Sistema de Negociação de Rastreamento de Média Móvel com Momentum Híbrido de Dupla Cadeia

Visão Geral

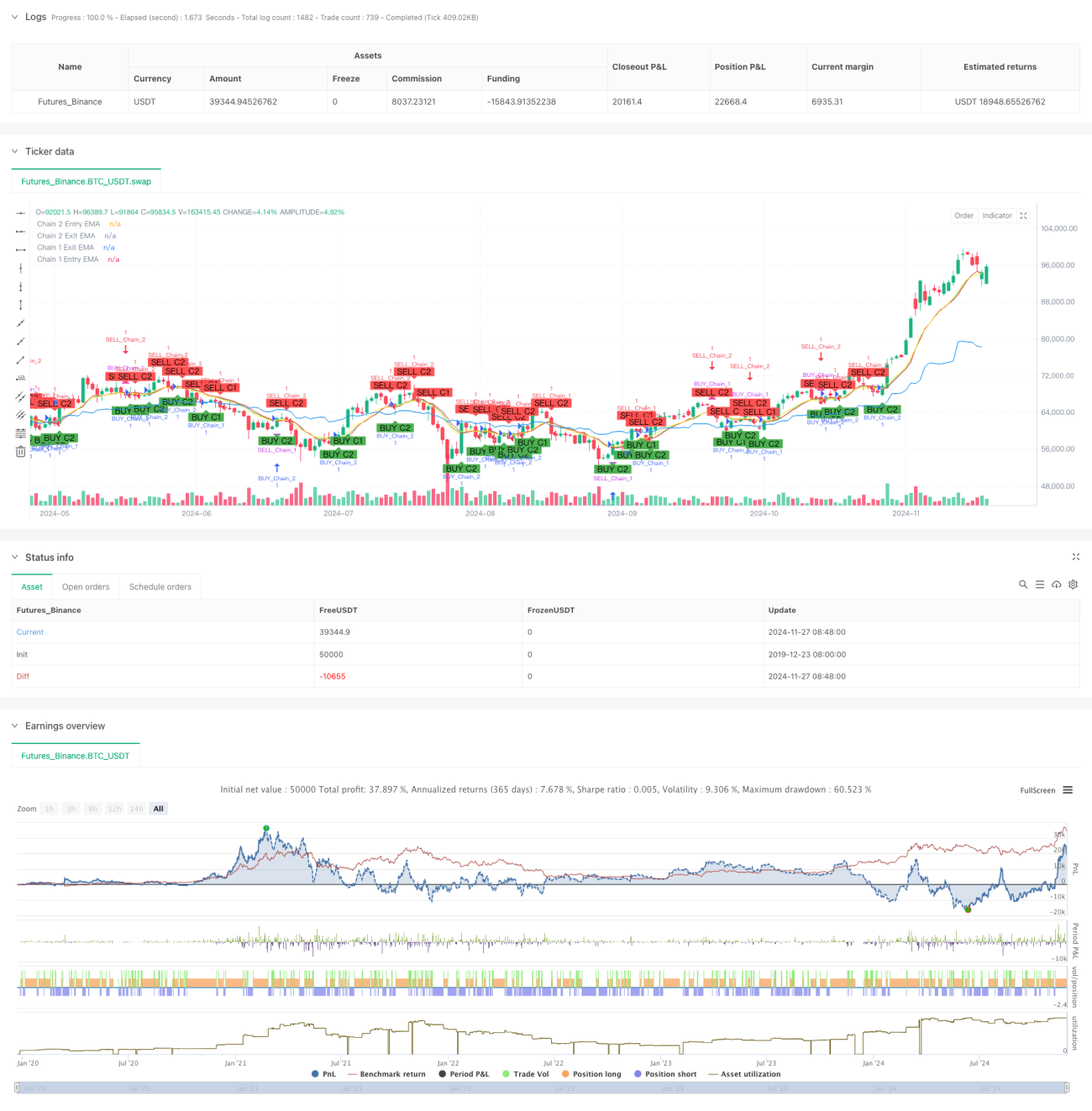

Esta estratégia é um sistema de negociação inovador baseado em Médias Móveis Exponenciais (EMA), que captura oportunidades de mercado através de duas cadeias de negociação independentes configuradas em diferentes períodos de tempo. A estratégia integra as vantagens do acompanhamento de tendência de longo prazo e do momentum de curto prazo, gerando sinais de negociação a partir de cruzamentos de EMA em múltiplos períodos de tempo, como semanal, diário, 12 horas e 9 horas, permitindo uma análise e compreensão multidimensional do mercado.

