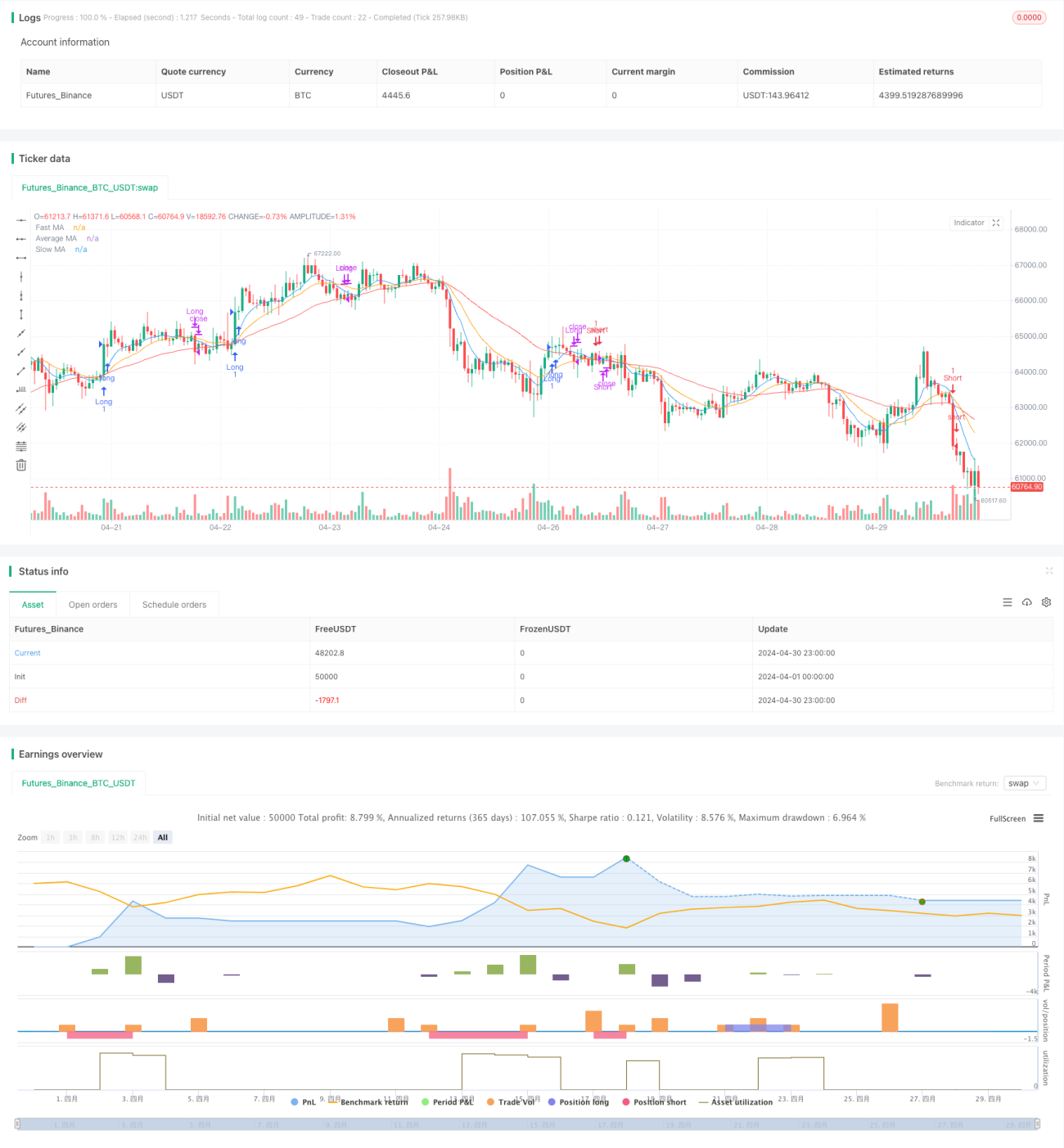

Estratégia de rejeição de média móvel com base no filtro de índice direcional médio

Visão geral

A estratégia usa várias médias móveis ((MA) como principal sinal de negociação e combina o índice de direção média ((ADX) como filtro. A principal idéia da estratégia é identificar oportunidades potenciais de múltiplas cabeças e cabeças vazias, comparando a relação entre a MA rápida, a MA lenta e a MA média.

Princípio da estratégia

- Calcule o MA rápido, o MA lento e o MA médio.

- Identificar potenciais níveis de pluralidade e vazio, comparando a relação entre o preço de fechamento e o MA lento.

- A relação entre o preço de fechamento e o MA rápido é usada para confirmar os níveis de heads e heads vazios.

- O indicador ADX é calculado manualmente para medir a intensidade da tendência.

- Quando o MA rápido atravessa o MA médio para cima, o ADX é maior do que o limiar definido e o nível de multiplicação é confirmado, gerando um sinal de entrada multiplo.

- Quando o MA rápido atravessa o MA médio para baixo, o ADX é maior do que o limiar definido e o nível de cabeçote é confirmado, gerando um sinal de entrada de cabeçote.

- Quando o preço de fechamento atravessa a MA lenta para baixo, gera um sinal de saída de cabeça; quando o preço de fechamento atravessa a MA lenta para cima, gera um sinal de saída de cabeça vazia.

Vantagens estratégicas

- O uso de MAs múltiplos permite uma captura mais abrangente das mudanças nas tendências e dinâmicas do mercado.

- A identificação de potenciais oportunidades de negociação pode ser feita comparando a relação entre o MA rápido, o MA lento e o MA médio.

- Usando o indicador ADX como filtro, pode-se evitar a produção de muitos falsos sinais em mercados de turbulência, aumentando a confiabilidade dos sinais de negociação.

- A lógica da estratégia é clara, fácil de entender e de implementar.

Risco estratégico

- A estratégia pode gerar mais falsos sinais em situações de tendências pouco visíveis ou de turbulência no mercado, resultando em negociações frequentes e perdas.

- A estratégia depende de indicadores atrasados como MA e ADX, podendo perder algumas oportunidades de formação de tendências iniciais.

- A configuração de parâmetros de uma estratégia (como o comprimento da MA e o limiar ADX) tem um grande impacto na performance da estratégia e precisa ser otimizada de acordo com diferentes mercados e variedades.

Direção de otimização da estratégia

- Considere a introdução de outros indicadores técnicos, como RSI, MACD, etc., para aumentar a confiabilidade e a diversidade dos sinais de negociação.

- Para diferentes ambientes de mercado, pode-se definir uma combinação diferente de parâmetros para se adaptar às mudanças do mercado.

- Introduzir medidas de gestão de risco, como stop loss e gestão de posições, para controlar potenciais perdas.

- Combinado com análises fundamentais, como dados econômicos e mudanças de política, para obter uma visão mais abrangente do mercado.

Resumir

A estratégia de rejeição linear baseada no filtro do índice de direção média utiliza vários indicadores de MA e ADX para identificar oportunidades de negociação potenciais e filtrar sinais de negociação de baixa qualidade. A lógica da estratégia é clara, fácil de entender e implementar, mas na aplicação prática precisa prestar atenção às mudanças no ambiente do mercado e ser otimizada em combinação com outros indicadores técnicos e medidas de gerenciamento de risco.

- 1