Visão Geral

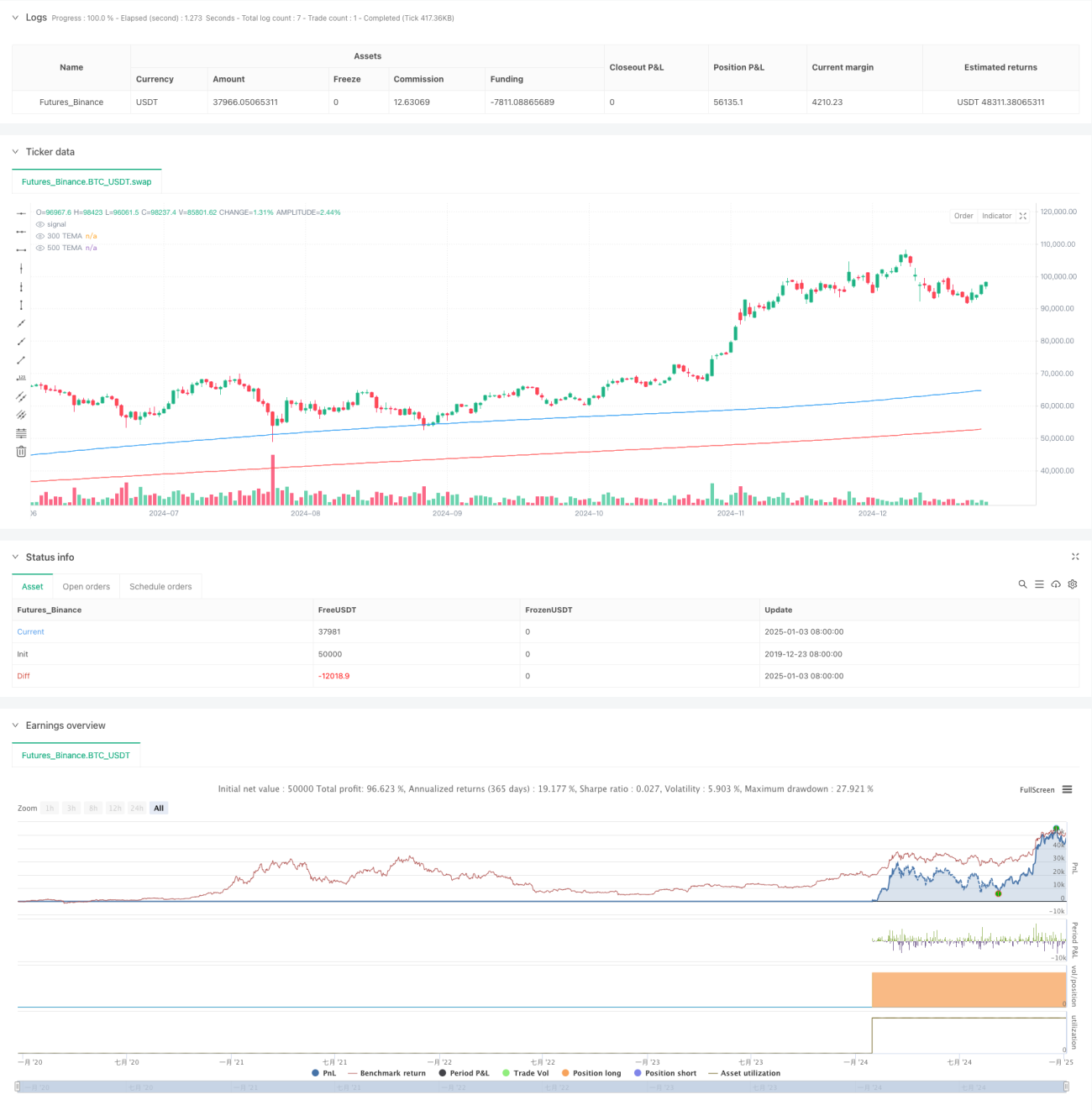

Esta estratégia é um sistema de negociação de acompanhamento de tendências baseado na Média Móvel Exponencial Tripla (TEMA). A estratégia captura tendências de mercado através da comparação dos sinais de cruzamento entre TEMA de curto e longo prazo, combinando stop loss por volatilidade para gerenciar riscos. Opera no timeframe de 5 minutos, utilizando indicadores TEMA de períodos 300 e 500 como base para a geração de sinais.

Princípio da Estratégia

A lógica central da estratégia baseia-se nos seguintes elementos-chave:

- Utilização de dois indicadores TEMA com diferentes períodos (300 e 500) para identificar a direção da tendência.

- Quando a TEMA de curto prazo cruza para cima a TEMA de longo prazo, o sistema gera um sinal de compra.

- Quando a TEMA de curto prazo cruza para baixo a TEMA de longo prazo, o sistema gera um sinal de venda.

- Utilização das máximas e mínimas de 10 períodos para definir o nível de stop loss.

- Após a entrada, a posição é mantida até que um sinal contrário seja gerado para o fechamento.

Vantagens da Estratégia

- Alta estabilidade dos sinais: o uso de TEMA com períodos mais longos filtra eficazmente o ruído do mercado, reduzindo sinais falsos.

- Controle de risco completo: combinado com stop loss por volatilidade, controla eficazmente o risco por operação.

- Forte capacidade de captura de tendências: a TEMA reage mais rapidamente às tendências do que as médias móveis tradicionais.

- Ciclo de negociação completo: inclui condições claras de entrada, stop loss e realização de lucros.

- Alta ajustabilidade de parâmetros: os parâmetros principais podem ser flexivelmente ajustados conforme as características do mercado.

Riscos da Estratégia

- Risco de mercado lateral: em mercados laterais, pode gerar sinais falsos, levando a perdas consecutivas.

- Risco de slippage: no timeframe de 5 minutos, pode haver slippage significativo durante movimentos bruscos.

- Risco de gestão de capital: um stop loss com pontos fixos pode resultar em perdas excessivas durante alta volatilidade.

- Atraso do sinal: o indicador TEMA possui inerentemente um certo atraso, podendo perder o ponto ideal de entrada.

- Sensibilidade a parâmetros: os parâmetros ideais variam significativamente em diferentes ambientes de mercado.

Direções de Otimização da Estratégia

- Adicionar identificação do ambiente de mercado: incluir indicadores de força de tendência, utilizando parâmetros diferentes em diferentes ambientes.

- Otimizar o método de stop loss: considerar o uso de stop loss dinâmico baseado no ATR para melhorar a adaptabilidade.

- Melhorar a gestão de posição: ajustar dinamicamente o tamanho da posição com base na força da tendência.

- Adicionar mecanismo de alerta: emitir sinais de alerta antecipados em níveis de preço chave.

- Incluir indicador de volume: combinar com o volume para confirmar a validade dos sinais.

Resumo

Esta estratégia é um sistema completo de acompanhamento de tendências, que captura a tendência através do cruzamento do indicador TEMA, combinado com stop loss dinâmico para gerenciamento de risco. A lógica da estratégia é clara, implementação simples e possui boa praticidade. No entanto, na negociação ao vivo, é necessário prestar atenção à identificação do ambiente de mercado e ao controle de risco. Recomenda-se, com base em backtests validados, otimizar os parâmetros de acordo com as condições reais do mercado.

- 1