Estratégia Avançada de Seguimento de Tendência com Stop Loss Adaptativo e Rastreamento

Visão Geral

Esta é uma estratégia de acompanhamento de tendência baseada no indicador Supertrend, combinada com um mecanismo adaptativo de stop loss móvel. A estratégia identifica principalmente a direção da tendência do mercado através do indicador Supertrend e utiliza um stop loss móvel ajustado dinamicamente para gerenciar riscos e otimizar o momento de saída. A estratégia suporta vários métodos de stop loss, incluindo stop loss percentual, stop loss ATR e stop loss por pontos fixos, permitindo ajustes flexíveis de acordo com diferentes condições de mercado.

Princípio da Estratégia

A lógica central da estratégia é baseada nos seguintes elementos-chave:

- O indicador Supertrend é usado como principal referência para julgar a tendência, combinando o ATR (Average True Range) para medir a volatilidade do mercado.

- Os sinais de entrada são acionados pela mudança de direção do Supertrend, suportando operações de compra, venda ou ambos os lados.

- O mecanismo de stop loss adota um stop loss móvel adaptativo, que pode ajustar automaticamente a posição do stop loss conforme a volatilidade do mercado.

- O sistema de gerenciamento de operações inclui gestão de posição (por padrão, 15% da conta) e um mecanismo de filtro de tempo.

Vantagens da Estratégia

- Forte capacidade de captura de tendência: O indicador Supertrend identifica eficazmente as principais tendências, reduzindo falsos sinais.

- Controle de risco completo: Utiliza diversos mecanismos de stop loss, adaptando-se a diferentes ambientes de mercado.

- Alta flexibilidade: Suporta a configuração de várias direções de negociação e métodos de stop loss.

- Forte adaptabilidade: O stop loss móvel se ajusta automaticamente à volatilidade do mercado, melhorando a capacidade de adaptação da estratégia.

- Sistema de backtesting completo: Inclui função de filtro de tempo, facilitando a análise de desempenho histórico.

Riscos da Estratégia

- Risco de reversão de tendência: Em mercados voláteis, podem ocorrer sinais falsos.

- Risco de slippage: A execução do stop loss móvel pode ser afetada pela liquidez do mercado.

- Sensibilidade a parâmetros: Os fatores do Supertrend e a configuração do período ATR têm grande impacto no desempenho da estratégia.

- Dependência do ambiente de mercado: Em mercados laterais, pode haver negociações frequentes, aumentando os custos.

Direções de Otimização da Estratégia

- Otimização do filtro de sinais: Podem ser adicionados indicadores técnicos extras para filtrar sinais falsos.

- Otimização do gerenciamento de posição: A proporção de posição pode ser ajustada dinamicamente de acordo com a volatilidade do mercado.

- Reforço do mecanismo de stop loss: Pode ser combinado com o preço médio para projetar uma lógica de stop loss mais complexa.

- Otimização do timing de entrada: A análise da estrutura de preços pode ser adicionada para melhorar a precisão das entradas.

- Aperfeiçoamento do sistema de backtesting: Podem ser adicionados mais indicadores estatísticos para avaliar o desempenho da estratégia.

