Estratégia de Seguimento de Tendência e Reversão de Preços com Múltiplos Equilíbrios

Visão Geral da Estratégia

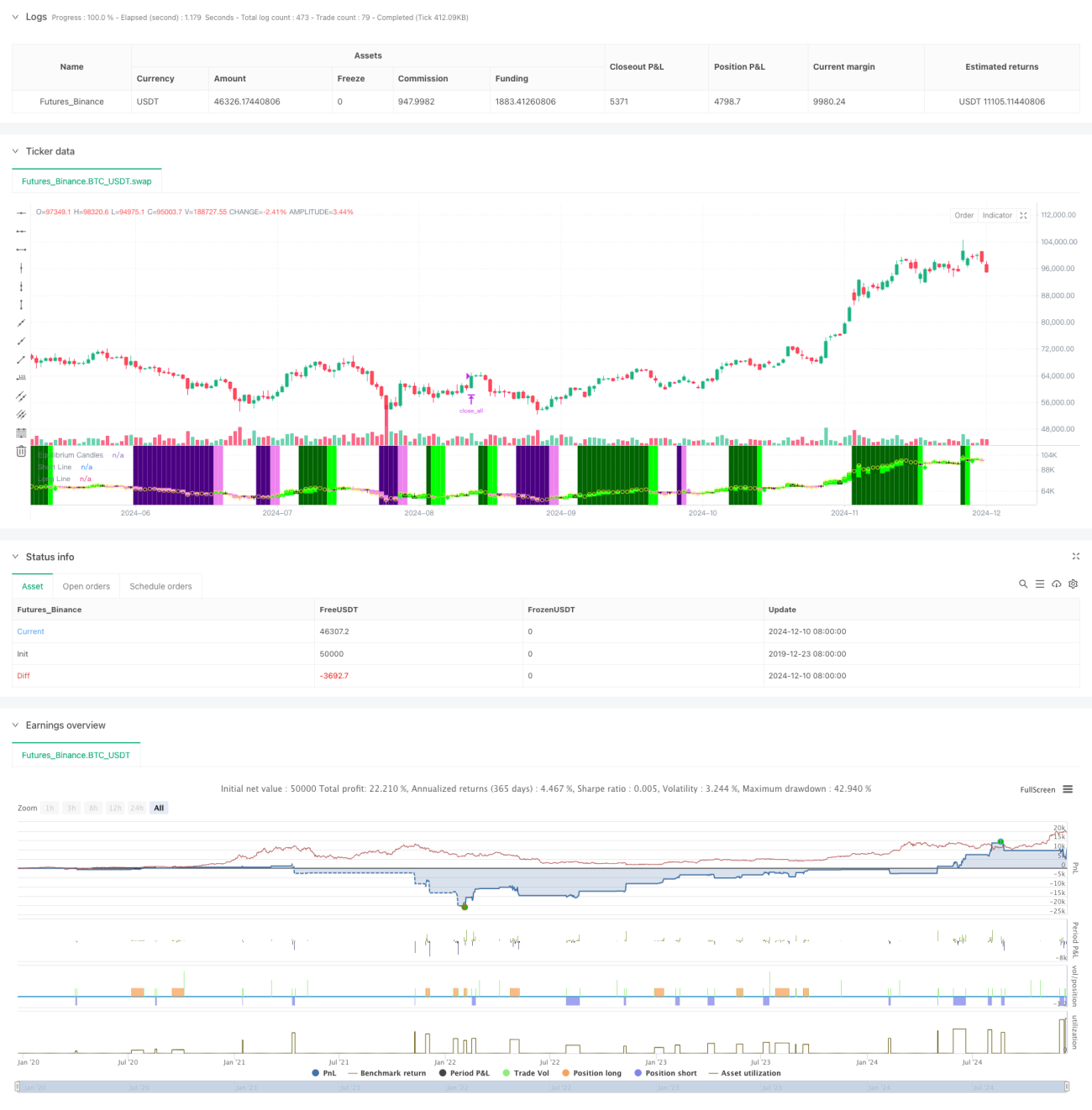

Esta estratégia é um sistema de negociação baseado em pontos de equilíbrio de preços, combinando tendência e reversão. Ela calcula o preço de equilíbrio por meio do valor médio entre o ponto mais alto e o ponto mais baixo das últimas X barras, e determina a direção da tendência com base na posição do preço de fechamento em relação a esse preço de equilíbrio. Quando o preço se mantém consistentemente em um lado do preço de equilíbrio por um número definido de barras, o sistema confirma a tendência. Na primeira correção (quando o preço rompe o preço de equilíbrio), o sistema busca oportunidades de entrada. A estratégia pode ser configurada para operar no modo de acompanhamento de tendência ou reversão.

Princípio da Estratégia

- Cálculo do Preço de Equilíbrio: Utiliza o ponto médio entre a máxima e a mínima das últimas X barras como preço de equilíbrio, método semelhante ao cálculo da linha base do Ichimoku Kinko Hyo.

- Identificação de Tendência: Quando o preço permanece continuamente no mesmo lado do preço de equilíbrio por X barras (padrão 7), a tendência é confirmada.

- Sinal de Entrada: O sinal de entrada é acionado na primeira correção após a confirmação da tendência (quando o preço rompe o preço de equilíbrio).

- Stop Loss e Take Profit: Utiliza o percentil 60 do ATR para ajustar dinamicamente as distâncias de stop loss e take profit, oferecendo flexibilidade no controle de risco.

- Proteção contra Grandes Oscilações: Quando o preço se desvia do ponto de equilíbrio além de um múltiplo do ATR definido, o sistema fecha automaticamente a posição para evitar drawdowns significativos.

Vantagens da Estratégia

- Alta Adaptabilidade: Permite alternar flexivelmente entre modos de acompanhamento de tendência e reversão, de acordo com as características do mercado.

- Controle de Risco Robusto: Utiliza stop loss dinâmico baseado no ATR e possui mecanismo de proteção contra grandes oscilações.

