Estratégia de negociação multi-timeframe baseada em indicador de compressão

Visão Geral

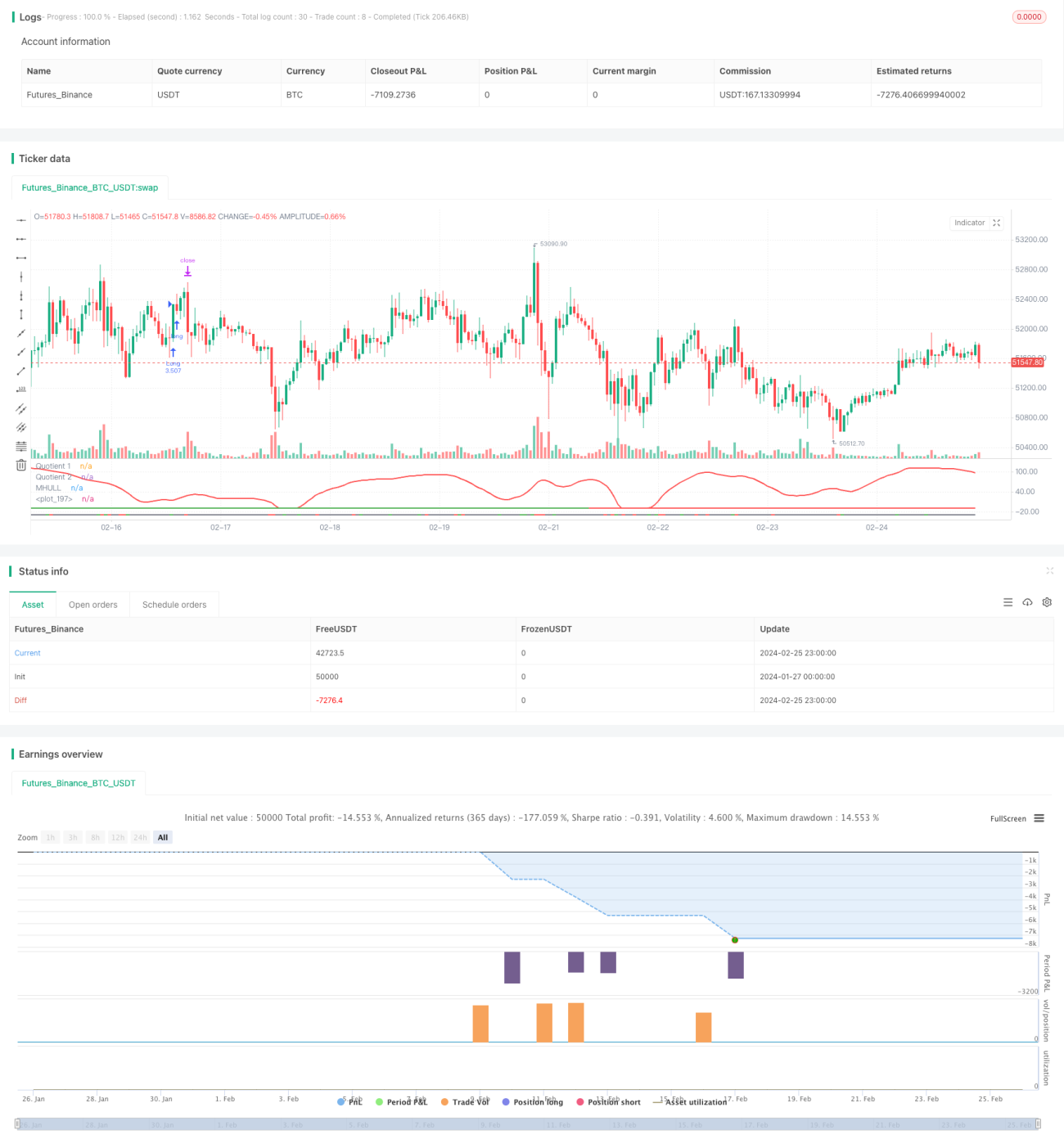

Esta estratégia combina três indicadores – Boom Hunter, Hull Suite e Volatility Oscillator – para realizar negociações quantitativas de acompanhamento de tendência e rompimento em múltiplos períodos. É adequada para ativos digitais como o Bitcoin, que apresentam alta volatilidade e movimentos de preço repentinos.

