Sistema de Seguimento de Tendência e Negociação de Swing com EMA/SMA, combinado com Filtro de Volume e Stop Loss/Take Profit Percentuais

Visão Geral

Esta estratégia é um sistema de negociação abrangente que combina métodos de acompanhamento de tendência e swing trading, construindo um sistema completo de negociação através de cruzamentos de médias móveis EMA e SMA, identificação de pontos altos e baixos de onda, filtro de volume e mecanismos de take profit percentual e stop loss móvel. O design da estratégia prioriza a confirmação multidimensional de sinais, aumentando a precisão e confiabilidade das negociações por meio da sinergia de indicadores técnicos.

Princípios da Estratégia

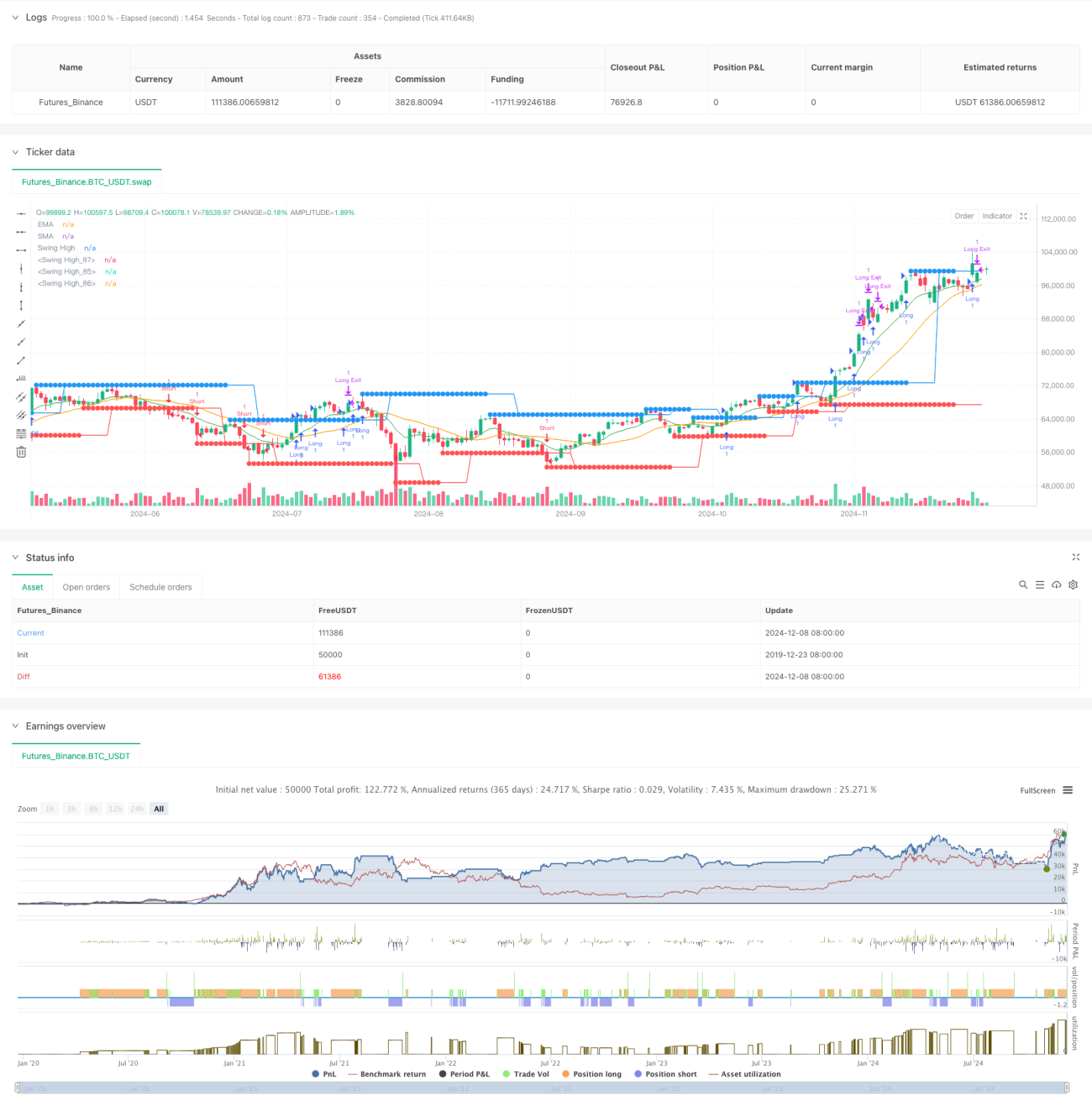

A estratégia emprega um mecanismo de filtragem de sinais em múltiplas camadas. Primeiro, utiliza o cruzamento das médias móveis EMA(10) e SMA(21) para formar um julgamento básico de tendência. Em seguida, determina o momento de entrada através da quebra de pontos altos e baixos das seis barras anteriores e posteriores, simultaneamente exigindo que o volume seja superior à média móvel de 200 períodos, garantindo negociação em ambiente de liquidez suficiente. O sistema utiliza take profit de 2% e stop loss móvel de 1% para gerenciar riscos. Quando o preço ultrapassa o ponto alto da onda e atende às condições de volume, o sistema abre uma posição comprada; quando o preço cai abaixo do ponto baixo da onda e atende às condições de volume, o sistema abre uma posição vendida.

Vantagens da Estratégia

- Mecanismo de confirmação de múltiplos sinais reduz sinais falsos: através da tríplice verificação da tendência das médias, quebra de preço e aumento de volume, aumenta a confiabilidade das negociações.

- Mecanismo flexível de take profit e stop loss: define take profit com base percentual e utiliza stop loss móvel para travar lucros.

- Sistema visual completo: fornece exibição gráfica de médias móveis e pontos de ruptura, facilitando o monitoramento das negociações.

