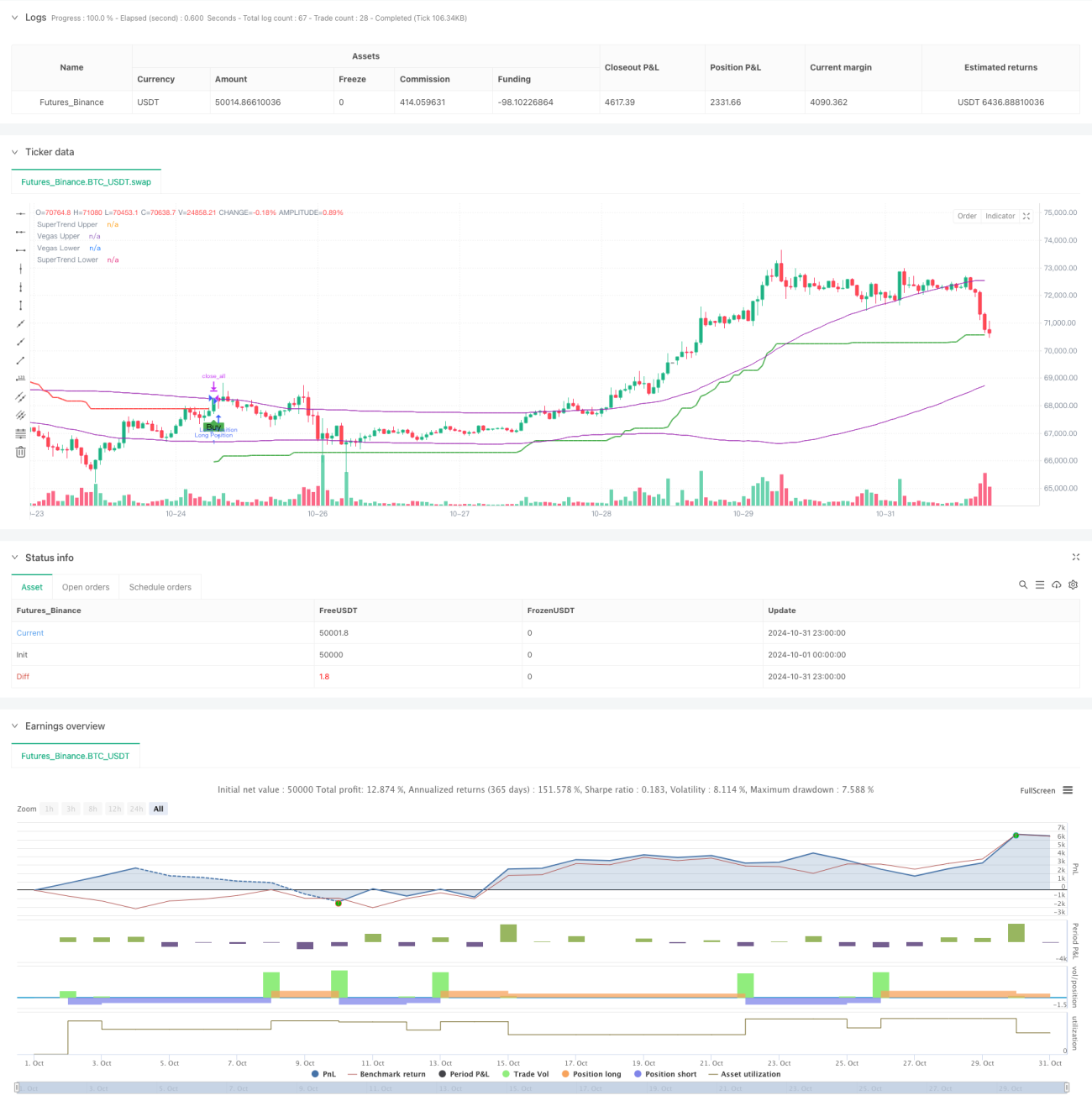

Estratégia de SuperTrend Dinâmico Adaptativo de Volatilidade Multi-Etapa

Visão Geral

A Estratégia de Super Tendência Dinâmica Adaptativa de Volatilidade em Múltiplas Etapas é um sistema de negociação inovador que combina o Canal Vegas e o indicador SuperTrend. Sua singularidade reside na capacidade de adaptação dinâmica à volatilidade do mercado, bem como no uso de um mecanismo de take-profit em múltiplas etapas para otimizar a relação risco-retorno. A estratégia integra a análise de volatilidade do Canal Vegas com a funcionalidade de acompanhamento de tendência do SuperTrend, ajustando automaticamente seus parâmetros conforme as condições do mercado mudam, gerando assim sinais de negociação mais precisos.

