Visão Geral

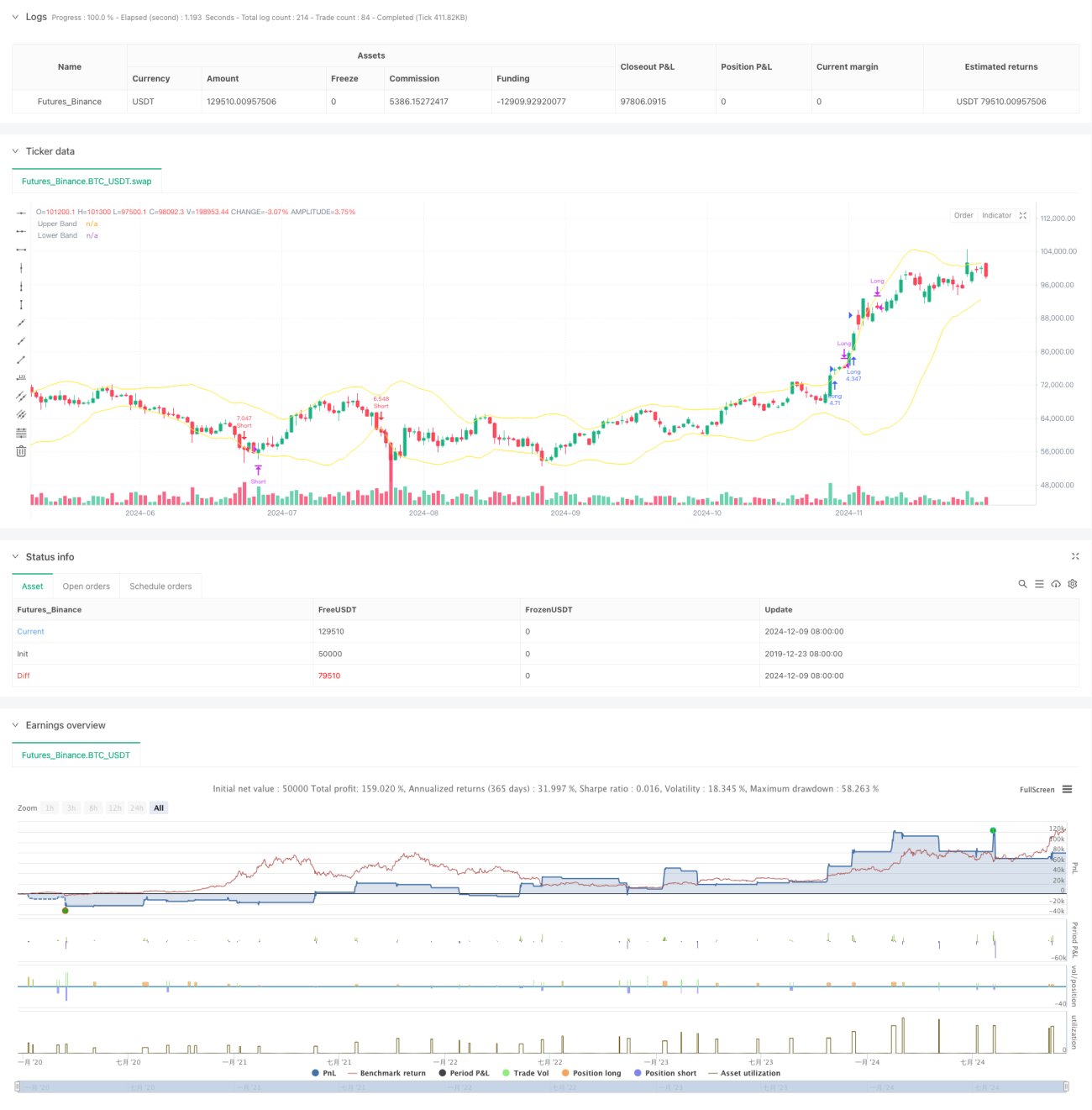

Esta estratégia é um sistema de negociação quantitativo de 4 horas baseado no indicador Bollinger Bands, combinando conceitos de breakout de tendência e reversão à média. A estratégia captura o momentum do mercado através de breakouts das bandas superior e inferior do Bollinger, realiza lucros quando o preço retorna à média e controla riscos com stops. Utiliza alavancagem de 3x, ponderando retorno e risco de forma equilibrada.

Princípio da Estratégia

A lógica central da estratégia baseia-se nos seguintes elementos-chave:

- Utiliza uma média móvel de 20 períodos como banda central do Bollinger, com desvio padrão de 2 vezes como intervalo de volatilidade.

- Sinal de entrada: quando o corpo real do candle (média entre abertura e fechamento) rompe a banda superior, abre-se compra; quando rompe a banda inferior, abre-se venda.

- Sinal de saída: em posição comprada, se dois candles consecutivos tiverem fechamento e abertura abaixo da banda superior e fechamento abaixo da abertura, fecha-se a posição; para posição vendida, lógica oposta.

- Controle de risco: no momento da entrada, o stop é definido no ponto mais alto/mais baixo do candle atual, garantindo perda controlada por operação.

Vantagens da Estratégia

- Lógica de negociação clara: combina ideias de tendência e reversão, com bom desempenho em diferentes condições de mercado.

- Controle de risco robusto: stop dinâmico baseado na volatilidade dos candles limita o drawdown.

- Filtragem de sinais falsos: confirma o rompimento pela posição do corpo do candle, não apenas pelo fechamento, reduzindo perdas com falsos breakouts.

- Gerenciamento de capital adequado: ajusta o tamanho da posição dinamicamente com base no patrimônio da conta, equilibrando retorno e risco.

Riscos da Estratégia

- Risco de mercado lateral: em mercados consolidados, pode gerar sinais falsos frequentes, levando a stops consecutivos.

- Risco de alavancagem: o uso de 3x pode causar perdas significativas em movimentos bruscos.

- Risco de stop: definir o stop no ponto mais alto/mais baixo do candle pode ser muito amplo, aumentando a perda por operação.

- Dependência do timeframe: o gráfico de 4 horas pode reagir lentamente em alguns cenários, perdendo o movimento.

Direções de Otimização

- Adicionar filtro de tendência: usar indicadores de timeframe maior para negociar na direção da tendência principal.

- Otimizar o stop: considerar ATR ou largura das Bandas de Bollinger para ajustar dinamicamente a distância do stop.

- Gerenciamento de posição: ajustar a alavancagem conforme a volatilidade ou força da tendência.

- Avaliação do ambiente: incluir indicadores de volume ou volatilidade para identificar o estado do mercado e decidir a entrada.

Resumo

Esta estratégia combina o seguimento de tendência e a reversão à média das Bandas de Bollinger, utilizando condições rigorosas de entrada/saída e controle de risco para alcançar retornos estáveis tanto em tendências quanto em mercados laterais. Sua principal vantagem é a lógica clara e o sistema robusto de gestão de risco, mas ainda precisa de otimizações no uso de alavancagem e na avaliação do ambiente de mercado para melhorar a estabilidade e o potencial de lucro.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Bollinger 4H Follow", overlay=true, initial_capital=300, commission_type=strategy.commission.percent, commission_value=0.04)

// StartYear = input(2022,"Backtest Start Year")

// StartMonth = input(1,"Backtest Start Month") - 1