Princípio

A lógica central da estratégia baseia-se nos três indicadores a seguir:

-

Boom Hunter: um oscilador que utiliza técnica de compressão de indicadores. Através do cruzamento de dois indicadores (Quotient1 e Quotient2), gera sinais de compra e venda.

-

Hull Suite: um conjunto de médias móveis suavizadas. Através da relação entre a banda central e as bandas superior e inferior, determina a direção da tendência.

-

Volatility Oscillator: um oscilador que quantifica informações de volatilidade dos preços.

A lógica de entrada da estratégia é: quando os dois indicadores Quotient do Boom Hunter fazem um cruzamento para cima ou para baixo, ao mesmo tempo o preço rompe a banda central do Hull e diverge da banda superior ou inferior, e o indicador de volatilidade está na região de sobrecompra ou sobrevenda. Isso ajuda a filtrar sinais falsos de rompimento, aumentando a precisão da entrada.

O stop loss é definido localizando o vale mais baixo ou o pico mais alto dentro de um determinado período (padrão: 20 velas). O lucro é obtido multiplicando a percentagem do stop loss pela relação de take profit configurada (padrão: 3x). O tamanho da posição é calculado com base numa percentagem do patrimônio total da conta (padrão: 3%) e na distância do stop loss do ativo específico.

Vantagens

- Utiliza técnica de compressão de indicadores para extrair os principais sinais de negociação dos preços, aumentando a probabilidade de lucro.

- Combinação de múltiplos indicadores para verificação, evitando rompimentos falsos e identificando com precisão a direção da tendência.

- Definição dinâmica de stop loss e take profit, permitindo um acompanhamento de tendência com risco controlado.

- Utiliza indicador de volatilidade para garantir negociações em ambientes de alta volatilidade.

- Análise em múltiplos períodos, aumentando a estabilidade da estratégia.

Riscos

- O indicador Boom Hunter pode sofrer distorções de compressão, gerando sinais incorretos.

- A banda central do Hull Suite tem atraso, não conseguindo acompanhar as mudanças de preço em tempo real.

- Quando a volatilidade diminui, podem perder-se oportunidades de negociação ou ocorrer fechamentos com prejuízo.

Formas de mitigar:

- Ajustar os parâmetros do indicador de compressão para equilibrar a sensibilidade.

- Experimentar usar médias móveis exponenciais como a EHMA para substituir a banda central.

- Adicionar outros indicadores de confirmação para evitar interpretações erradas da volatilidade.

Otimização

A estratégia pode ser otimizada nos seguintes aspetos:

-

Otimização de parâmetros: alterar parâmetros como comprimento do período, coeficiente de compressão, etc., para obter a melhor combinação.

-

Otimização de período: testar diferentes períodos (1 minuto, 5 minutos, 30 minutos, etc.) para encontrar o mais adequado.

-

Otimização de tamanho de posição: alterar o tamanho e a percentagem da posição em cada negociação para encontrar a melhor alocação de capital.

-

Otimização de stop loss: ajustar a localização do stop loss para diferentes pares de negociação, obtendo a melhor relação risco-retorno.

-

Otimização de condições: adicionar ou remover condições de filtro dos indicadores para obter momentos de entrada mais precisos.

Resumo

Esta estratégia combina os indicadores Boom Hunter, Hull Suite e Volatility Oscillator para realizar negociações de acompanhamento de tendência em múltiplos períodos. Ela é capaz de identificar movimentos súbitos de preço com eficácia, sendo adequada para ativos digitais de alta volatilidade. A estratégia tem risco controlado e, através da otimização de parâmetros, condições de filtro e stop loss, apresenta grande aplicabilidade prática e escalabilidade.

- 1