Visão Geral

Esta estratégia é um sistema de trading inteligente que combina MACD (Convergência/Divergência de Médias Móveis) e a inclinação da regressão linear (LRS). A estratégia otimiza o cálculo do indicador MACD através da combinação de vários métodos de média móvel e introduz a análise de regressão linear para aumentar a confiabilidade dos sinais de trading. Permite que o trader escolha flexivelmente usar um único indicador ou uma combinação de dois indicadores para gerar sinais de trading, e inclui mecanismos de stop-loss e take-profit para gerenciar riscos.

Princípio da Estratégia

O núcleo da estratégia é capturar tendências de mercado por meio do MACD otimizado e do indicador de regressão linear. A parte do MACD utiliza uma combinação de quatro métodos de média móvel: SMA, EMA, WMA e TEMA, aumentando a sensibilidade às tendências de preço. A parte de regressão linear determina a direção e a força da tendência calculando a inclinação e a posição da linha de regressão. Os sinais de compra podem ser baseados no cruzamento de ouro do MACD, na tendência de alta da regressão linear ou na confirmação de ambos. Da mesma forma, os sinais de venda também podem ser configurados de forma flexível. A estratégia inclui ainda configurações de stop-loss e take-profit baseadas em porcentagem, gerenciando efetivamente a relação risco-retorno de cada operação.

Vantagens da Estratégia

- Flexibilidade na combinação de indicadores: Possibilidade de escolher usar um único indicador ou uma combinação de dois, conforme as condições do mercado.

- Cálculo MACD aprimorado: Maior precisão na identificação de tendências através do uso de múltiplos métodos de média móvel.

- Confirmação objetiva de tendências: Uso da regressão linear para fornecer uma avaliação de tendência com suporte estatístico matemático.

- Gestão de risco completa: Integração de mecanismos de stop-loss e take-profit.

- Alta ajustabilidade de parâmetros: Parâmetros-chave podem ser otimizados de acordo com diferentes características de mercado.

Riscos da Estratégia

- Sensibilidade a parâmetros: Diferentes condições de mercado podem exigir ajustes frequentes nos parâmetros.

- Atraso nos sinais: Indicadores baseados em médias móveis possuem alguma defasagem.

- Não adequada para mercados laterais: Em mercados de congestão (sideways), pode gerar sinais falsos.

- Custo de oportunidade da dupla confirmação: A confirmação rigorosa com dois indicadores pode fazer com que se percam boas oportunidades de trading.

Direções de Otimização da Estratégia

- Adicionar identificação do ambiente de mercado: Introduzir indicadores de volatilidade para distinguir entre mercados de tendência e laterais.

- Ajuste dinâmico de parâmetros: Ajustar automaticamente os parâmetros do MACD e da regressão linear de acordo com o estado do mercado.

- Otimizar stop-loss e take-profit: Introduzir stop-loss e take-profit dinâmicos, ajustando automaticamente conforme a volatilidade do mercado.

- Adicionar análise de volume: Combinar indicadores de volume para aumentar a confiabilidade dos sinais.

- Introduzir análise de períodos temporais: Considerar a confirmação em múltiplos períodos de tempo para melhorar a precisão das operações.

Resumo

Esta estratégia cria um sistema de trading que alia flexibilidade e confiabilidade ao combinar versões aprimoradas de indicadores clássicos com métodos estatísticos. Seu design modular permite que o trader ajuste de forma flexível os parâmetros da estratégia e os mecanismos de confirmação de sinais de acordo com diferentes condições de mercado. Com otimização e melhorias contínuas, esta estratégia tem potencial para manter um desempenho estável em diversos ambientes de mercado.

