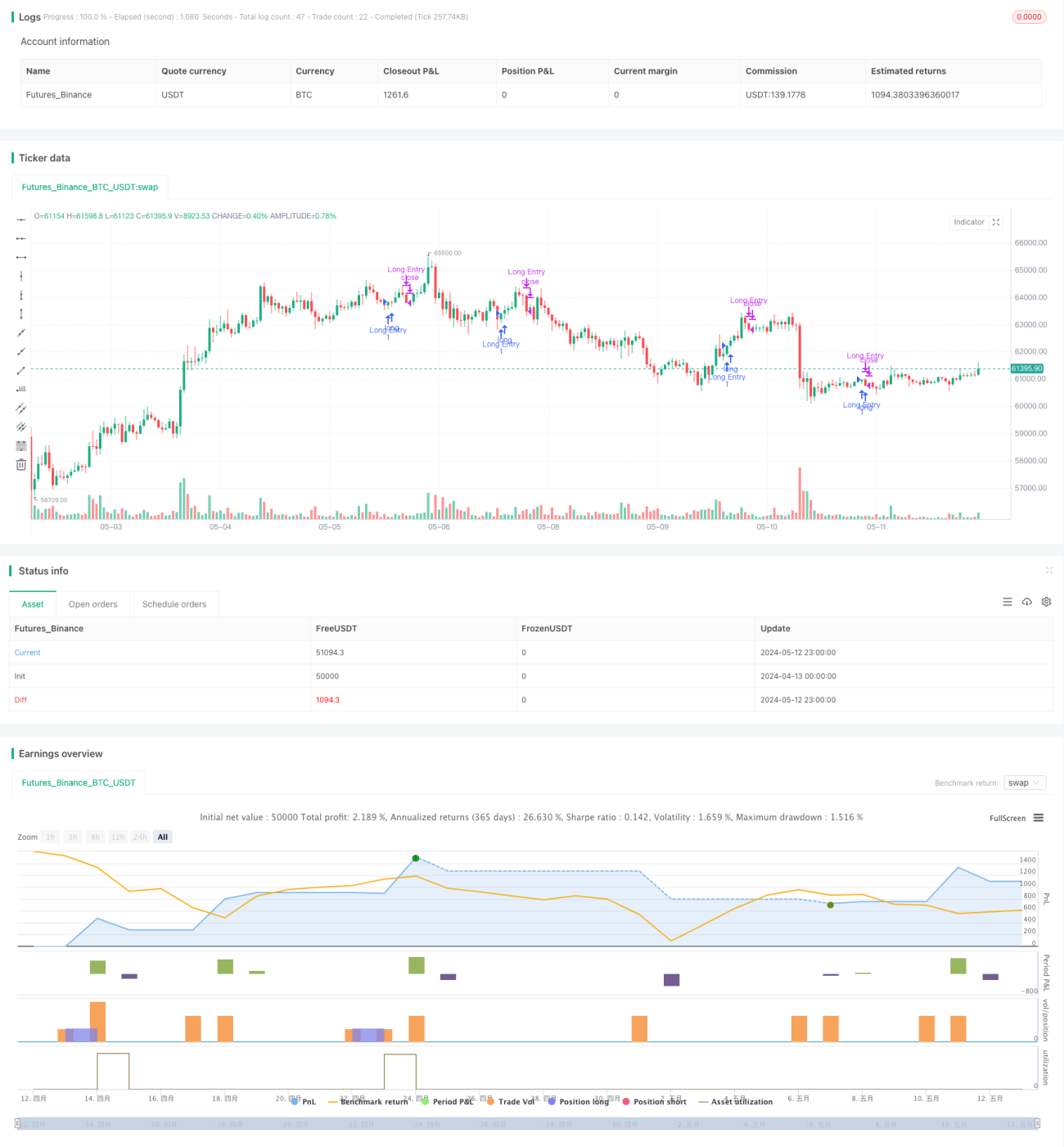

Visão Geral

A ideia principal desta estratégia é encontrar velas de alta sem pavio superior como sinal de compra e fechar a posição quando o preço cair abaixo do mínimo da vela anterior. A estratégia utiliza a característica de velas de alta com pavio superior muito pequeno, indicando forte momentum de alta e maior probabilidade de continuação do aumento de preço. Ao mesmo tempo, usar o mínimo da vela anterior como nível de stop-loss pode controlar o risco de forma eficaz.

Princípios da Estratégia

- Determinar se a vela atual é uma vela de alta (preço de fechamento maior que o preço de abertura)

- Calcular a relação entre o comprimento do pavio superior da vela atual e o comprimento do seu corpo

- Se a proporção do pavio superior for inferior a 5%, considere-a uma vela de alta válida sem pavio superior e gere um sinal de compra

- Registrar o preço mais baixo da vela anterior após a compra como nível de stop-loss

- Quando o preço cair abaixo do nível de stop-loss, feche a posição e saia

Vantagens da Estratégia

- Selecionar velas de alta sem pavio superior para entrada, a força da tendência é maior e a taxa de sucesso é maior

- Usar o mínimo da vela anterior como nível de stop-loss, os riscos são controláveis

- Lógica simples, fácil de implementar e otimizar

- Adequada para uso em mercados com tendência

Riscos da Estratégia

- Podem ocorrer casos em que um sinal de compra é seguido por um recuo imediato que aciona o stop-loss

- Para instrumentos de alta volatilidade, o nível de stop-loss pode ser definido muito próximo ao preço de compra, levando a saídas prematuras

- Falta de metas de lucro, dificultando a determinação do momento ideal de saída

Direções de Otimização da Estratégia

- Combinar com outros indicadores como MA, MACD, etc., para confirmar a força da tendência e melhorar a eficácia dos sinais de entrada

- Para instrumentos de alta volatilidade, definir o nível de stop-loss em uma posição mais distante, como o ponto mais baixo das N velas anteriores, para reduzir a frequência de stop-loss

- Introduzir metas de lucro, como N vezes o ATR ou ganhos percentuais, para travar lucros de forma oportuna

- Considerar a adição de gerenciamento de posição, como ajustar o tamanho da posição com base na força do sinal

Resumo

Esta estratégia captura lucros de forma eficaz em mercados com tendência, selecionando velas de alta sem pavio superior para entrada e usando o mínimo da vela anterior para stop-loss. No entanto, a estratégia também apresenta certas limitações, como posicionamento inflexível do stop-loss e falta de metas de lucro. Melhorias podem ser feitas introduzindo outros indicadores para filtrar sinais, otimizando as posições de stop-loss e definindo metas de lucro para tornar a estratégia mais robusta e eficaz.

- 1