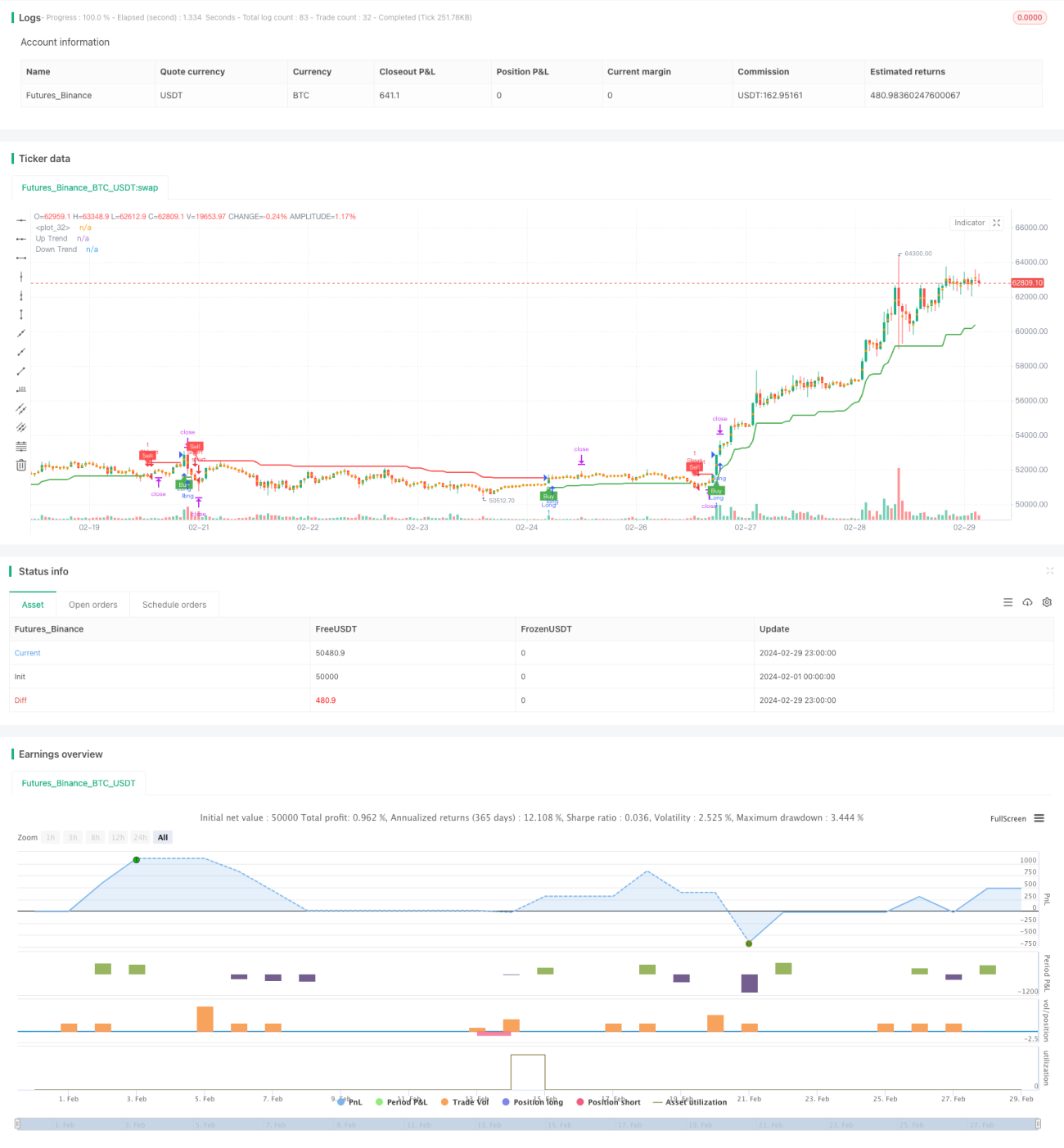

Estratégia Super Trend ATR

Visão geral

Esta é uma estratégia baseada em indicadores de tendência super e indicadores ATR. A principal idéia da estratégia é: usar indicadores de tendência super para determinar a direção da tendência do mercado atual e negociar quando os indicadores de tendência super mudam. Ao mesmo tempo, a estratégia usa o indicador ATR para calcular o preço de parada e parada e calcular o tamanho da posição de acordo com uma certa proporção do saldo da conta para controlar o risco.

