Sistema de negociação inteligente e adaptativo baseado no momentum do RSI e stop loss/take profit multinível

Visão Geral

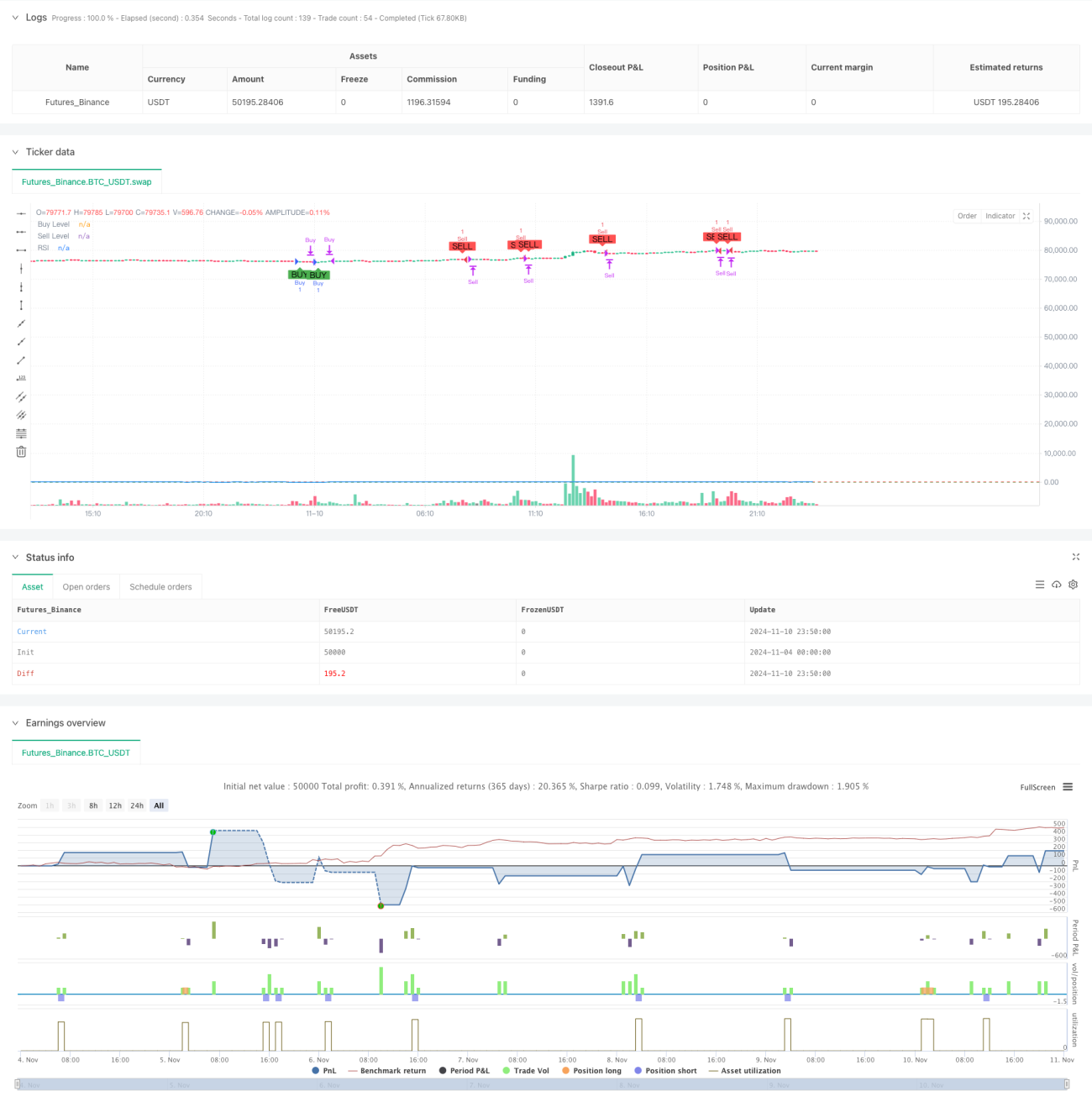

Esta estratégia é um sistema de negociação adaptativo baseado no Índice de Força Relativa (RSI), que captura as mudanças de momentum do mercado através da monitorização das zonas de sobrecompra e sobrevenda do indicador RSI. O sistema integra um mecanismo inteligente de gestão de posições, incluindo controlo de take profit e stop loss em vários níveis, bem como uma função de fecho automático, visando alcançar uma relação risco-retorno robusta.

Princípio da Estratégia

O núcleo da estratégia assenta nos sinais de sobrecompra e sobrevenda do indicador RSI, combinando múltiplas condições de negociação:

- Sinal de entrada: quando o RSI ultrapassa o nível 30, gera um sinal de compra; quando o RSI cai abaixo do nível 70, gera um sinal de venda.

- Gestão de risco:

- Define stop loss fixo (perda de 100 pontos) e alvo de lucro (ganho de 150 pontos)

- Monitoriza em tempo real o estado das posições, garantindo posições unidirecionais

- Fecho automático de posições às 15:25 diariamente para evitar risco noturno

- Execução das negociações: o sistema executa automaticamente as ordens de negociação através das funções strategy.entry e strategy.close

Vantagens da Estratégia

- Sinais claros: os sinais de cruzamento baseados no RSI são nítidos, fáceis de compreender e executar

- Controlo de risco completo: integra mecanismos de controlo de risco em múltiplos níveis

- Elevado grau de automação: desde a geração de sinais até à execução das negociações, tudo é automatizado

- Boa visualização: exibe claramente os sinais de compra/venda e as linhas de nível do RSI no gráfico

- Adaptabilidade: permite ajustar parâmetros de acordo com diferentes características do mercado

Riscos da Estratégia

- O atraso do sinal RSI pode causar atraso no momento de entrada

- Os níveis fixos de stop loss e take profit podem não ser adequados para todos os ambientes de mercado

- A dependência de um único indicador pode perder outros sinais importantes do mercado

- Negociações frequentes podem gerar custos de transação elevados

Sugestões:

- Combinar com outros indicadores técnicos para confirmação dos sinais

- Ajustar dinamicamente os níveis de stop loss e take profit

- Aumentar a limitação da frequência de negociação

Direções de Otimização da Estratégia

- Otimização de indicadores:

- Adicionar indicadores de tendência, como médias móveis

- Adicionar indicadores de volume para confirmar sinais

- Otimização do controlo de risco:

- Implementar stop loss e take profit dinâmicos

- Adicionar controlo de drawdown máximo

- Otimização da execução:

- Adicionar gestão do tamanho das posições

- Otimizar a gestão do tempo de negociação

- Otimização de parâmetros:

- Desenvolver um sistema de parâmetros adaptativos

- Implementar limiares dinâmicos do RSI

Resumo

Esta estratégia captura as mudanças de momentum do mercado através do indicador RSI, combinada com um sistema de gestão de risco completo, resultando num sistema de negociação totalmente automatizado. Embora apresente algumas limitações, após melhorias com base nas direções de otimização sugeridas, é expectável obter um desempenho de negociação mais estável. A principal vantagem da estratégia reside na integridade do sistema e no grau de automação, sendo adequada como estrutura base para desenvolvimento e otimização adicionais.

- 1