Estratégia de Seguimento de Tendência com Tripla Confirmação

Visão Geral

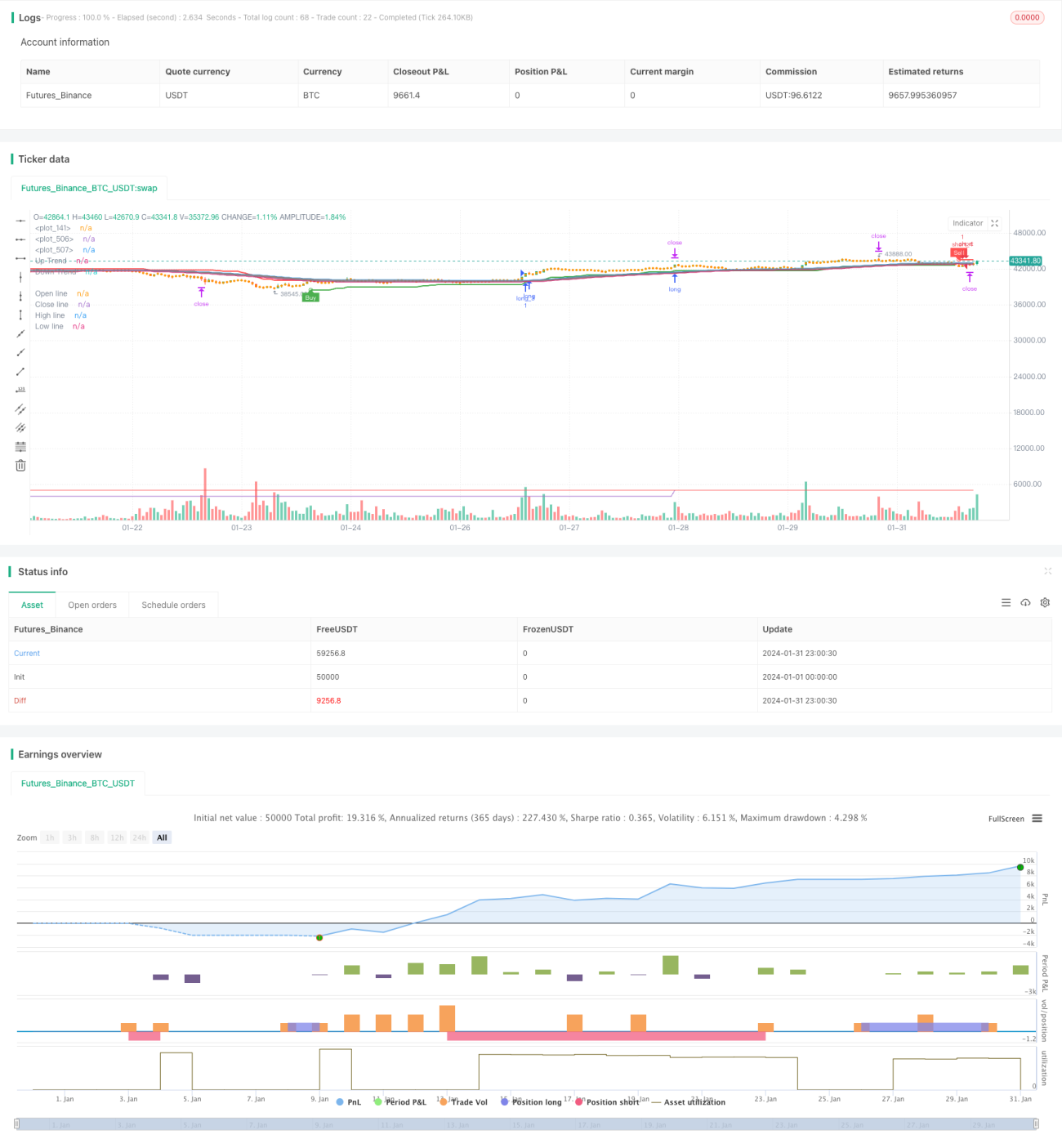

A Estratégia de Rastreamento de Tendência com Tripla Confirmação combina sinais de três indicadores – Média Móvel, Linha de Intenção e Super Tendência – para capturar tendências com alta probabilidade. Quando os três indicadores emitem simultaneamente um sinal de compra ou venda, a estratégia entra no mercado de forma oportuna e rastreia a tendência. Quando a tendência se inverte, a estratégia fecha rapidamente a posição e assume uma posição vendida.

