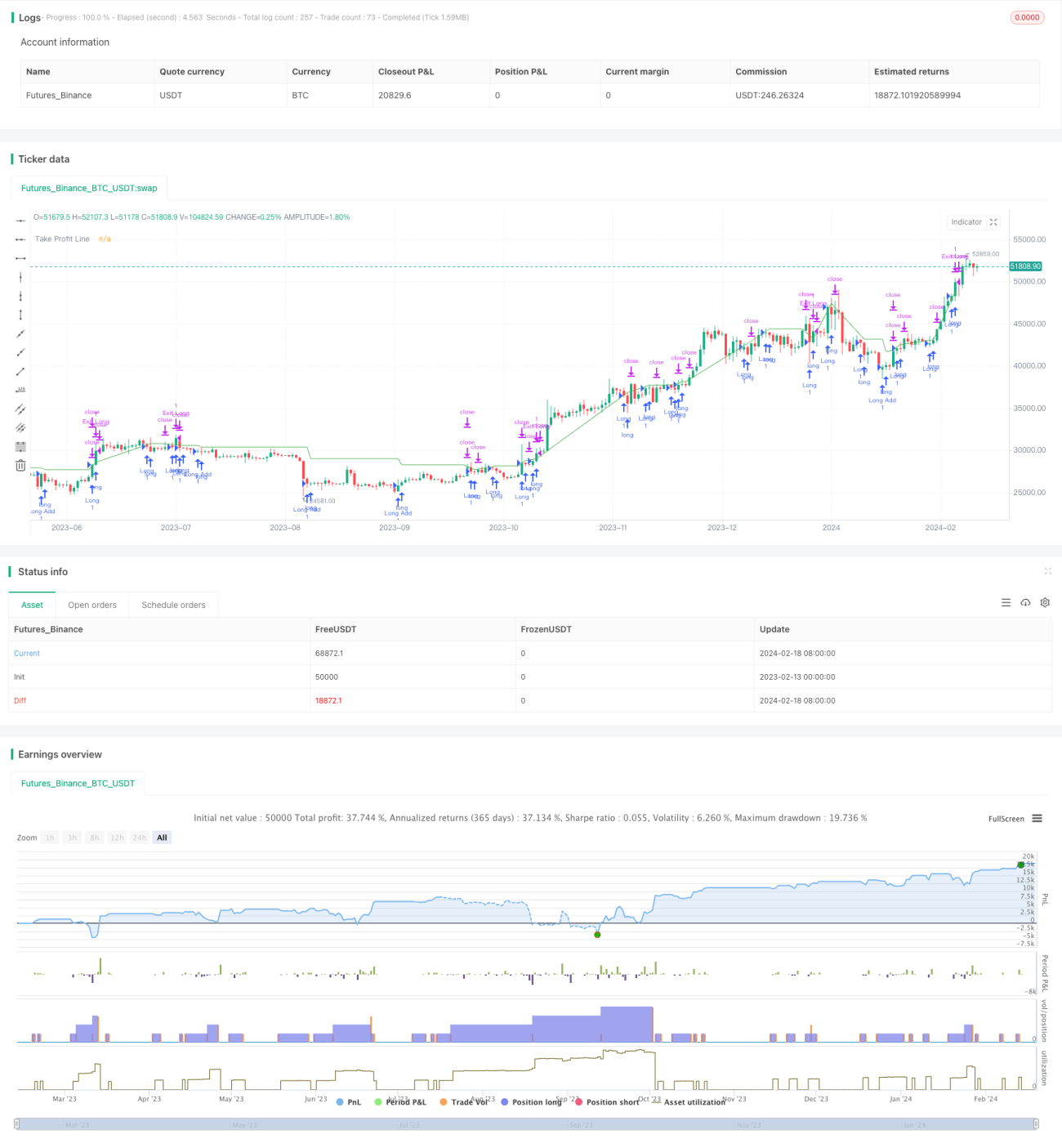

Estratégia de negociação quantitativa baseada em múltiplos fatores

Visão Geral

Esta estratégia combina múltiplos indicadores técnicos como RSI, MACD, OBV, CCI, CMF, MFI e VWMACD para detectar divergências entre preço e volume, identificando potenciais oportunidades de entrada. A estratégia também incorpora um indicador de detecção de dip definido pelo usuário, gerando sinais de negociação quando condições de alta volatilidade e profundidade ou VFI são atendidas. A estratégia opera apenas em posições compradas (long), utilizando trailing stop e aumentando gradualmente a posição.

Princípio da Estratégia

-

Calcula indicadores como RSI, MACD, OBV, CCI, CMF, MFI e VWMACD, e detecta divergências entre cada indicador e o histórico de preços através de um método de regressão linear adaptativa. Quando um indicador atinge novas mínimas sem que o preço as acompanhe, é gerado um sinal de compra.

-

Com base no limiar de volatilidade e no percentual de profundidade definidos pelo usuário, combinado com o filtro do indicador VFI, são emitidos sinais em candles que atendem às condições de alta volatilidade e teste de profundidade.

-

Após a primeira entrada comprada, se o preço cair abaixo de uma determinada porcentagem (configurável) em relação ao último preço de compra, a estratégia adiciona mais posições (recompra).

-

Utiliza trailing stop, encerrando a posição quando o lucro atinge a porcentagem de take profit configurada.

Análise de Vantagens

-

Combinação de múltiplos fatores, utilizando indicadores de preço e volume para aumentar a confiabilidade dos sinais.

-

O método de regressão linear adaptativa para detectar divergências elimina a subjetividade das análises manuais.

-

A integração de indicadores de volatilidade e profundidade/VFI ajuda a identificar oportunidades de reversão.

-

A estratégia de recompra em múltiplas etapas aproveita as correções de preço, e o trailing stop ajuda a garantir lucros.

Análise de Riscos

-

A combinação de múltiplos fatores torna a avaliação complexa; a otimização de parâmetros e a eficácia na detecção de divergências podem impactar o desempenho real.

-

Alto risco de posições unidirecionais (apenas compradas); erros de julgamento podem resultar em perdas significativas.

-

O padrão de recompra repetida amplifica as perdas, exigindo controle cuidadoso do tamanho da posição.

-

É necessário considerar o impacto das taxas de negociação sobre o lucro real.

Direções de Otimização

-

Testar diferentes combinações de parâmetros e indicadores para selecionar a configuração ideal.

-

Adicionar uma estratégia de stop loss para controlar perdas por operação e perda máxima.

-

Considerar oportunidades de negociação bidirecionais (compra e venda) para diversificar o risco.

-

Integrar métodos de aprendizado de máquina para otimizar automaticamente os parâmetros.

Resumo

Esta estratégia combina vários indicadores técnicos para identificar pontos de entrada, utilizando condições definidas pelo usuário e o indicador VFI para filtrar sinais falsos. A estratégia aproveita as correções de preço para aumentar posições gradualmente, favorecendo a captura de oportunidades durante tendências. No entanto, também enfrenta riscos de erros de julgamento e exposição unidirecional, exigindo otimização adequada dos parâmetros dos indicadores e estratégias de stop loss para reduzir riscos e aumentar o potencial de lucro.

- 1