Estratégia de Posicionamento Overnight de Tendência Long/Short Cross-Market Baseada no Indicador EMA

Esta estratégia é uma estratégia de posicionamento noturno entre mercados baseada no indicador técnico EMA, com o objetivo de capturar oportunidades de negociação antes do fechamento e após a abertura dos mercados. Através de um controle preciso do tempo e filtragem por indicadores técnicos, realiza operações inteligentes em diferentes ambientes de mercado.

Visão Geral da Estratégia

A estratégia busca obter lucros ao entrar no mercado em um horário específico antes do fechamento e sair em um horário fixo após a abertura no dia seguinte. Combinando o indicador EMA como confirmação de tendência, identifica oportunidades de negociação em múltiplos mercados globais. A estratégia também integra funções de negociação automatizada, permitindo operação não supervisionada.

Princípio da Estratégia

- Controle de Tempo: Com base nos horários de negociação de diferentes mercados, entra em um horário fixo antes do fechamento e sai em um horário fixo após a abertura.

- Filtro EMA: Utiliza o indicador EMA opcional para validar os sinais de entrada.

- Seleção de Mercado: Suporta adaptação automática aos horários de negociação dos mercados dos EUA, Ásia e Europa.

- Proteção de Fim de Semana: Força o fechamento das posições antes do fechamento de sexta-feira, evitando o risco de manter posições durante o fim de semana.

Vantagens da Estratégia

- Adaptabilidade a Múltiplos Mercados: Permite ajustar flexivelmente os horários de negociação de acordo com as características de cada mercado.

- Controle de Risco Completo: Inclui mecanismo de proteção de fechamento no fim de semana.

- Alto Grau de Automação: Suporta integração com interfaces de negociação automática.

- Parâmetros Flexíveis e Ajustáveis: Horários de negociação e parâmetros de indicadores técnicos podem ser personalizados.

- Consideração de Custos de Negociação: Inclui configurações de taxas e slippage.

Riscos da Estratégia

- Risco de Volatilidade do Mercado: O posicionamento noturno pode enfrentar riscos de gap.

- Dependência Temporal: A eficácia da estratégia é influenciada pela escolha do período de mercado.

- Limitação do Indicador Técnico: Um único indicador EMA pode apresentar atraso.

Sugestão: Definir limites de stop loss e adicionar mais validações com indicadores técnicos.

Direções de Otimização da Estratégia

- Adicionar mais combinações de indicadores técnicos.

- Introduzir mecanismo de filtragem por volatilidade.

- Otimizar a escolha dos horários de entrada e saída.

- Incluir função de ajuste adaptativo de parâmetros.

- Reforçar o módulo de controle de risco.

Resumo

Esta estratégia, através de controle preciso de tempo e filtragem por indicadores técnicos, constrói um sistema confiável de negociação noturna. O design da estratégia considera de forma abrangente as necessidades reais de negociação, incluindo adaptabilidade a múltiplos mercados, controle de risco, automação de negociação, etc., possuindo alto valor prático. Com otimização e aprimoramento contínuos, a estratégia tem potencial para gerar retornos estáveis em negociações ao vivo.

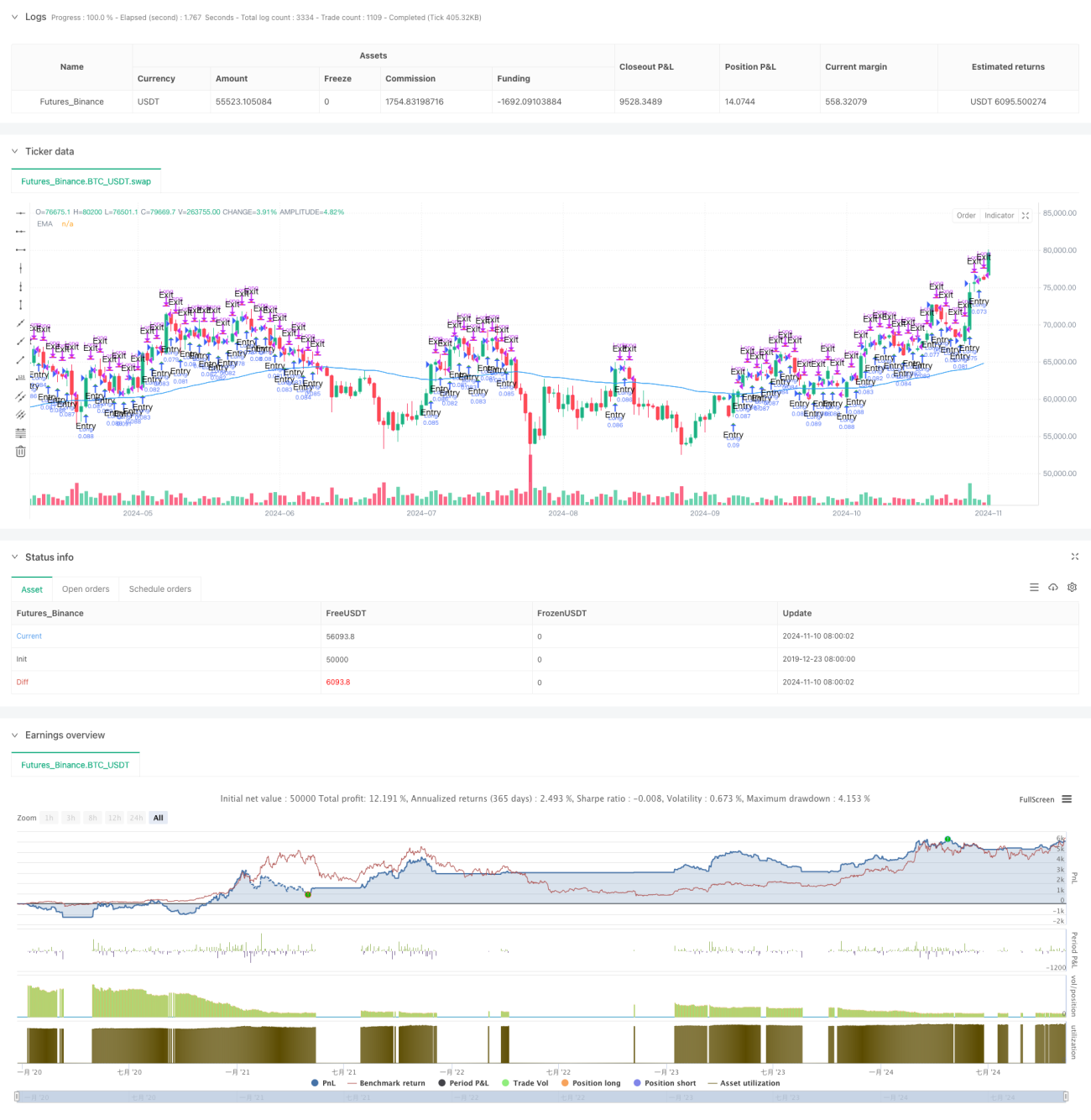

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy, titled "Overnight Market Entry Strategy with EMA Filter," is designed for entering long positions shortly before - 1