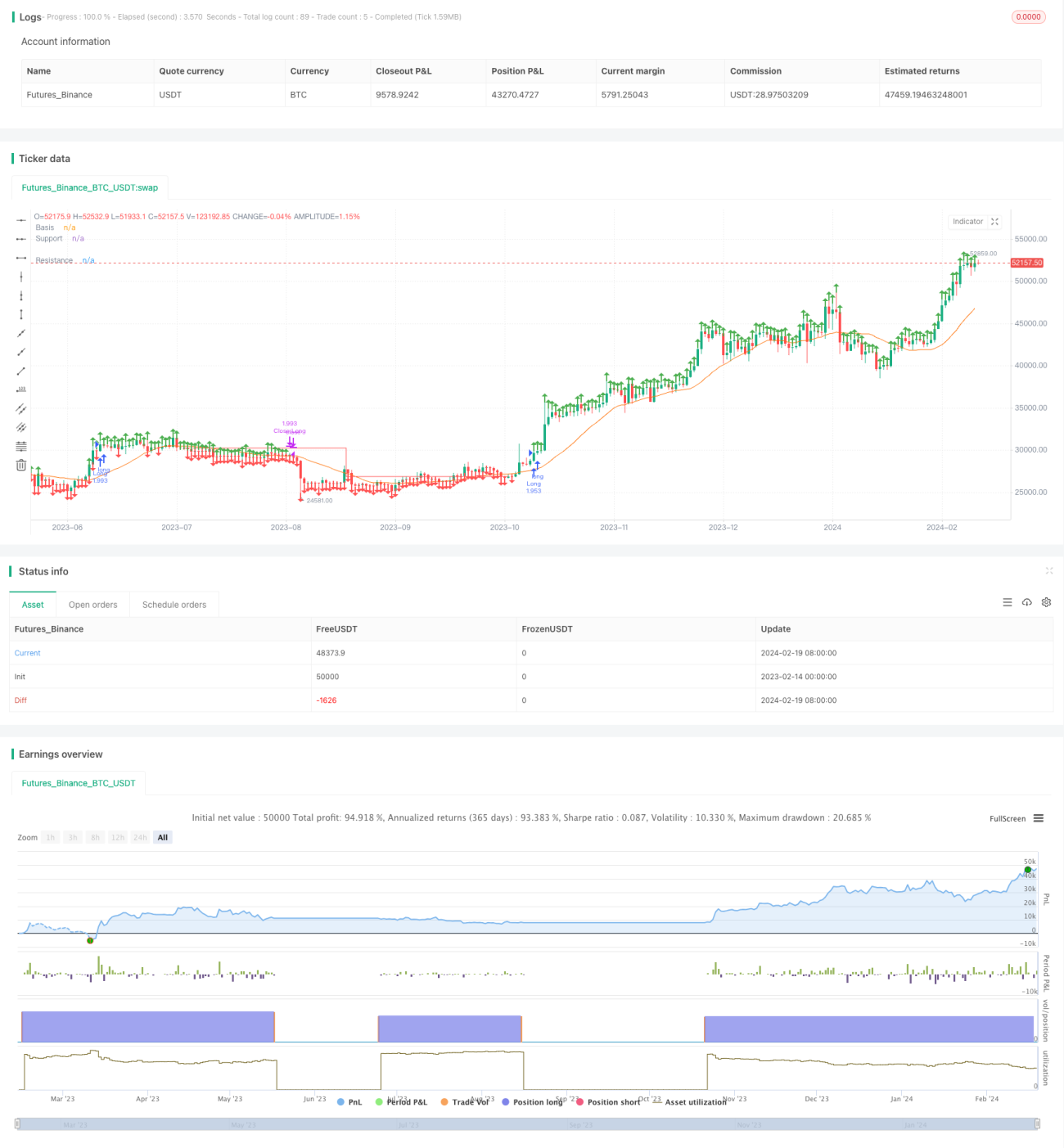

Estratégia de referência de tendência de alta do tipo breakout

Visão geral

Esta estratégia é uma estratégia de posicionamento de longo prazo baseada em médias móveis simples para determinar a direção da tendência, combinada com linhas de suporte e resistência para formar sinais de rompimento. Ao calcular os pontos de pivot máximos e mínimos, traça linhas de resistência e suporte. Quando o preço rompe a linha de resistência, abre uma posição longa; quando rompe a linha de suporte, fecha a posição. Esta estratégia é adequada para ações com tendências claras, podendo obter uma boa relação risco-retorno.

Princípios da estratégia

- Calcular a média móvel simples de 20 períodos como linha de base para julgar a tendência.

- Calcular os pontos de pivot máximos e mínimos com base nos parâmetros fornecidos pelo usuário.

- Traçar linhas de resistência e suporte com base nos pontos de pivot máximos e mínimos.

- Quando o preço de fechamento estiver acima da linha de resistência, entrar em posição longa.

- Quando a linha de suporte cruzar abaixo da linha de resistência, fechar a posição.

Esta estratégia usa médias móveis simples para determinar a direção geral da tendência e, em seguida, utiliza rompimentos de pontos-chave para formar sinais de negociação, sendo uma estratégia típica de rompimento. Através dos pontos-chave e do julgamento da tendência, é possível filtrar eficazmente os falsos rompimentos.

Análise de vantagens

- A estratégia oferece oportunidades suficientes, adequada para ações de alta volatilidade, facilitando a captura de tendências.

- Controle de risco eficaz, alta relação risco-retorno.

- Utiliza sinais de rompimento, evitando o risco de falsos rompimentos.

- Parâmetros personalizáveis, alta adaptabilidade.

Análise de riscos

- Depende da otimização de parâmetros; parâmetros inadequados aumentam a probabilidade de falsos rompimentos.

- Atraso nos sinais de rompimento, podendo perder algumas oportunidades.

- Facilmente aciona stop loss em mercados oscilantes.

- Ajuste tardio da linha de suporte pode causar perdas.

É possível otimizar os parâmetros em negociação real e combinar com estratégias de stop loss e take profit para reduzir riscos.

Direções de otimização

- Otimizar os parâmetros do período da média móvel.

- Otimizar os parâmetros das linhas de suporte e resistência.

- Adicionar estratégias de stop loss e take profit.

- Adicionar mecanismos de confirmação de rompimento.

- Combinar com indicadores como volume de negociação para filtrar sinais.

Conclusão

No geral, esta estratégia é uma estratégia típica de rompimento, dependendo da otimização de parâmetros e liquidez, adequada para traders que seguem tendências. Como um quadro de referência, pode ser expandido modularmente conforme as necessidades reais, utilizando mecanismos como stop loss/take profit e filtragem de sinais para reduzir riscos e melhorar a estabilidade.

- 1