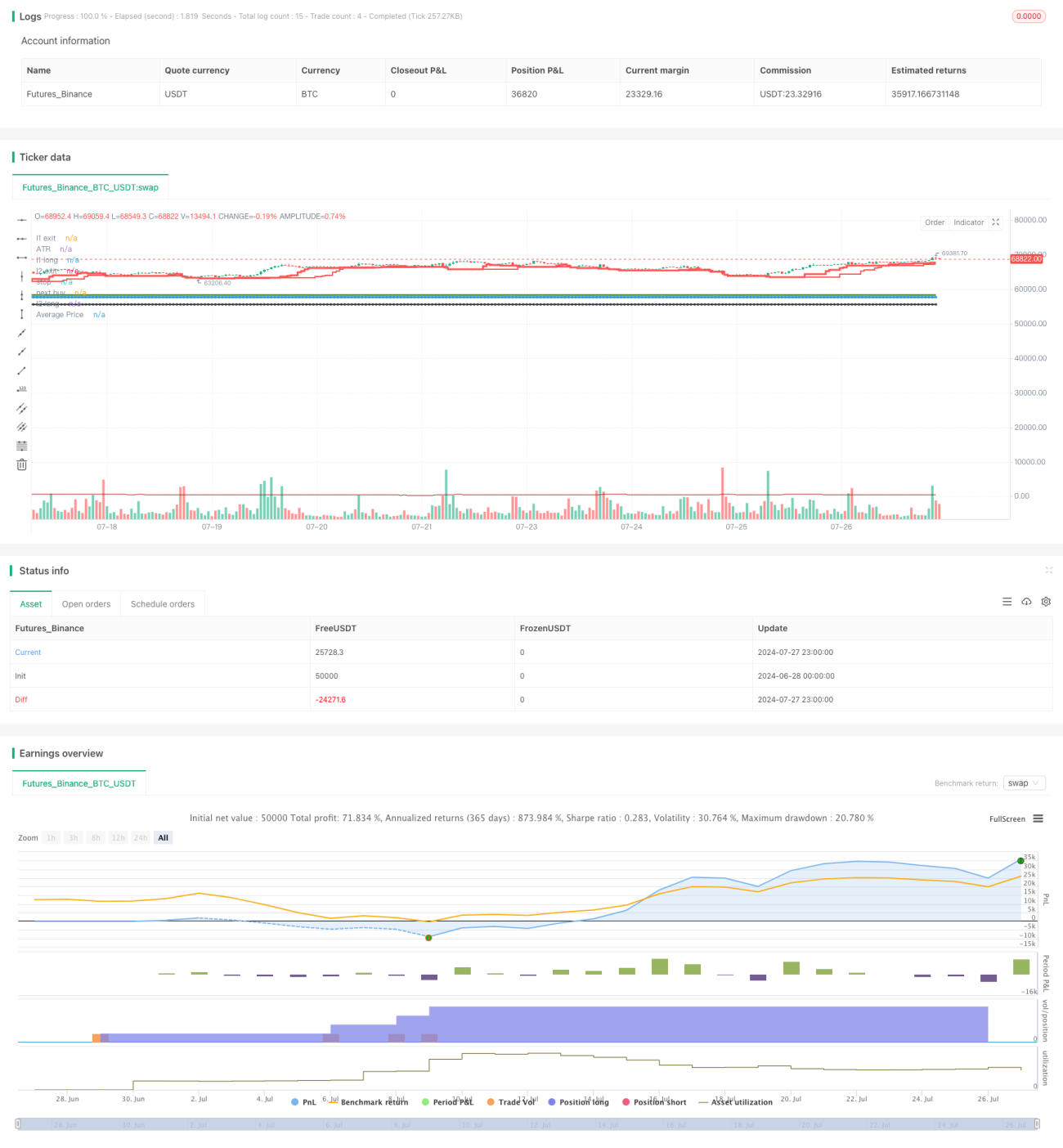

Sistema de Seguimento de Tendência Dinâmico de Múltiplos Níveis

Visão Geral

O sistema de acompanhamento de tendência dinâmica em múltiplos níveis é uma estratégia aprimorada baseada nas Regras da Tartaruga. Esta estratégia utiliza sinais de tendência de múltiplos períodos de tempo, combinados com stop loss dinâmico e adição em pirâmide, para capturar tendências de médio e longo prazo. O sistema define dois períodos de acompanhamento de tendência (L1 e L2) para capturar tendências de diferentes velocidades e usa o indicador ATR adaptativo para ajustar dinamicamente as posições de entrada, adição e stop loss. Este design de múltiplos níveis permite que a estratégia mantenha estabilidade em diferentes condições de mercado, ao mesmo tempo que maximiza o potencial de lucro através da adição em pirâmide.

