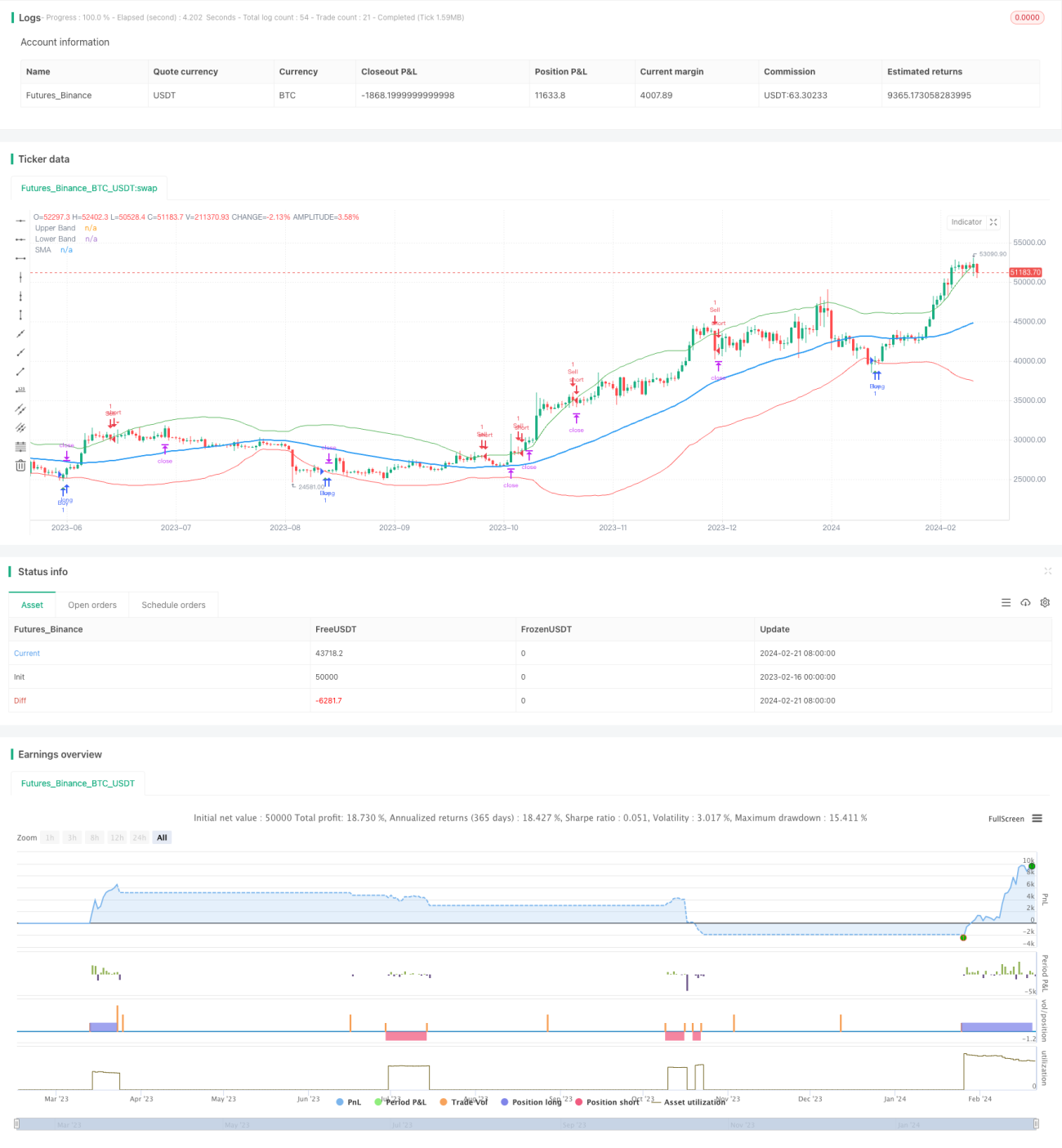

Estratégia de rastreamento de tendência com base em regressão de média móvel e rompimentos

Visão Geral

A Estratégia de Ruptura de Regressão à Média Móvel é uma estratégia de negociação quantitativa típica de acompanhamento de tendência. Essa estratégia utiliza médias móveis e seus canais de desvio padrão para julgar a direção do mercado e gera sinais de negociação quando o preço rompe o canal de desvio padrão.

Princípio da Estratégia

Primeiro, a estratégia calcula a média móvel simples (SMA) de N dias (padrão 50 dias) e, em seguida, com base na SMA, calcula o desvio padrão (StdDev) do preço para esse período. Usando a SMA como eixo central, são construídos canais de desvio padrão com limites superior e inferior de 2 vezes o StdDev. Quando o preço cruza o limite superior para cima, é feita uma venda a descoberto; quando o preço cruza o limite inferior para baixo, é feita uma compra.

Após entrar no mercado, a estratégia define níveis de stop loss e take profit. Especificamente, após comprar, o stop loss é o preço de fechamento no momento da entrada multiplicado por (100 – percentual de stop loss); após vender a descoberto, o take profit é o preço de fechamento no momento da entrada multiplicado por (100 + percentual de take profit).

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Forte capacidade de acompanhamento de tendência. O uso do canal de desvio padrão permite acompanhar dinamicamente a volatilidade do mercado.

- Forte controle de drawdown. O uso de stop loss móvel controla efetivamente perdas individuais.

- Implementação simples. Elimina a necessidade de grande otimização de parâmetros, sendo muito fácil de implementar.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Risco de reversão de tendência. Estratégias de acompanhamento de tendência estão sujeitas a saídas com perda seguidas de reversão.

- Risco de sensibilidade a parâmetros. A escolha dos parâmetros do período da média móvel e do múltiplo do desvio padrão tem grande impacto no desempenho da estratégia.

- Stop loss excessivamente agressivo pode causar perdas adicionais. A definição inadequada do nível de stop loss pode resultar em perdas extras.

As soluções correspondentes para os riscos são:

- Combinar com indicadores de volatilidade para evitar falsos rompimentos.

- Otimizar os parâmetros para encontrar a combinação ideal.

- Ajustar o mecanismo de stop loss para evitar agressividade excessiva.

Direções de Otimização

A estratégia ainda possui espaço para otimização adicional:

-

Usar médias móveis de múltiplos períodos de tempo para validação, evitando sensibilidade excessiva da curva.

-

Combinar outros indicadores, como MACD, para julgar tendências e divergências.

-

Introduzir algoritmos de aprendizado de máquina para otimizar dinamicamente os parâmetros.

Resumo

No geral, a Estratégia de Ruptura de Regressão à Média Móvel é uma estratégia de negociação quantitativa muito prática. Ela possui as vantagens de acompanhar tendências e controlar drawdowns, é simples de implementar e adequada às necessidades da negociação quantitativa. Também é necessário estar atento a questões de seleção de parâmetros e definição de stop loss. Com a análise multi-temporal e a otimização de parâmetros, é possível obter um desempenho ainda melhor da estratégia.

- 1