Princípio da Estratégia

A estratégia utiliza um design de cadeia dupla, cada uma com sua lógica de entrada e saída específica:

Cadeia 1 (Tendência de Longo Prazo) utiliza períodos semanal e diário:

- Sinal de entrada: Quando o preço de fechamento cruza acima da EMA no período semanal, gera um sinal de compra.

- Sinal de saída: Quando o preço de fechamento cruza abaixo da EMA no período diário, gera um sinal de encerramento.

- Período padrão da EMA: 10 (ajustável conforme necessário).

Cadeia 2 (Momentum de Curto Prazo) utiliza períodos de 12 horas e 9 horas:

- Sinal de entrada: Quando o preço de fechamento cruza acima da EMA no período de 12 horas, gera um sinal de compra.

- Sinal de saída: Quando o preço de fechamento cruza abaixo da EMA no período de 9 horas, gera um sinal de encerramento.

- Período padrão da EMA: 9 (ajustável conforme necessário).

Vantagens da Estratégia

- Análise multidimensional do mercado: Através da combinação de diferentes períodos de tempo, compreende de forma abrangente os movimentos do mercado.

- Alta flexibilidade: As duas cadeias podem ser ativadas ou desativadas independentemente, adaptando-se a diferentes estilos de negociação.

- Controle de risco aprimorado: Utiliza confirmação em múltiplos períodos de tempo para reduzir o risco de sinais falsos.

- Parâmetros altamente ajustáveis: Tanto os períodos da EMA quanto os períodos de tempo podem ser modificados conforme necessário.

- Funcionalidade completa de backtest: Possui configuração de período para backtest integrada, facilitando a validação e otimização da estratégia.

Riscos da Estratégia

- Risco de reversão de tendência: Em mercados voláteis, pode haver atraso nos sinais.

- Risco de configuração de períodos de tempo: Diferentes mercados podem exigir combinações distintas de períodos de tempo.

- Risco de otimização de parâmetros: Otimização excessiva pode levar ao sobreajuste.

- Risco de sobreposição de sinais: Quando ambas as cadeias disparam simultaneamente, pode aumentar o risco da posição.

Recomendações de controle de risco:

- Definir stops razoáveis.

- Ajustar parâmetros com base nas características do mercado.

- Realizar backtests completos antes de operar ao vivo.

- Controlar a proporção de capital por operação.

Direções de Otimização da Estratégia

-

Otimização de filtragem de sinais:

- Adicionar mecanismo de confirmação de volume.

- Introduzir indicadores de volatilidade para filtrar sinais.

- Aumentar confirmação de força da tendência.

-

Otimização do controle de risco:

- Desenvolver mecanismos de stop dinâmico.

- Projetar sistema de gerenciamento de posição.

- Adicionar controle de drawdown.

-

Otimização dos períodos de tempo:

- Estudar combinações ótimas de períodos de tempo.

- Desenvolver mecanismos de período de tempo adaptativo.

- Adicionar reconhecimento de estado do mercado.

Resumo

O Sistema de Negociação de Média Móvel com Momentum de Cadeia Dupla, ao combinar inovadoramente estratégias de médias móveis de curto e longo prazo, realiza uma análise e compreensão multidimensional do mercado. O sistema possui design flexível, podendo ser ajustado conforme diferentes condições de mercado e estilo do trader, apresentando alta praticabilidade. Com controle de risco adequado e otimização contínua, a estratégia tem potencial para obter lucros consistentes em negociações reais. Recomenda-se que os traders realizem backtests completos e otimização de parâmetros antes de utilizar em ambiente real, a fim de alcançar o melhor desempenho de negociação.

- 1