- Alta customização: parâmetros-chave são ajustáveis para se adaptar a diferentes condições de mercado.

- Gestão de risco sistematizada: controla o risco por meio de stop loss e take profit predefinidos.

Riscos da Estratégia

- Em mercados laterais, pode gerar falsas rupturas frequentes.

- O filtro de volume pode fazer com que alguns sinais válidos sejam perdidos.

- Take profit percentual fixo pode causar saída precoce em movimentos fortes.

- O sistema de médias móveis apresenta atraso em mercados com rápidas reversões de tendência.

- É necessário considerar o impacto dos custos de negociação no retorno da estratégia.

Direções de Otimização da Estratégia

- Introduzir mecanismo adaptativo de volatilidade para ajustar dinamicamente os parâmetros de take profit e stop loss.

- Adicionar filtro de força da tendência para evitar negociações em tendências fracas.

- Otimizar o algoritmo de filtro de volume, considerando a variação relativa do volume.

- Adicionar mecanismo de filtragem temporal para evitar negociações em períodos desfavoráveis.

- Considerar a inclusão de classificação do ambiente de mercado, adotando parâmetros diferentes conforme o tipo de mercado.

Resumo

Esta estratégia constrói um sistema de negociação completo através do sistema de médias móveis, quebra de preço e verificação de volume, sendo adequada para acompanhamento de tendências de médio a longo prazo. O ponto forte do sistema reside na confirmação de múltiplos sinais e no mecanismo completo de gerenciamento de risco, mas é importante prestar atenção ao seu desempenho em mercados laterais. Com as direções de otimização sugeridas, a estratégia ainda possui espaço para melhorias, especialmente no que diz respeito à adaptabilidade, o que contribuirá para aumentar a estabilidade da estratégia.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// Strategy combining EMA/SMA Crossover, Swing High/Low, Volume Filtering, and Percentage TP & Trailing Stop

strategy("Swing High/Low Strategy with Volume, EMA/SMA Crossovers, Percentage TP and Trailing Stop", overlay=true)

- 1