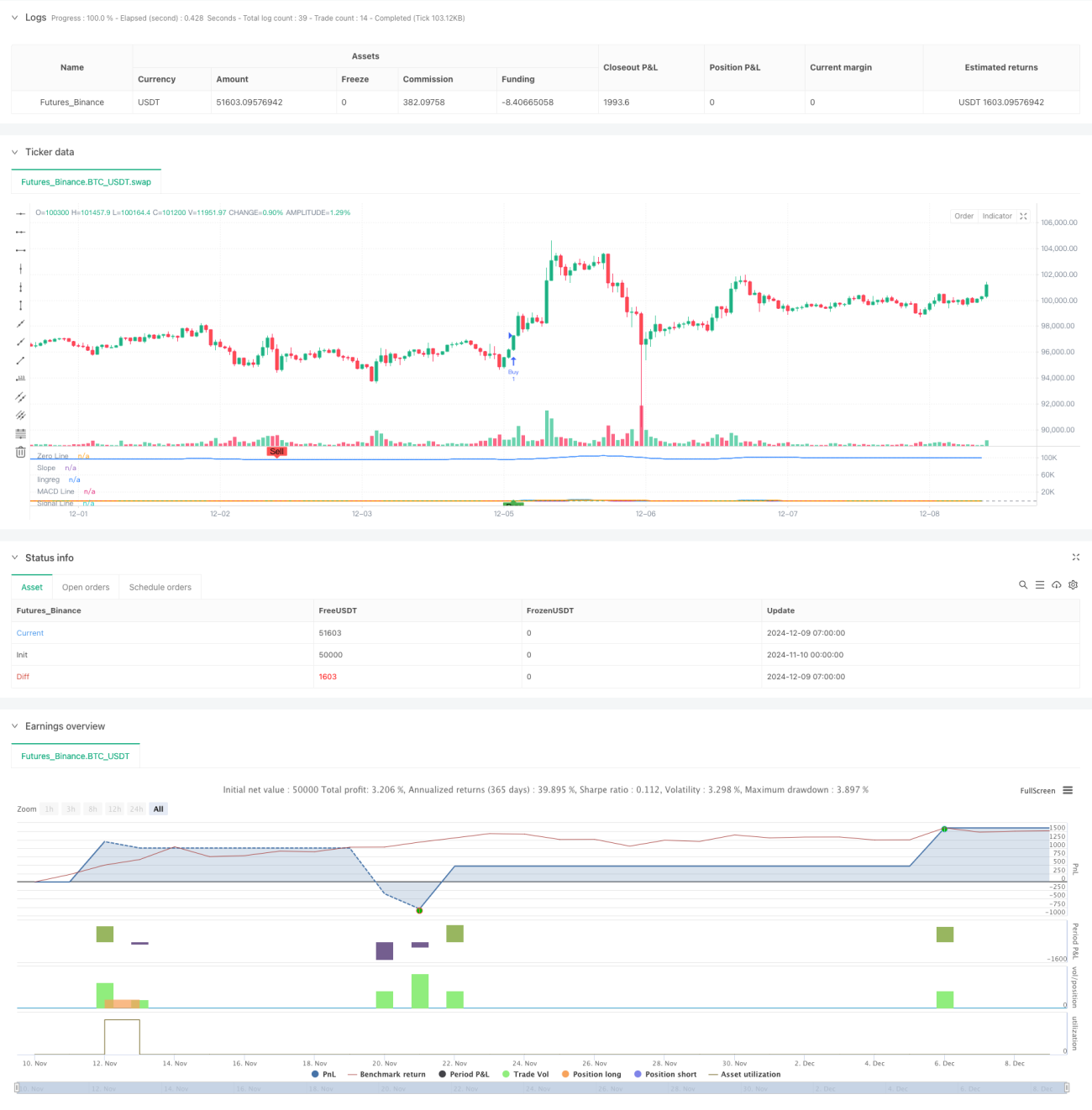

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('SIMPLIFIED MACD & LRS Backtest by NHBProd', overlay=false)

// Function to calculate TEMA (Triple Exponential Moving Average)- 1