Este sistema é um sistema de negociação quantitativo baseado em um oscilador dinâmico RSI. Através do ajuste polinomial e da análise de séries temporais do indicador RSI, calcula a taxa de variação do RSI para capturar o momentum do mercado. A estratégia utiliza métodos matemáticos avançados, como a decomposição QR, para processamento de sinais e combina um sistema de médias móveis para tomar decisões de negociação.

Princípio da Estratégia

O núcleo da estratégia é o oscilador Delta-RSI, que é implementado através das seguintes etapas:

- Primeiro, calcula o RSI tradicional como dado base.

- Utiliza ajuste polinomial para suavizar o RSI, reduzindo o ruído.

- Calcula a derivada temporal do RSI para obter o Delta-RSI, refletindo a taxa de variação do RSI.

- Compara o Delta-RSI com sua média móvel para gerar sinais de negociação.

- Utiliza o erro quadrático médio (RMSE) para avaliar e filtrar a qualidade do ajuste.

Os sinais de negociação podem ser gerados de três formas:

- Cruzamento da linha zero: Quando o Delta-RSI passa de negativo para positivo, indica compra; quando passa de positivo para negativo, indica venda.

- Cruzamento da linha de sinal: Quando o Delta-RSI cruza para cima/para baixo de sua média móvel, indica compra/venda, respectivamente.

- Mudança de direção: Quando o Delta-RSI começa a subir em território negativo, indica compra; quando começa a cair em território positivo, indica venda.

Vantagens da Estratégia

- Base matemática sólida: Utiliza métodos matemáticos avançados, como a decomposição QR, para processamento de sinais, com fundamentação teórica confiável.

- Suavização de sinais: O ajuste polinomial pode filtrar efetivamente o ruído do mercado, melhorando a qualidade dos sinais.

- Alta flexibilidade: Oferece diversas formas de geração de sinais e opções de parâmetros, adaptando-se a diferentes ambientes de mercado.

- Risco controlável: Inclui mecanismo de filtragem por RMSE, permitindo selecionar sinais com maior confiabilidade.

- Eficiência computacional: Utiliza algoritmos otimizados para operações matriciais, resultando em alta eficiência de execução.

Riscos da Estratégia

- Sensibilidade a parâmetros: Vários parâmetros-chave precisam ser ajustados cuidadosamente; a escolha inadequada de parâmetros pode afetar gravemente o desempenho da estratégia.

- Atraso: O processamento de suavização de sinais pode introduzir algum atraso, podendo perder movimentos rápidos do mercado.

- Falsos rompimentos: Em mercados laterais, podem ser gerados sinais falsos, aumentando os custos de negociação.

- Complexidade computacional: Envolve muitas operações matriciais, podendo haver gargalos de desempenho em negociações de alta frequência.

- Sobreajuste: Ao otimizar parâmetros, é necessário evitar o sobreajuste aos dados históricos.

Direções de Otimização da Estratégia

- Parâmetros adaptativos: Ajustar dinamicamente o período do RSI e a ordem do ajuste com base na volatilidade do mercado.

- Múltiplos períodos de tempo: Combinar sinais de mais períodos de tempo para validação cruzada.

- Filtragem por volatilidade: Adicionar indicadores de volatilidade, como o ATR, para filtrar sinais.

- Classificação de mercado: Utilizar regras diferentes de geração de sinais para diferentes estados do mercado (tendência/lateral).

- Otimização de stop loss: Incorporar mecanismos de stop loss mais inteligentes, como stop loss dinâmico baseado em níveis de suporte e resistência.

Resumo

Esta é uma estratégia de negociação quantitativa com estrutura completa e base teórica sólida. Através da análise das características dinâmicas do RSI, combinada com métodos matemáticos modernos para processamento de sinais, consegue capturar bem as tendências do mercado. Embora apresente certa sensibilidade a parâmetros e complexidade computacional, com a escolha adequada de parâmetros e melhorias na otimização, a estratégia tem bom valor de aplicação. Recomenda-se atenção ao controle de risco, dimensionamento adequado das posições e monitoramento contínuo do desempenho da estratégia em aplicações reais.

