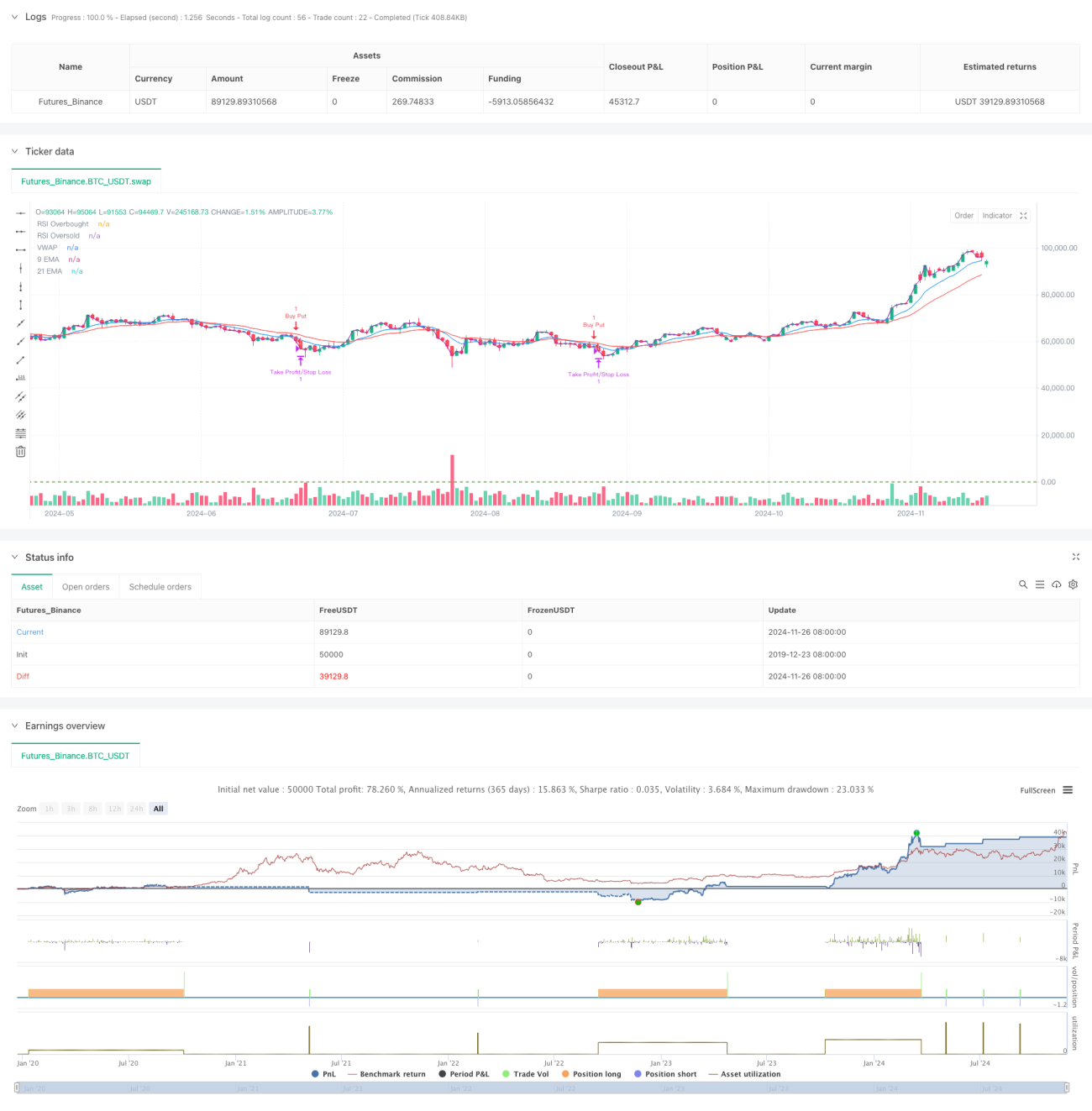

Visão Geral

Esta estratégia é um sistema de negociação de alta frequência baseado em múltiplos indicadores técnicos, utilizando um timeframe de 5 minutos, combinando sistemas de médias móveis, indicadores de momentum e análise de volume. A estratégia se adapta dinamicamente às flutuações do mercado, utilizando múltiplas confirmações de sinais para aumentar a precisão e a confiabilidade das negociações. O núcleo da estratégia está na combinação de indicadores técnicos multidimensionais para capturar tendências de curto prazo do mercado, ao mesmo tempo que usa stops dinâmicos para gerenciar o risco.

Princípio da Estratégia

A estratégia utiliza um sistema de dupla média móvel (EMA de 9 e 21 períodos) como principal ferramenta de julgamento de tendência, combinada com o indicador RSI para confirmação de momentum. Quando o preço está acima das duas médias móveis e o RSI está na faixa de 40-65, o sistema procura oportunidades de compra; quando o preço está abaixo das duas médias móveis e o RSI está na faixa de 35-60, o sistema procura oportunidades de venda. Simultaneamente, a estratégia introduz um mecanismo de confirmação de volume, exigindo que o volume atual seja 1,2 vezes maior que a média móvel de 20 períodos. O uso do VWAP garante ainda que a direção da negociação esteja alinhada com a tendência intradiária predominante.

Vantagens da Estratégia

- O mecanismo de múltiplas confirmações de sinais aumenta significativamente a confiabilidade das negociações.

- Configurações dinâmicas de take profit e stop loss se adaptam a diferentes condições de mercado.

- Utiliza limites de RSI mais conservadores, evitando negociações em zonas extremas.

- O mecanismo de confirmação de volume filtra efetivamente sinais falsos.

- O uso do VWAP ajuda a garantir que a direção da negociação esteja alinhada com o fluxo de capital dominante.

- O sistema de médias móveis de resposta rápida é adequado para capturar oportunidades de curto prazo.

Riscos da Estratégia

- Em mercados laterais (congestionados), pode gerar sinais falsos frequentes.

- A restrição de múltiplas condições pode levar à perda de algumas oportunidades de negociação.

- Negociações de alta frequência podem enfrentar custos de transação elevados.

- Pode reagir lentamente em mudanças rápidas de direção do mercado.

- Exige alta precisão nos dados de mercado em tempo real.

Direções de Otimização da Estratégia

- Introduzir um mecanismo de ajuste adaptativo de parâmetros, permitindo que a estratégia ajuste dinamicamente os parâmetros dos indicadores conforme as condições do mercado.

- Adicionar um módulo de identificação de ambiente de mercado, adotando diferentes estratégias de negociação sob diferentes condições.

- Otimizar o filtro de volume, considerando o uso de volume relativo ou análise de perfil de volume.

- Aprimorar o mecanismo de stop loss, considerando a adição de uma função de trailing stop.

- Adicionar filtro de horário de negociação, evitando períodos de alta volatilidade na abertura e no fechamento do mercado.

Conclusão

Esta estratégia constrói um sistema de negociação relativamente completo por meio da combinação de múltiplos indicadores técnicos. Sua vantagem está no mecanismo de confirmação de sinais multidimensionais e no método dinâmico de gerenciamento de risco. Embora existam alguns riscos potenciais, a estratégia ainda possui bom valor de aplicação com uma otimização adequada de parâmetros e gerenciamento de risco. Recomenda-se que os traders realizem backtests completos antes do uso em conta real e ajustem os parâmetros conforme as condições específicas do mercado.

- 1