- Operação Clara: Os sinais de negociação são nítidos, sem depender de combinações complexas de indicadores técnicos.

- Boa Visualização: Usa velas coloridas e fundo para fornecer uma exibição intuitiva do estado do mercado.

- Amigável para Automação: Pode ser facilmente integrado a plataformas de negociação como MT5 para automação.

Riscos da Estratégia

- Risco de Mercado Lateral: Em mercados laterais, pode gerar sinais falsos frequentes.

- Impacto de Slippage: Pode enfrentar deslizamento significativo durante movimentos voláteis.

- Sensibilidade a Parâmetros: Parâmetros-chave, como período de equilíbrio e ciclo de confirmação de tendência, exigem otimização cuidadosa para diferentes mercados.

- Risco de Transição de Mercado: Períodos de transição de tendência para lateralização podem causar grandes drawdowns.

Direções de Otimização da Estratégia

- Identificação do Ambiente de Mercado: Adicionar módulo de avaliação do ambiente de mercado para ajustar dinamicamente os parâmetros da estratégia em diferentes condições.

- Filtragem de Sinais: Considerar a inclusão de indicadores auxiliares, como volume e volatilidade, para filtrar sinais falsos.

- Gerenciamento de Posição: Introduzir mecanismos mais complexos de gerenciamento de posição, como ajuste dinâmico baseado na volatilidade.

- Múltiplos Timeframes: Integrar sinais de múltiplos períodos para aumentar a precisão das negociações.

- Otimização de Custos de Transação: Ajustar os momentos de entrada e saída considerando as características de custo de cada instrumento negociado.

Conclusão

Este é um sistema de negociação de tendências bem projetado, que oferece uma lógica de negociação clara através do conceito central de preço de equilíbrio. A principal característica da estratégia é sua alta flexibilidade, podendo ser usada tanto para acompanhamento de tendência quanto para reversão, além de possuir mecanismos robustos de controle de risco. Embora possa enfrentar desafios em certas condições de mercado, com otimização contínua e ajustes flexíveis, a estratégia tem potencial para manter desempenho estável em diversos ambientes de mercado.

- 1