Princípio da Estratégia

Média Móvel para Determinar a Tendência Principal

A estratégia utiliza uma Média Móvel de período 52 para determinar a direção da tendência principal. Quando o preço cruza acima da Média Móvel, a tendência é considerada de alta; quando cruza abaixo, a tendência é considerada de baixa.

Linha de Intenção para Identificar Reversões Secundárias

A estratégia também utiliza a Linha de Intenção para identificar reversões secundárias de curto prazo. O cálculo da Linha de Intenção é semelhante ao da Média Móvel, mas substitui o preço de fechamento pelo preço de abertura, permitindo uma reação mais rápida às reversões de preço. Quando o preço cruza acima da Linha de Intenção descendente, sinaliza uma possível estabilização e recuperação de curto prazo; quando cruza abaixo da Linha de Intenção ascendente, sinaliza uma possível queda de curto prazo.

Super Tendência para Identificar Pontos de Reversão

A estratégia também combina o indicador Super Tendência para identificar pontos-chave de reversão. O Super Tendência utiliza o período da janela do ATR e os dados de preço para ajustar dinamicamente os canais superior e inferior, determinando assim o momento da reversão.

Filtro de Sinais com Tripla Confirmação

A estratégia só assume uma posição comprada quando os três indicadores (Média Móvel, Linha de Intenção e Super Tendência) emitem simultaneamente um sinal de compra; e só assume uma posição vendida quando os três emitem simultaneamente um sinal de venda. Essa tripla confirmação filtra efetivamente sinais falsos e aumenta a probabilidade de entrada.

Análise de Vantagens

Julgamento Multidimensional com Alta Probabilidade

Ao combinar Média Móvel, Linha de Intenção e Super Tendência, a estratégia avalia tendências e pontos críticos sob diferentes perspectivas, garantindo entradas de alta probabilidade.

Reação Rápida e Acompanhamento em Tempo Real

A introdução da Linha de Intenção garante que a estratégia reaja rapidamente às reversões de curto prazo dos preços; o Super Tendência com canais adaptativos baseados no ATR também acompanha as mudanças de preço em tempo real.

Stop Loss e Take Profit Automáticos para Controle de Risco

A estratégia incorpora lógica automática de stop loss e take profit, ajustando dinamicamente os níveis com base no ATR, controlando efetivamente as perdas individuais.

Riscos e Soluções

Risco de Alta Frequência de Negociação

Devido à frequência elevada de sinais, a estratégia pode gerar negociações excessivas. É possível aumentar o período da Média Móvel para reduzir a frequência de operações.

Risco de Incerteza na Reversão

A eficácia da Linha de Intenção e do Super Tendência na identificação de pontos de reversão não é garantida, podendo ocorrer erros de julgamento. Podem ser adicionados filtros adicionais nos parâmetros dos indicadores para garantir sinais de reversão de maior probabilidade.

Risco de Perdas em Mercados Laterais

Em mercados laterais, devido aos repetidos cruzamentos, a estratégia pode abrir e fechar posições com frequência, gerando perdas. É possível identificar períodos de lateralidade e pausar a estratégia durante essas fases.

Direções de Otimização

Combinar com Indicadores de Volatilidade

Pode-se considerar a incorporação de indicadores de volatilidade, como as Bandas de Bollinger. Quando o preço se aproxima das bandas superior ou inferior, evitar novas entradas ajuda a reduzir riscos em mercados laterais.

Adicionar Condições de Filtro de Entrada

Podem ser adicionados outros indicadores auxiliares, como KDJ, MACD, etc., exigindo que também emitam sinais simultâneos para entrar. Isso filtra ainda mais sinais falsos e reduz negociações desnecessárias.

Otimizar Estratégias de Stop Loss e Take Profit

As estratégias de stop loss e take profit podem ser otimizadas, como stop loss móvel, stop loss exponencial móvel, take profit parcial por escalonamento, etc., para aumentar e estabilizar os lucros.

Conclusão

A Estratégia de Rastreamento de Tendência com Tripla Confirmação aproveita plenamente as vantagens da Média Móvel, da Linha de Intenção e do Super Tendência para identificar e capturar tendências com alta probabilidade. Além disso, incorpora mecanismos automáticos de stop loss e take profit para controlar efetivamente as perdas individuais. Para maior praticidade, sugere-se otimizar a estratégia combinando outros indicadores auxiliares para filtrar entradas e aprimorando as estratégias de stop loss e take profit.

- 1