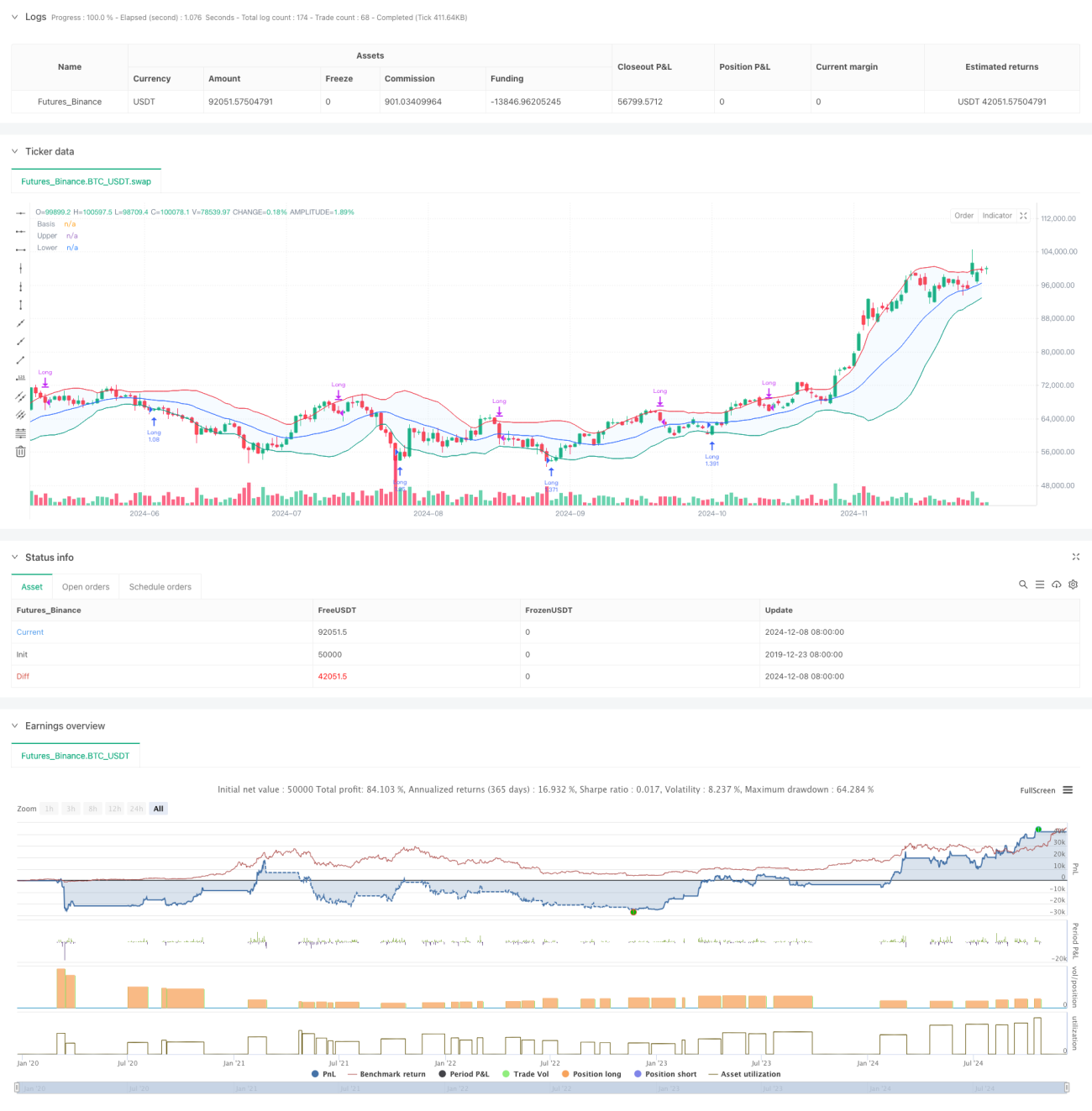

Visão Geral

Esta estratégia é um sistema de negociação inteligente baseado em Bandas de Bollinger e no indicador ATR, combinando mecanismos multiníveis de take profit e stop loss. A estratégia identifica principalmente sinais de reversão próximos à banda inferior de Bollinger para entradas longas e utiliza um método de trailing stop dinâmico para gerenciar o risco. O sistema define uma meta de lucro de 20% e um stop loss de 12%, além de utilizar o ATR para implementar um trailing stop dinâmico, protegendo os lucros e dando espaço suficiente para o desenvolvimento da tendência.

