Estratégia de trading de cruzamento de duas médias móveis com stop loss e take profit dinâmicos

Visão Geral

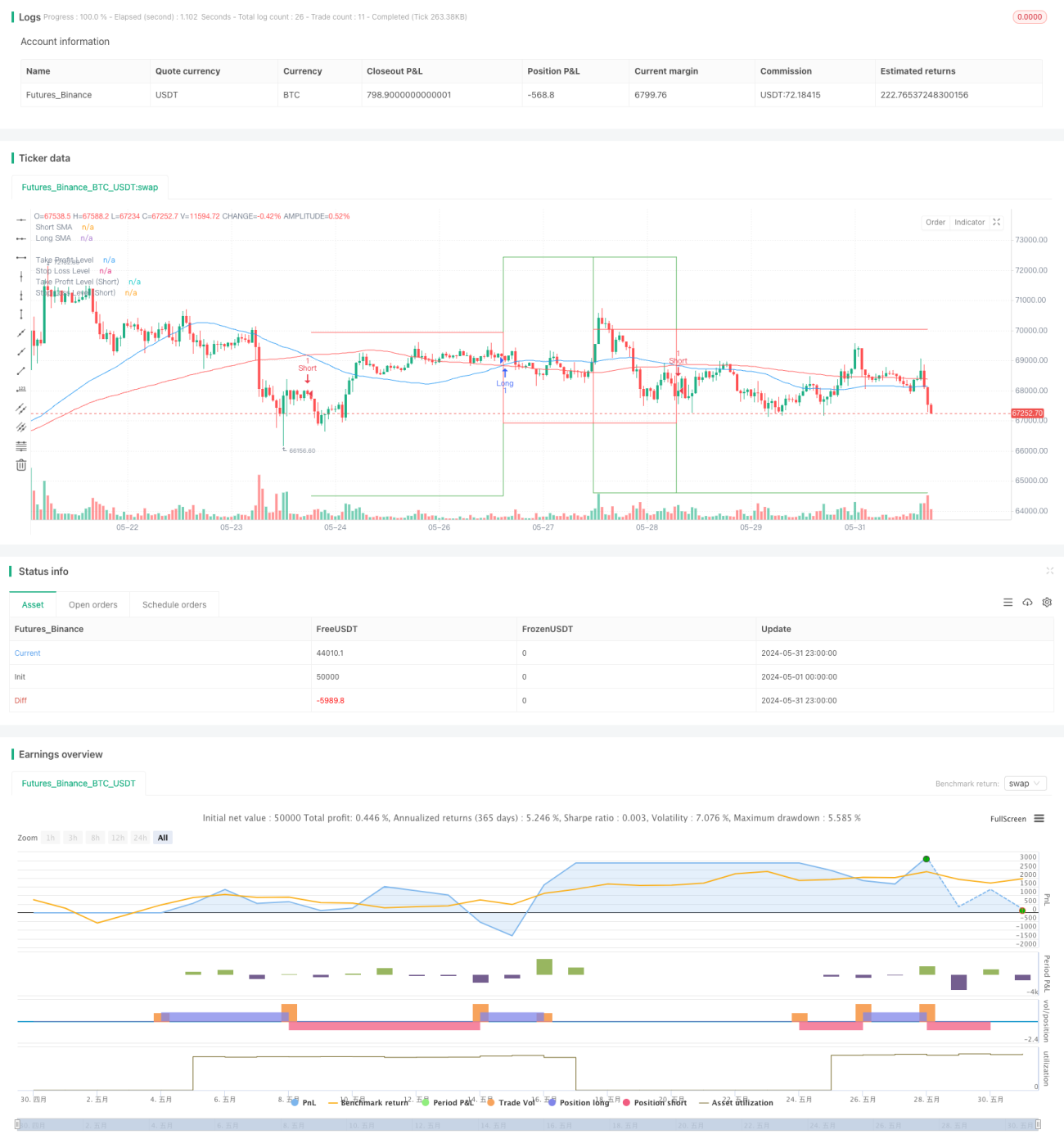

Esta estratégia é um sistema de negociação automatizado baseado no cruzamento de Médias Móveis Simples (SMA), combinado com mecanismos dinâmicos de take profit e stop loss. Utiliza duas SMAs de períodos diferentes, gerando sinais de compra e venda a partir de seus cruzamentos. Além disso, a estratégia define níveis percentuais de take profit e stop loss para controlar riscos e proteger lucros.