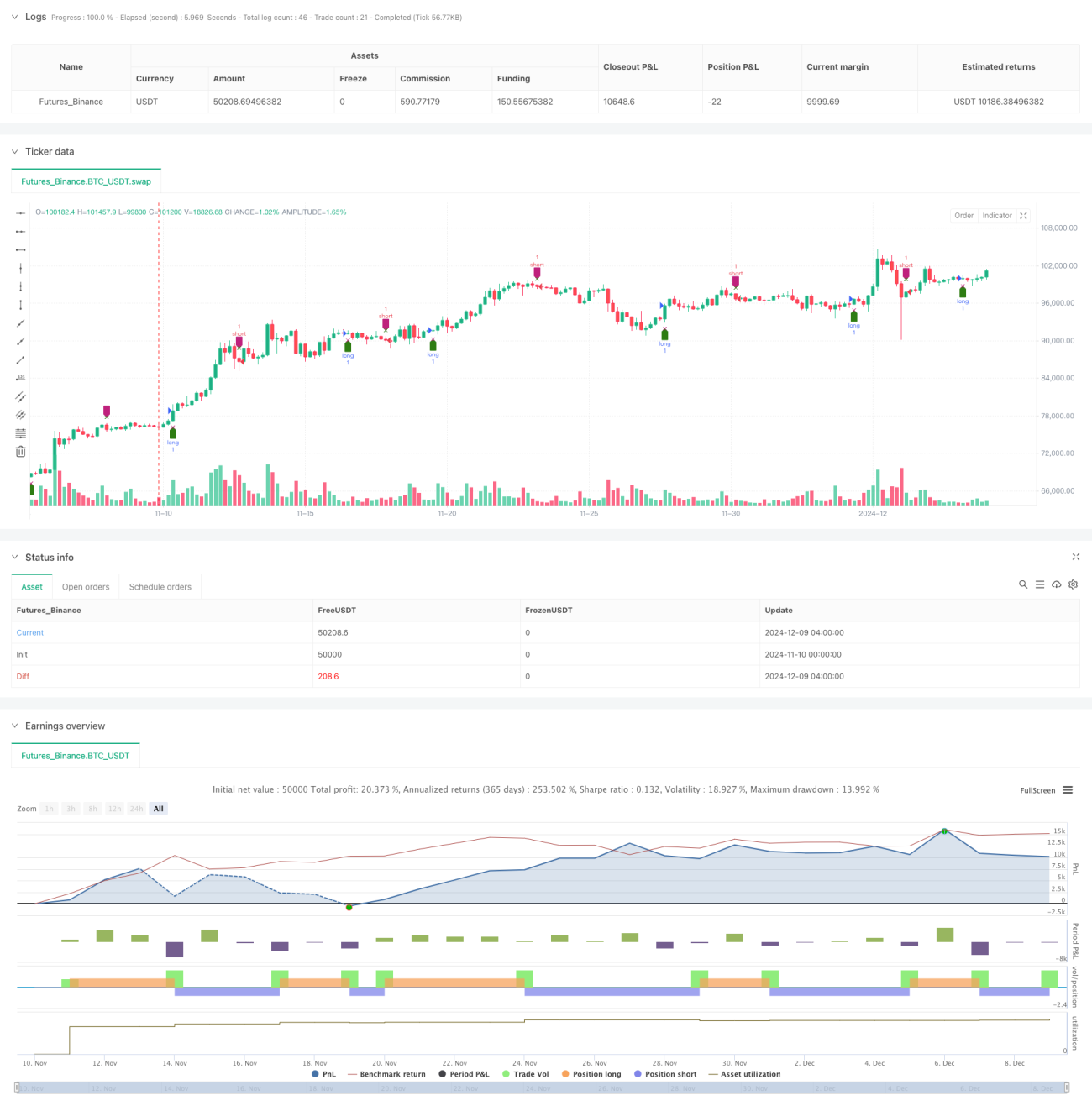

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tbiktag

//

// Delta-RSI Oscillator Strategy- 1