Resumo

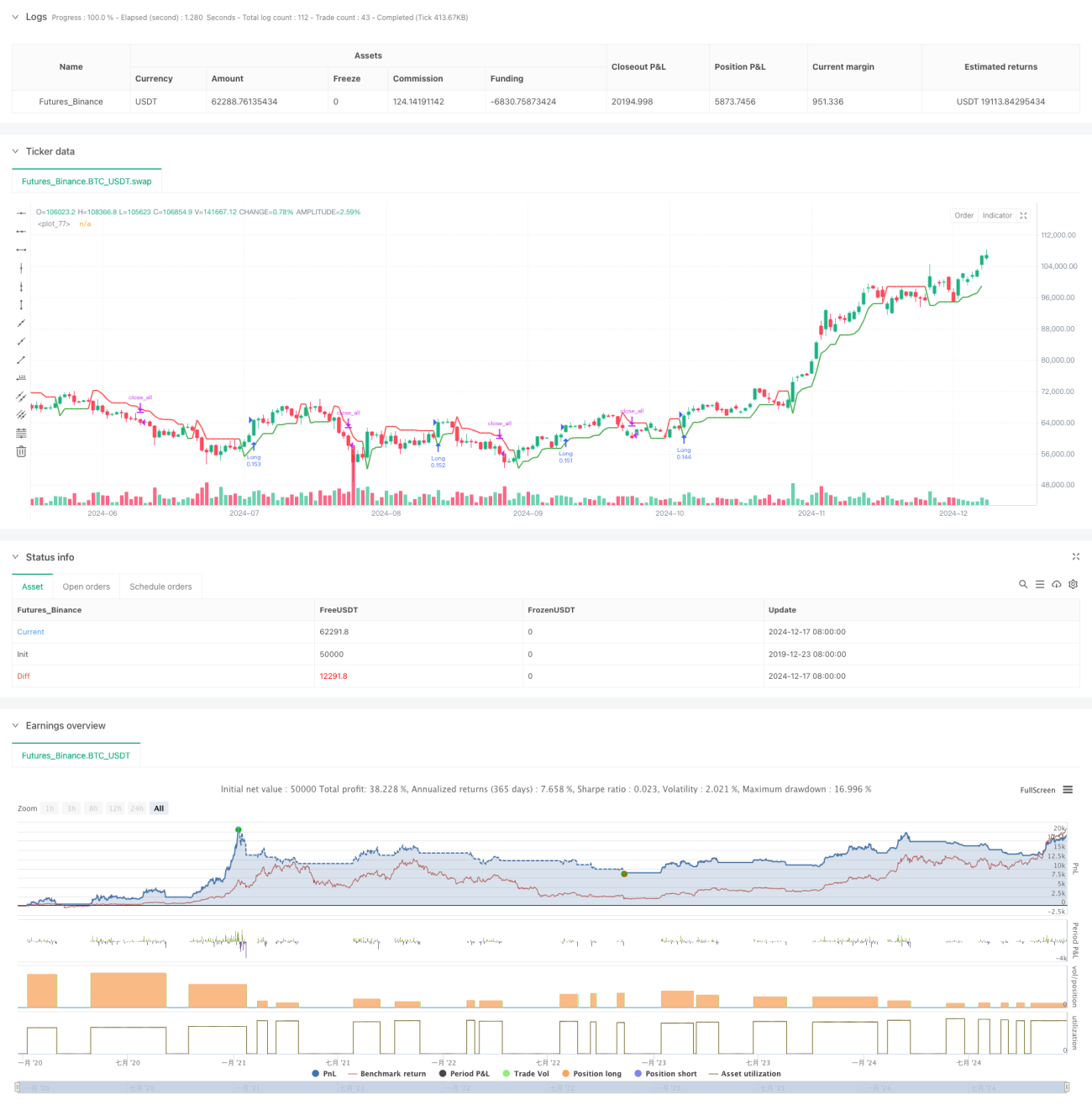

Esta é uma estratégia de acompanhamento de tendência bem projetada e com risco controlável. Ao combinar o indicador Supertrend com um mecanismo flexível de stop loss, a estratégia pode manter alta rentabilidade enquanto controla eficazmente o risco. A estratégia possui alta capacidade de configuração, sendo adequada para uso em diferentes condições de mercado, mas requer otimização completa de parâmetros e validação por backtesting. No futuro, a estabilidade e a lucratividade da estratégia podem ser melhoradas com a adição de mais ferramentas de análise técnica e medidas de controle de risco.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Supertrend Strategy with Adjustable Trailing Stop [Bips]", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15)

// Inputs- 1