Princípio da Estratégia

A operação da estratégia baseia-se em três componentes principais: cálculo do Canal Vegas, detecção de tendência e mecanismo de take-profit em múltiplas etapas. O Canal Vegas utiliza a Média Móvel Simples (SMA) e o Desvio Padrão (STD) para definir a faixa de oscilação dos preços, enquanto o indicador SuperTrend determina a direção da tendência com base no valor ajustado do ATR. Quando a tendência do mercado muda, o sistema gera sinais de negociação. O mecanismo de take-profit em múltiplas etapas permite saídas graduais em diferentes níveis de preço, garantindo lucros e permitindo que parte da posição continue a obter ganhos potenciais. O diferencial da estratégia está no fator de ajuste de volatilidade, que modifica dinamicamente o multiplicador do SuperTrend com base na largura do Canal Vegas.

Vantagens da Estratégia

- Adaptabilidade Dinâmica: Por meio do fator de ajuste de volatilidade, a estratégia se adapta automaticamente a diferentes condições de mercado.

- Gestão de Risco: O mecanismo de take-profit em múltiplas etapas oferece uma solução sistematizada para realização de lucros.

- Personalização: Disponibiliza diversas opções de configuração de parâmetros para atender diferentes estilos de negociação.

- Cobertura Abrangente do Mercado: Suporta operações tanto de compra quanto de venda.

- Feedback Visual: Oferece uma interface gráfica clara para facilitar a análise e a tomada de decisão.

Riscos da Estratégia

- Sensibilidade a Parâmetros: Diferentes combinações de parâmetros podem levar a desempenhos significativamente distintos.

- Atraso: Indicadores baseados em médias móveis apresentam certo atraso.

- Risco de Falsos Rompimentos: Em mercados laterais, podem ser gerados sinais incorretos.

- Trade-off na Definição do Take-Profit: Take-profit precoce pode perder grandes tendências; take-profit tardio pode sacrificar lucros já obtidos.

Direções de Otimização da Estratégia

- Introduzir um filtro de ambiente de mercado para ajustar os parâmetros da estratégia conforme as condições do mercado.

- Adicionar análise de volume para melhorar a confiabilidade dos sinais.

- Desenvolver um mecanismo de take-profit adaptativo que ajuste dinamicamente os níveis de take-profit com base na volatilidade.

- Integrar outros indicadores técnicos para fornecer confirmação de sinais.

- Implementar gerenciamento dinâmico de posição, ajustando o tamanho da negociação conforme o risco de mercado.

Resumo

A Estratégia de Super Tendência Dinâmica Adaptativa de Volatilidade em Múltiplas Etapas representa uma abordagem avançada de negociação quantitativa. Ao combinar múltiplos indicadores técnicos e um mecanismo inovador de take-profit, oferece aos traders um sistema de negociação abrangente. Sua adaptabilidade dinâmica e funcionalidades de gestão de risco a tornam particularmente adequada para operar em diferentes ambientes de mercado, com boa escalabilidade e espaço para otimização. Com aprimoramentos e otimizações contínuos, essa estratégia tem potencial para proporcionar um desempenho de negociação mais estável no futuro.

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Multi-Step Vegas SuperTrend - strategy [presentTrading]", shorttitle="Multi-Step Vegas SuperTrend - strategy [presentTrading]", overlay=true, precision=3, commission_value=0.1, commission_type=strategy.commission.percent, slippage=1, currency=currency.USD)

// Input settings allow the user to customize the strategy's parameters.- 1