Estratégia Avançada de Detecção de Gap de Valor Justo Baseada em Gestão de Risco Dinâmica e Lucro Fixo

Visão Geral

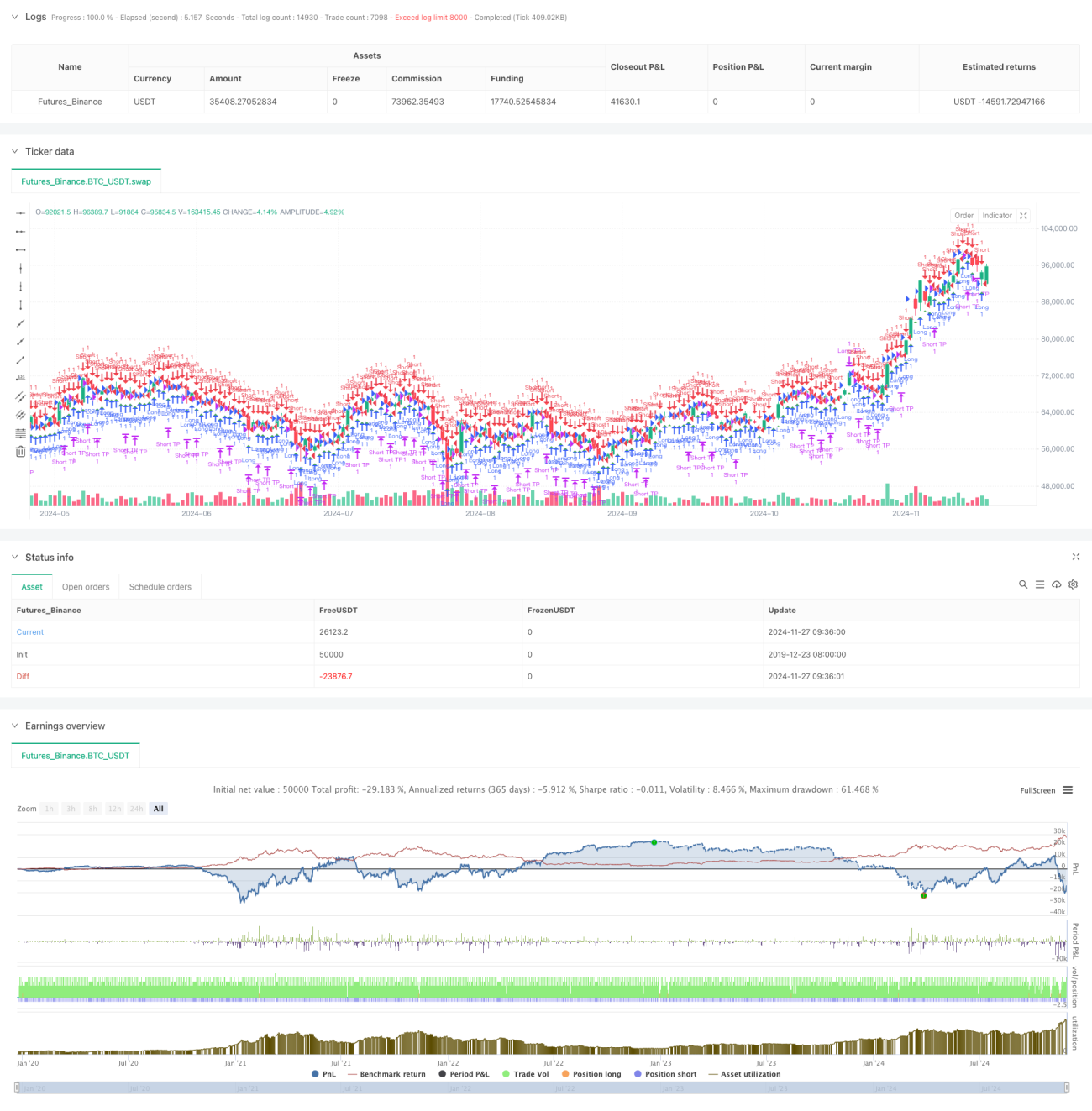

Esta é uma estratégia de negociação baseada no Gap de Valor Justo (FVG - Fair Value Gap), combinando gestão de risco dinâmica com metas de lucro fixas. A estratégia opera no período de 15 minutos, identificando gaps de preço no mercado para capturar oportunidades potenciais de negociação. De acordo com os dados de backtest, entre novembro de 2023 e agosto de 2024, a estratégia alcançou um retorno líquido de 284,40%, totalizando 153 negociações, com uma taxa de lucro de 71,24% e um fator de lucro de 2,422.

Princípio da Estratégia

O núcleo da estratégia é identificar gaps de valor justo monitorando a relação de preços entre três candles consecutivos. Especificamente:

- Condição de formação de FVG de alta: quando a máxima do candle anterior é menor que a mínima dos dois candles anteriores

- Condição de formação de FVG de baixa: quando a mínima do candle anterior é maior que a máxima dos dois candles anteriores

- O sinal de entrada é controlado pelo parâmetro de limiar do FVG, acionado apenas quando o tamanho do gap excede uma certa porcentagem do preço

- O controle de risco utiliza uma porcentagem fixa (1%) do patrimônio da conta como padrão de stop loss

- A meta de lucro é definida em um número fixo de pontos (50 pontos)

Vantagens da Estratégia

- Gestão de risco científica e razoável: utiliza stop loss baseado em porcentagem do patrimônio da conta, permitindo controle de risco dinâmico

- Regras de negociação claras: utiliza meta de lucro fixa, evitando julgamentos subjetivos

- Desempenho excelente: alta taxa de lucro e fator de lucro indicam boa estabilidade da estratégia

- Implementação simples: lógica de código clara, fácil de entender e manter

- Adaptabilidade: pode ser ajustada por parâmetros para se adaptar a diferentes condições de mercado

Riscos da Estratégia

- Risco de volatilidade do mercado: em mercados de alta volatilidade, a meta de lucro fixa em pontos pode ser pouco flexível

- Risco de slippage: negociações frequentes podem gerar altos custos de slippage

- Dependência de parâmetros: o desempenho da estratégia depende fortemente da configuração do limiar do FVG

- Risco de falso rompimento: alguns sinais de FVG podem ser falsos rompimentos, exigindo indicadores de confirmação adicionais

- Risco de gestão de capital: o stop loss em porcentagem fixa pode levar a uma rápida redução do capital em caso de perdas consecutivas

Direções de Otimização da Estratégia

- Introduzir indicadores de volatilidade do mercado para ajustar dinamicamente a meta de lucro

- Adicionar filtro de tendência para evitar negociações em mercados laterais

- Desenvolver mecanismo de confirmação de múltiplos períodos de tempo

- Otimizar o algoritmo de gestão de posição, introduzindo sistema de posição variável

- Adicionar filtro de horário de negociação, evitando períodos de alta volatilidade

- Desenvolver sistema de pontuação de intensidade de sinal para selecionar oportunidades de negociação de alta qualidade

Resumo

Esta estratégia, ao combinar a teoria do gap de valor justo com métodos científicos de gestão de risco, demonstrou bons resultados de negociação. A alta taxa de lucro e o fator de lucro estável indicam seu valor prático. Através das direções de otimização sugeridas, a estratégia ainda tem espaço para melhoria. Recomenda-se que os traders realizem uma otimização completa de parâmetros e validação por backtest antes de usar em conta real.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1