Princípio da Estratégia

-

Identificação de Tendência: Utiliza dois períodos de médias móveis (L1 e L2) para identificar tendências de diferentes velocidades. L1 é usado para capturar tendências mais rápidas, enquanto L2 é usado para capturar tendências mais lentas, mas mais confiáveis.

-

Sinal de Entrada: Quando o preço ultrapassa o ponto alto de L1 ou L2, é gerado um sinal de compra. Se a última negociação baseada em L1 foi lucrativa, o próximo sinal de L1 é ignorado até que apareça um sinal de L2.

-

Stop Loss Dinâmico: Usa um múltiplo do ATR (padrão de 3 vezes) como distância inicial do stop loss. À medida que o tempo de posição aumenta, o stop loss é gradualmente elevado.

-

Adição em Pirâmide: Durante a continuação da tendência, a cada aumento de 0,5 ATR no preço, uma nova posição é adicionada, com um máximo de 5 adições.

-

Controle de Risco: O risco de cada negociação não excede 2% do patrimônio líquido da conta, calculado dinamicamente através do tamanho da posição.

-

Mecanismo de Saída: A posição é fechada quando o preço cai abaixo da mínima de 10 dias (L1) ou da mínima de 20 dias (L2), ou quando a linha de stop loss móvel é acionada.

Vantagens da Estratégia

-

Captura de Tendência em Múltiplos Níveis: Através dos dois períodos L1 e L2, é possível capturar tanto tendências rápidas quanto tendências de longo prazo, melhorando a adaptabilidade e estabilidade da estratégia.

-

Gerenciamento de Risco Dinâmico: Utiliza o ATR como indicador de volatilidade, permitindo ajustes dinâmicos nas posições de entrada, adição e stop loss, adaptando-se melhor às mudanças do mercado.

-

Adição em Pirâmide: Adiciona posições gradualmente durante a continuação da tendência, controlando o risco ao mesmo tempo que maximiza o potencial de lucro.

-

Parâmetros Flexíveis: Múltiplos parâmetros ajustáveis permitem que a estratégia se adapte a diferentes mercados e estilos de negociação.

-

Execução Automatizada: A estratégia pode ser totalmente automatizada, reduzindo a intervenção humana e a influência emocional.

Riscos da Estratégia

-

Risco de Reversão de Tendência: Tem bom desempenho em mercados com tendências fortes, mas pode gerar negociações frequentes e perdas em mercados laterais.

-

Slippage e Custos de Transação: As adições frequentes e o stop loss móvel podem resultar em custos de transação elevados.

-

Risco de Sobre-Otimização: A grande quantidade de parâmetros pode levar a um ajuste excessivo aos dados históricos.

-

Risco de Gerenciamento de Capital: Se o capital inicial for pequeno, pode ser difícil executar múltiplas adições de forma eficaz.

-

Risco de Liquidez de Mercado: Em mercados com baixa liquidez, pode ser difícil executar negociações ao preço ideal.

Direções de Otimização da Estratégia

-

Introduzir Filtro de Ambiente de Mercado: Adicionar indicadores de força de tendência (como ADX) para avaliar o ambiente de mercado, reduzindo a frequência de negociações em mercados laterais.

-

Otimizar Estratégia de Adição: Considerar o ajuste dinâmico do intervalo e número de adições com base na força da tendência, em vez de um intervalo fixo de 0,5 ATR e 5 adições.

-

Introduzir Mecanismo de Take Profit: Em tendências de longo prazo, definir take profit parcial para garantir lucros, por exemplo, fechando metade da posição quando o lucro atinge 3 vezes o ATR.

-

Análise de Correlação entre Múltiplos Ativos: Ao aplicar em portfólios, adicionar análise de correlação entre ativos para otimizar a relação risco-retorno geral.

-

Adicionar Filtro de Volatilidade: Em períodos de volatilidade extremamente alta, pausar as negociações ou ajustar os parâmetros de risco para lidar com condições anormais de mercado.

-

Otimizar Mecanismo de Saída: Considerar o uso de indicadores de saída mais flexíveis, como o Parabolic SAR ou o Chandelier Exit.

Resumo

O sistema de acompanhamento de tendência dinâmica em múltiplos níveis é uma estratégia abrangente que combina as clássicas Regras da Tartaruga com técnicas quantitativas modernas. Através da identificação de tendência em múltiplos níveis, gerenciamento de risco dinâmico e adição em pirâmide, esta estratégia melhora a capacidade de capturar tendências e o potencial de lucro, mantendo a robustez. Embora enfrente desafios em mercados laterais, com uma otimização adequada de parâmetros e controle de risco, a estratégia pode manter um desempenho estável em diferentes condições de mercado. Melhorias futuras podem incluir a introdução de avaliação do ambiente de mercado, otimização dos mecanismos de adição e saída, a fim de aumentar a robustez e a lucratividade da estratégia.

- 1