Princípio da estratégia

O princípio da estratégia é o seguinte:

- Calcular o valor do indicador de super tendência, que gera um sinal de compra ou venda quando o indicador de super tendência muda.

- O indicador ATR é usado para calcular o preço de parada e o preço de parada, multiplicando o preço de parada pelo valor de ATR adicionado ao preço atual por um múltiplo, e o preço de parada pelo preço de parada por um risco-benefício.

- O tamanho da posição é calculado de acordo com uma certa proporção do saldo da conta e o preço de parada para controlar o risco de cada transação.

- Quando um sinal de compra é gerado, a posição é aberta, o preço de parada é o preço de produção do sinal menos o valor do ATR multiplicado por um múltiplo, o preço de parada é o preço de produção do sinal mais o valor do ATR multiplicado por um múltiplo multiplicado pela taxa de ganho de risco.

- Quando o sinal de venda é gerado, a posição é fechada, o preço de parada é o preço de produção do sinal mais o valor do ATR multiplicado por um múltiplo, o preço de parada é o preço de produção do sinal menos o valor do ATR multiplicado por um múltiplo multiplicado pelo risco de ganho.

Vantagens estratégicas

As vantagens desta estratégia são:

- A combinação de rastreamento de tendências e indicadores de volatilidade permite capturar as tendências de forma eficaz e, ao mesmo tempo, controlar os riscos.

- O tamanho da posição é calculado automaticamente de acordo com o saldo da conta e o nível de risco, sem necessidade de ajuste manual e fácil de implementar.

- Os parâmetros podem ser ajustados de forma flexível para diferentes mercados e variedades.

Risco estratégico

Os riscos dessa estratégia são:

- Em mercados turbulentos, os sinais de compra e venda frequentes podem levar a custos de transação mais elevados e a pontos de deslizamento.

- As proporções fixas de stop loss e de stop loss podem não se adaptar às mudanças no mercado, resultando em stop loss prematuros ou em lucros muito pequenos.

- O cálculo do tamanho da posição depende da volatilidade histórica, que pode levar a um retorno maior se a volatilidade aumentar de repente.

As medidas a serem tomadas para combater estes riscos são:

- Aumentar as condições de filtragem de sinais e reduzir a frequência de transações.

- Otimização de métodos de cálculo de stop-loss e paralisação, como o uso de stop-loss móvel ou paralisação dinâmica.

- Introduzir fatores de controle de risco no cálculo da posição, como reduzir a posição quando a taxa de flutuação for ultrapassada.

Direção de otimização da estratégia

A estratégia pode ser melhorada em:

- A introdução de mais indicadores técnicos, como MACD, RSI e outros, como condição auxiliar para o julgamento de tendências e filtragem de sinais, aumenta a precisão do sinal.

- Optimizar os parâmetros do Super Trend Indicator e do ATR Indicator para encontrar a melhor combinação de parâmetros para diferentes mercados e variedades.

- A introdução de mais fatores de controle de risco no cálculo de posições, como o retorno máximo da conta, o risco máximo de uma única transação, etc., aumenta a solidez da estratégia.

- Aumentar as estratégias de stop-loss, como stop-loss parciais, stop-loss móveis, etc., para aumentar os lucros.

A otimização acima pode aumentar a lucratividade e a estabilidade da estratégia, ao mesmo tempo em que reduz o risco da estratégia, tornando-a mais adaptável a diferentes condições de mercado.

Resumir

A estratégia combina o indicador de tendência super e o indicador ATR para capturar efetivamente a tendência e, ao mesmo tempo, controlar o risco. O risco de cada transação é controlado por meio do cálculo do tamanho da posição ideal.

- 1