Estratégia de negociação BTC com múltiplos indicadores

Visão Geral

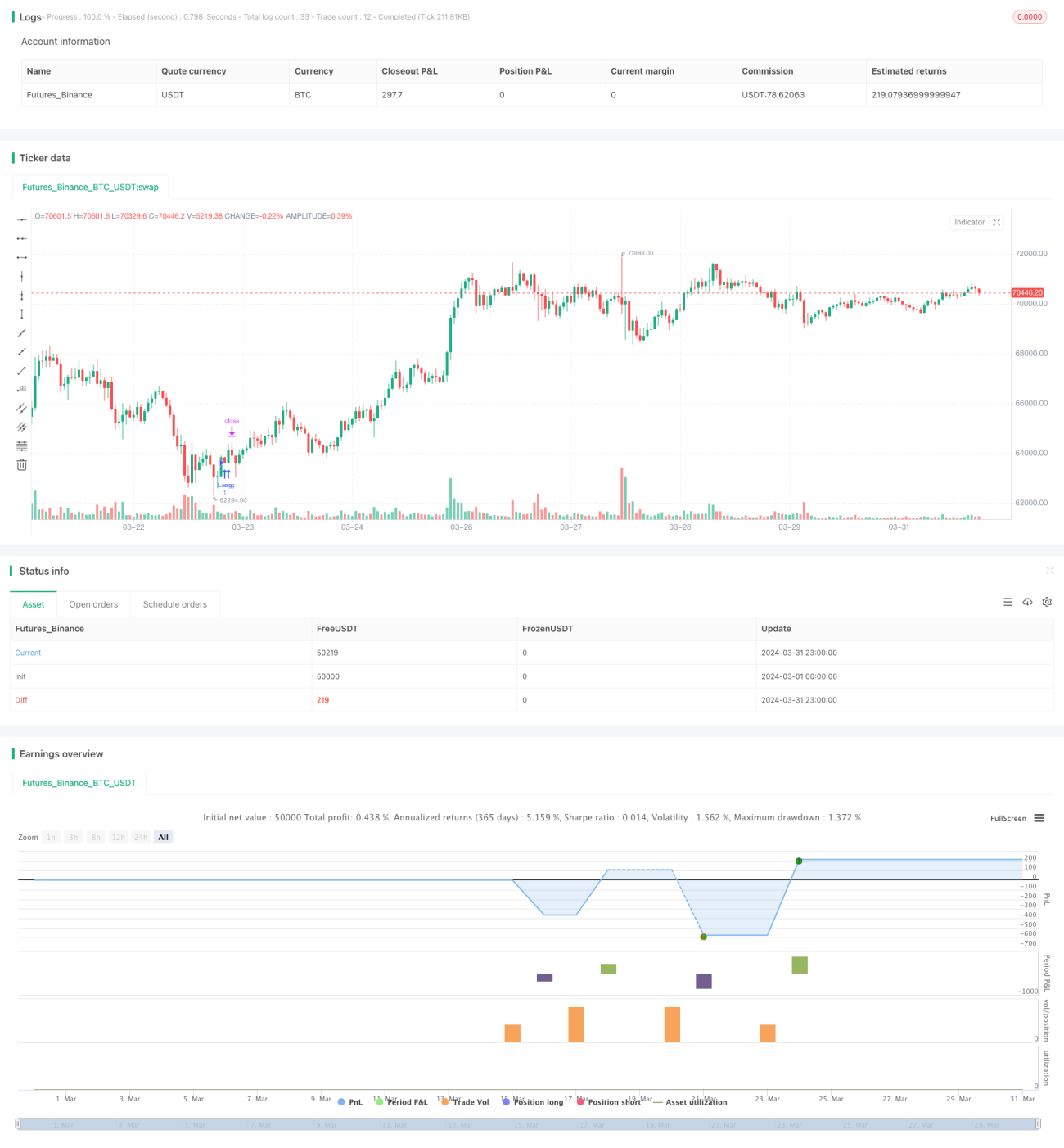

Esta estratégia combina múltiplos indicadores técnicos, incluindo o Índice de Força Relativa (RSI), o Indicador de Convergência/Divergência de Médias Móveis (MACD) e várias Médias Móveis Simples (SMA) de diferentes períodos, com o objetivo de fornecer uma ferramenta de análise abrangente para negociação de Bitcoin (BTC). A ideia principal da estratégia é considerar sinais de diferentes indicadores em conjunto: abrir posições longas quando o RSI estiver em uma faixa específica, o MACD apresentar um cruzamento de alta, o preço estiver abaixo de várias SMAs, enquanto define stop loss e take profit, e atualiza o stop loss quando o RSI atinge 50.

Princípio da Estratégia

- Calcular os indicadores RSI, MACD e SMAs de diferentes períodos.

- Verificar se o valor anterior do RSI está abaixo do limite inferior ou acima do limite superior, se o valor atual do RSI está entre o limite inferior e superior, se o MACD apresenta um cruzamento de alta, e se o preço de fechamento está abaixo de todas as SMAs.

- Se as condições acima forem atendidas e não houver posição aberta, abrir uma posição longa.

- Definir o stop loss e o take profit com base em uma porcentagem de risco.

- Se houver uma posição longa e o RSI atingir 50, atualizar o stop loss para o preço máximo.

- Se o MACD apresentar um cruzamento de baixa, fechar a posição.

Vantagens da Estratégia

- Considera múltiplos indicadores técnicos, aumentando a confiabilidade dos sinais.

- Abre posições quando o RSI está em uma faixa específica, evitando entradas em condições extremas.

- Define stop loss e take profit, controlando o risco.

- Ajusta dinamicamente o stop loss, travando parte dos lucros.

- Fecha a posição prontamente com base no sinal de cruzamento de baixa do MACD, reduzindo perdas potenciais.

Riscos da Estratégia

- Em mercados laterais, sinais frequentes de negociação podem levar a excesso de negociações e perdas com taxas.

- Stop loss e take profit baseados em porcentagens fixas de risco podem não se adaptar a diferentes condições de mercado.

- Depender exclusivamente de indicadores técnicos, ignorando fatores fundamentais, pode levar a decisões de negociação equivocadas.

Direções de Otimização da Estratégia

- Incorporar mais indicadores técnicos ou indicadores de sentimento do mercado para aumentar a precisão dos sinais.

- Ajustar dinamicamente os níveis de stop loss e take profit com base na volatilidade do mercado, adaptando-se a diferentes ambientes.

- Combinar análise fundamental, como grandes eventos noticiosos ou mudanças regulatórias, para auxiliar nas decisões de negociação.

- Considerar indicadores de diferentes períodos de tempo para capturar oportunidades de negociação em múltiplas escalas.

Resumo

Esta estratégia oferece uma estrutura de análise abrangente para negociação de Bitcoin, utilizando indicadores técnicos como RSI, MACD e SMA. Ela gera sinais de negociação com base na confirmação conjunta de múltiplos indicadores e implementa medidas de controle de risco. No entanto, ainda há espaço para otimização, como a introdução de mais indicadores, ajuste dinâmico de parâmetros e incorporação de análise fundamental. Na prática, os traders devem adaptar a estratégia de acordo com sua tolerância ao risco e as condições de mercado.

- 1