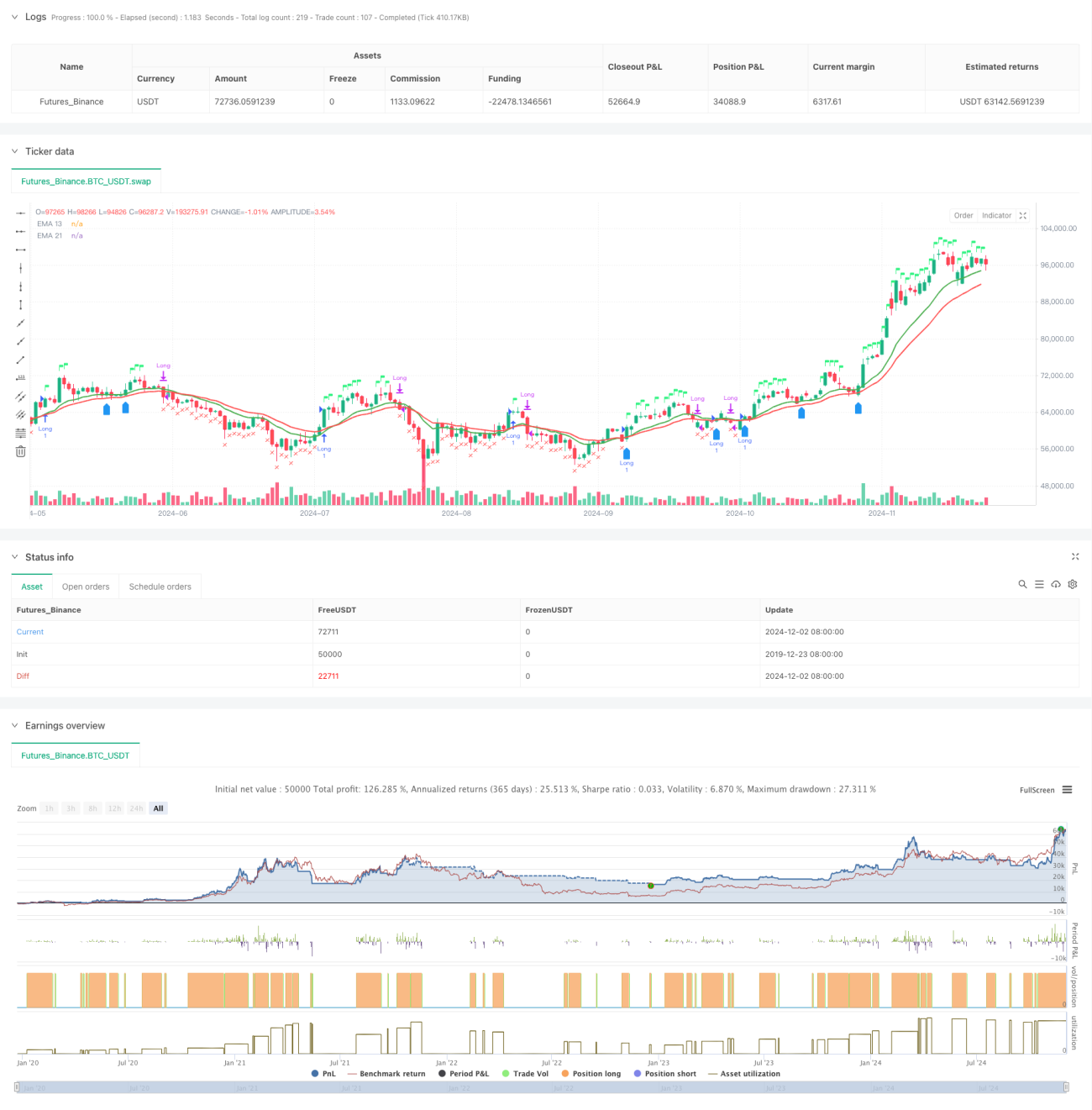

Estratégia Adaptativa Híbrida de Duas Médias Móveis e Força Relativa

Resumo

Esta estratégia é um sistema de negociação abrangente que combina o sistema de médias móveis duplas, o Índice de Força Relativa (RSI) e a análise de Força Relativa (RS). Ela confirma a tendência por meio do cruzamento das médias exponenciais de 13 e 21 períodos (EMA), ao mesmo tempo que usa o RSI e o valor RS em relação ao índice de referência para confirmar sinais de negociação, implementando um mecanismo de tomada de decisão multidimensional. A estratégia também inclui um mecanismo de controle de risco baseado nas máximas de 52 semanas e condições para reentrada.

Princípio da Estratégia

A estratégia utiliza um mecanismo de confirmação de múltiplos sinais:

- Condições de entrada devem satisfazer simultaneamente:

- EMA13 cruza acima da EMA21 ou o preço está acima da EMA13

- RSI maior que 60

- Força Relativa (RS) positiva

- Condições de saída incluem:

- Preço cai abaixo da EMA21

- RSI abaixo de 50

- RS torna-se negativo

- Condições de reentrada:

- Preço cruza acima da EMA13 e EMA13 está acima da EMA21

- RS permanece positivo

- Ou o preço ultrapassa a máxima da semana anterior

Vantagens da Estratégia

- O mecanismo de confirmação de múltiplos sinais reduz o risco de falsos rompimentos

- A análise de força relativa filtra eficazmente ativos fortes

- Mecanismo de ajuste adaptativo do período de tempo

- Sistema de controle de risco abrangente

- Inclui mecanismo inteligente de reentrada

- Visualização do status da negociação em tempo real

Riscos da Estratégia

- Mercados laterais podem gerar negociações frequentes

- A dependência de múltiplos indicadores pode causar atraso nos sinais

- Limiares fixos de RSI podem não se adaptar a todos os ambientes de mercado

- O cálculo da força relativa depende da precisão do índice de referência

- O stop loss baseado nas máximas de 52 semanas pode ser muito amplo

Direções de Otimização da Estratégia

- Introduzir limiares adaptativos de RSI

- Otimizar a lógica de julgamento das condições de reentrada

- Adicionar dimensão de análise de volume de negociação

- Aprimorar os mecanismos de stop loss e take profit

- Incluir filtro de volatilidade

- Otimizar o período de cálculo da força relativa

Conclusão

A estratégia constrói um sistema de negociação abrangente ao combinar análise técnica e análise de força relativa. Seu mecanismo de confirmação de múltiplos sinais e sistema de controle de risco a tornam bastante prática. Com as direções de otimização sugeridas, há ainda espaço para aprimoramento. A implementação bem-sucedida da estratégia exige que o trader tenha um conhecimento profundo do mercado e faça ajustes adequados de parâmetros de acordo com as características específicas do ativo negociado.

- 1