Visão Geral

Esta estratégia é um sistema de negociação quantitativo que combina o Indicador de Aceleração (AC) e o Estocástico (Stochastic). Ela captura as mudanças no momentum do mercado identificando divergências entre o preço e os indicadores técnicos, prevendo assim potenciais reversões de tendência. A estratégia também integra a Média Móvel Simples (SMA) e o Índice de Força Relativa (RSI) para aumentar a confiabilidade dos sinais, e define stop-loss e take-profit fixos para controlar o risco.

Princípio da Estratégia

A lógica central da estratégia baseia-se na cooperação de múltiplos indicadores técnicos. Primeiro, calcula-se o Indicador de Aceleração (AC), que é obtido pela diferença entre as médias móveis de 5 e 34 períodos do preço mediano, subtraindo-se sua média móvel de N períodos. Simultaneamente, calculam-se os valores K e D do Estocástico para confirmar os sinais de divergência. Quando o preço atinge uma nova mínima e o AC sobe, forma-se uma divergência de alta; quando o preço atinge uma nova máxima e o AC cai, forma-se uma divergência de baixa. A estratégia também introduz o RSI como indicador de confirmação auxiliar, aumentando a precisão dos sinais por meio da validação cruzada de múltiplos indicadores.

Vantagens da Estratégia

- Cooperação de múltiplos indicadores: A combinação dos indicadores AC, Estocástico e RSI pode filtrar eficazmente sinais falsos.

- Gerenciamento de risco automatizado: Configurações fixas de stop-loss e take-profit integradas podem controlar efetivamente o risco de cada negociação.