Princípio da Estratégia

A lógica central da estratégia inclui as seguintes partes principais:

- Condição de entrada: exige que, após um candle vermelho tocar a banda inferior de Bollinger, apareça um candle verde. Esse padrão geralmente indica um possível sinal de reversão.

- Seleção de Média Móvel: suporta vários tipos de médias móveis (SMA, EMA, SMMA, WMA, VWMA), com SMA de 20 períodos como padrão.

- Parâmetros das Bandas de Bollinger: utiliza 1,5 vezes o desvio padrão como largura da banda, uma configuração mais conservadora que o tradicional 2 desvios padrão.

- Mecanismo de Take Profit: define uma meta de lucro inicial de 20%.

- Mecanismo de Stop Loss: estabelece um stop loss fixo de 12% para proteger o capital.

- Trailing Stop Dinâmico:

- Ativa o trailing stop baseado em ATR após o preço atingir o nível de lucro alvo.

- Inicia o trailing stop dinâmico com ATR ao tocar a banda superior de Bollinger.

- Utiliza um multiplicador do ATR para ajustar dinamicamente a distância do trailing stop.

Vantagens da Estratégia

- Controle de Risco Multinível:

- Stop loss fixo para proteger o capital.

- Trailing stop dinâmico para travar lucros.

- Stop loss dinâmico acionado pela banda superior de Bollinger oferece proteção adicional.

- A escolha flexível de médias móveis permite que a estratégia se adapte a diferentes condições de mercado.

- O trailing stop dinâmico combinado com o ATR ajusta-se automaticamente à volatilidade do mercado, evitando saídas prematuras.

- O sinal de entrada combina formações de preço e indicadores técnicos, aumentando a confiabilidade do sinal.

- Suporte para gerenciamento de posição e custos de negociação, aproximando-se de um ambiente de negociação real.

Riscos da Estratégia

- Mercados com rápidas oscilações podem gerar negociações frequentes, aumentando os custos de transação.

- O stop loss fixo de 12% pode ser muito apertado em mercados de alta volatilidade.

- Sinais das Bandas de Bollinger podem gerar falsos sinais em mercados com tendência.

- O trailing stop baseado em ATR pode levar a grandes drawdowns durante movimentos bruscos.

Medidas de mitigação:

- Recomenda-se o uso em prazos maiores (30 minutos a 1 hora).

- Ajustar a porcentagem de stop loss conforme as características específicas do ativo.

- Considerar a adição de um filtro de tendência para reduzir sinais falsos.

- Ajustar dinamicamente o multiplicador do ATR para se adaptar a diferentes condições de mercado.

Direções de Otimização da Estratégia

-

Otimização de Entrada:

- Adicionar mecanismo de confirmação por volume.

- Incluir filtro baseado em indicador de força de tendência.

- Considerar a incorporação de indicadores de momentum para auxiliar na decisão.

-

Otimização de Stop Loss:

- Substituir o stop loss fixo por um stop loss dinâmico baseado em ATR.

- Desenvolver algoritmo de stop loss adaptativo.

- Ajustar a distância do stop loss dinamicamente de acordo com a volatilidade.

-

Otimização de Médias Móveis:

- Testar diferentes combinações de períodos.

- Estudar métodos de período adaptativo.

- Considerar o uso de price action em substituição às médias móveis.

-

Otimização de Gerenciamento de Posição:

- Desenvolver sistema de gerenciamento de posição baseado em volatilidade.

- Implementar mecanismos de entrada e saída parcial.

- Adicionar controle de exposição ao risco.

Resumo

Esta estratégia constrói um sistema de negociação multinível através das Bandas de Bollinger e do ATR, adotando métodos de gerenciamento dinâmico na entrada, stop loss e take profit. Sua vantagem reside no sistema robusto de controle de risco e na capacidade de adaptação à volatilidade do mercado. Com as direções de otimização sugeridas, a estratégia possui grande potencial de melhoria. É particularmente adequada para uso em prazos maiores e, para investidores que detêm ativos de qualidade, pode ajudar a otimizar os momentos de entrada e saída de posições.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Demo GPT - Bollinger Bands Strategy with Tightened Trailing Stops", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_value=0.1, slippage=3)

// Input settings- 1