Princípio da Estratégia

- Utiliza duas SMAs: uma de curto prazo (50 períodos) e uma de longo prazo (100 períodos).

- Quando a SMA de curto prazo cruza acima da SMA de longo prazo, gera um sinal de compra; quando a SMA de curto prazo cruza abaixo da SMA de longo prazo, gera um sinal de venda.

- Ao abrir uma posição, os níveis de take profit e stop loss são calculados com base no preço atual e em percentuais predefinidos.

- Quando o preço atinge o nível de take profit ou stop loss, a posição é automaticamente encerrada.

- A estratégia marca os sinais de compra e venda no gráfico e desenha linhas de take profit e stop loss.

Vantagens da Estratégia

- Simples e compreensível: O cruzamento de duas médias móveis é um método clássico de análise técnica, fácil de entender e implementar.

- Seguidora de tendência: Capaz de capturar tendências de médio e longo prazo, favorecendo ganhos em grandes movimentos.

- Gerenciamento de risco: Através do ajuste dinâmico de take profit e stop loss, controla efetivamente o risco de cada operação.

- Automatizada: Executada inteiramente pelo programa, reduzindo interferência humana e influência emocional.

- Visualização: Sinaliza claramente as operações e níveis-chave no gráfico, facilitando análise e backtest.

Riscos da Estratégia

- Inadequada para mercados laterais: Em mercados de oscilação lateral, pode gerar sinais falsos frequentes, resultando em perdas consecutivas.

- Atraso: A SMA possui inércia, podendo perder o ponto ideal de entrada ou atrasar a saída.

- Percentual fixo de risco: Usar percentuais fixos de take profit e stop loss pode não ser adequado para todas as condições de mercado.

- Falta de indicadores de confirmação: Depender apenas do cruzamento de médias pode ignorar outras informações importantes do mercado.

- Não considera custos de transação: Negociações frequentes podem gerar custos elevados, impactando o resultado final.

Direções de Otimização

- Adicionar filtros: Incluir volume, volatilidade ou outros indicadores técnicos como filtros para reduzir sinais falsos.

- Ajustar dinamicamente os períodos da SMA: Adaptar automaticamente o comprimento das SMAs conforme a volatilidade do mercado para se adequar a diferentes ambientes.

- Otimizar take profit e stop loss: Considerar o uso do ATR (Average True Range) para definir níveis dinâmicos, melhor adaptação à volatilidade.

- Aumentar confirmação de tendência: Combinar outros indicadores de tendência, como MACD ou ADX, para aumentar a confiabilidade dos sinais.

- Incluir gerenciamento de posição: Ajustar o tamanho de cada posição conforme o tamanho da conta e a volatilidade do mercado.

- Filtro de tempo: Adicionar restrições de janela de negociação, evitando períodos de alta volatilidade ou baixa liquidez.

- Controle de drawdown: Limitar o drawdown máximo, pausando a negociação após uma sequência de perdas.

Resumo

Esta estratégia baseada no cruzamento de duas médias móveis oferece uma estrutura simples e eficaz, ideal para iniciantes em negociação automatizada. Ela combina elementos de seguimento de tendência e gerenciamento de risco, protegendo o capital através de take profit e stop loss dinâmicos. No entanto, para obter melhores resultados em negociações reais, são necessárias otimizações e melhorias adicionais. Pode-se considerar adicionar mais indicadores técnicos como filtros, otimizar os métodos de definição de take profit e stop loss, e introduzir estratégias mais complexas de gerenciamento de posição. Além disso, realizar backtests e validações abrangentes em diferentes condições de mercado e prazos é essencial. Com aperfeiçoamento contínuo e adaptação às mudanças do mercado, esta estratégia tem potencial para se tornar um sistema de negociação confiável.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Pubgentleman

//@version=5- 1