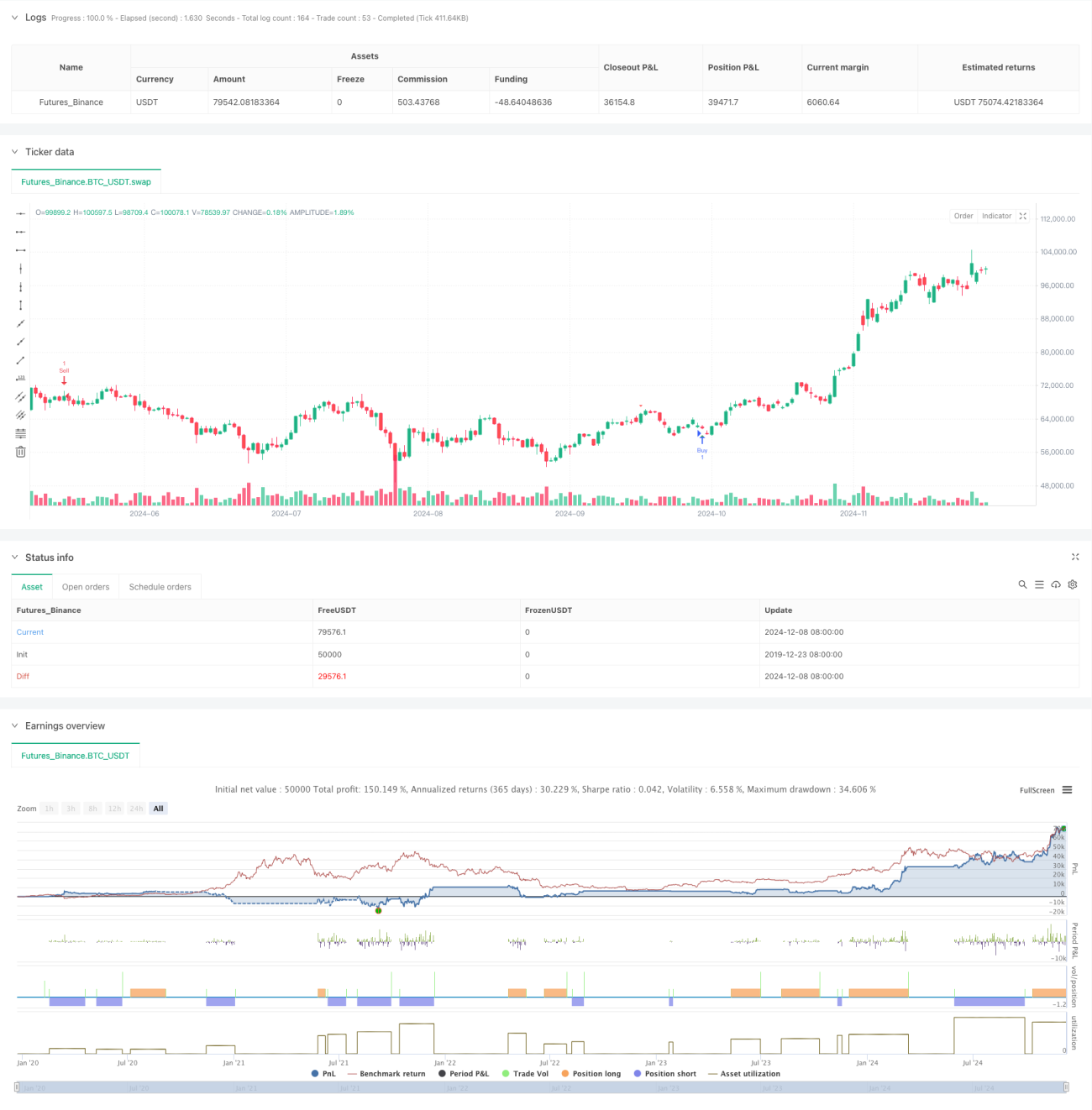

- Dicas visuais: Sinais de compra e venda são claramente marcados no gráfico, facilitando a identificação rápida de oportunidades pelo trader.

- Alta flexibilidade: Parâmetros altamente ajustáveis, adequados para diferentes ambientes de mercado e períodos de negociação.

- Alertas em tempo real: Sistema de alerta em tempo real integrado para garantir que nenhuma oportunidade de negociação seja perdida.

Riscos da Estratégia

- Risco de falso rompimento: Em mercados laterais, podem ocorrer sinais falsos de divergência.

- Risco de slippage: Como são usados stop-loss e take-profit fixos, pode haver slippage significativo durante alta volatilidade do mercado.

- Sensibilidade a parâmetros: Diferentes combinações de parâmetros podem levar a grandes variações no desempenho da estratégia.

- Dependência do ambiente de mercado: Em mercados sem tendência clara, a estratégia pode não ter um bom desempenho.

- Atraso nos sinais: Devido ao uso de médias móveis, os sinais podem apresentar algum atraso.

Direções de Otimização da Estratégia

- Stop-loss e take-profit dinâmicos: Ajustar dinamicamente os níveis de stop-loss e take-profit com base na volatilidade do mercado.

- Introduzir indicadores de volume: Aumentar a confiabilidade dos sinais por meio da confirmação de volume.

- Filtro de ambiente de mercado: Adicionar um módulo de identificação de tendência para adotar diferentes estratégias de negociação em diferentes ambientes de mercado.

- Otimização de parâmetros: Usar métodos de aprendizado de máquina para otimizar as combinações de parâmetros dos indicadores.

- Adicionar filtro de tempo: Considerar as características do horário do mercado para evitar negociações em períodos desfavoráveis.

Resumo

Esta é uma estratégia de negociação quantitativa que integra múltiplos indicadores técnicos, capturando pontos de virada do mercado por meio de sinais de divergência. Sua vantagem reside na validação cruzada de múltiplos indicadores e no sistema completo de controle de risco, mas é preciso estar atento a problemas como falsos rompimentos e otimização de parâmetros. Com otimização e melhorias contínuas, espera-se que esta estratégia mantenha um desempenho estável em diferentes ambientes de mercado.

- 1