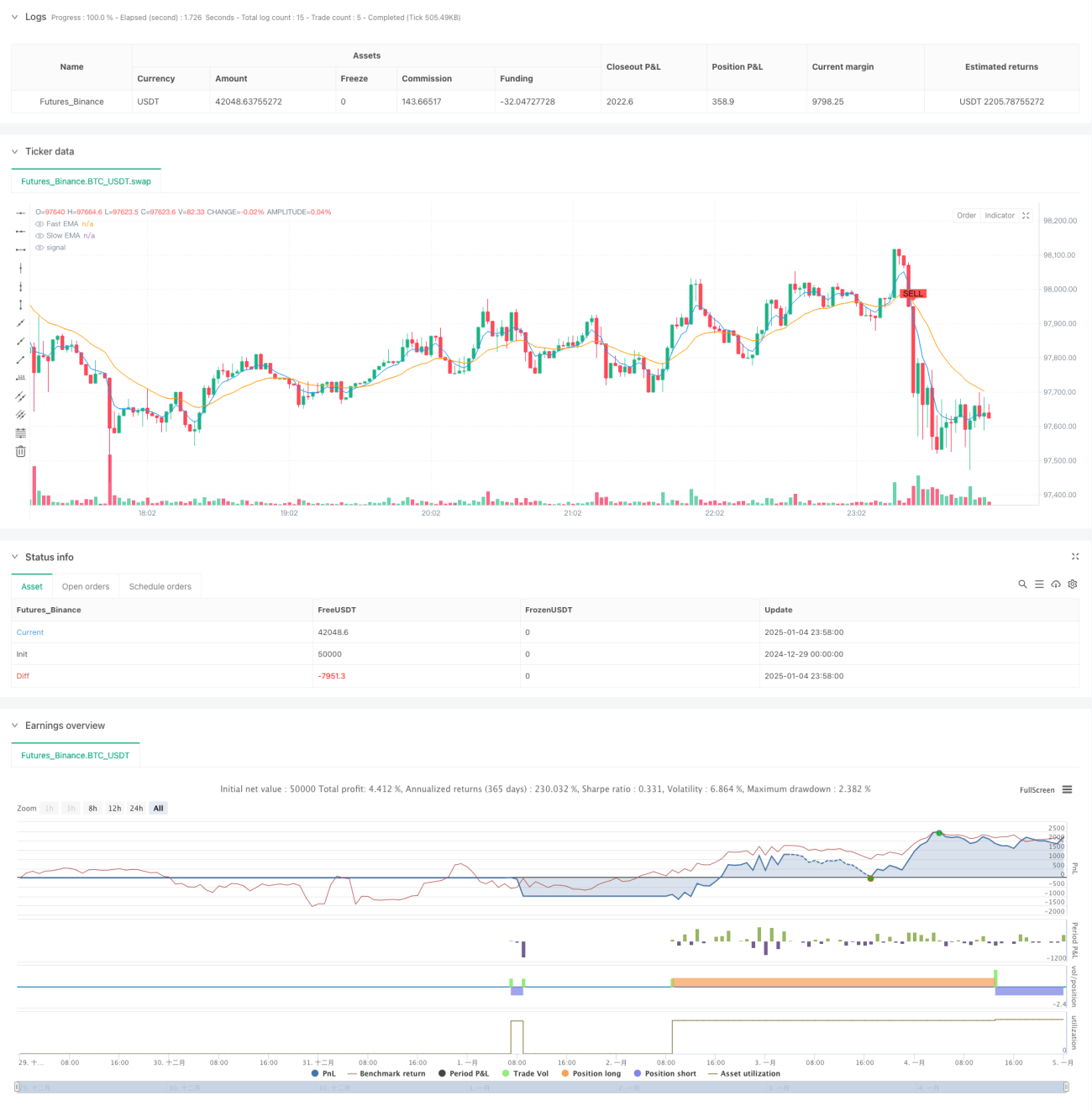

Visão Geral

Esta estratégia é um sistema de negociação de acompanhamento de tendência que combina sinais de cruzamento de médias móveis com gerenciamento de risco dinâmico. Utiliza médias exponenciais (EMA) rápidas e lentas para identificar tendências de mercado e incorpora o indicador Average True Range (ATR) para otimizar o timing de entrada. Ao mesmo tempo, a estratégia integra um mecanismo de proteção triplo composto por stop loss percentual, take profit e trailing stop.

Princípio da Estratégia

A lógica central da estratégia baseia-se nos seguintes elementos-chave:

- Utiliza o cruzamento das EMAs de 5 e 20 períodos para determinar a direção da tendência

- Filtra a confiabilidade dos sinais de negociação por meio de múltiplos do ATR

- Gera sinais de negociação quando ocorre o cruzamento da EMA e o preço rompe o canal do ATR

- Após a abertura da posição, define imediatamente um stop loss fixo de 1% e um take profit de 5%

- Utiliza um trailing stop baseado no ATR para proteger os lucros

- Opera em ambos os lados (long e short), aproveitando plenamente as oportunidades de mercado

Vantagens da Estratégia

- O sistema de sinais combina indicadores de tendência e volatilidade, aumentando a precisão das negociações

- O canal ATR dinâmico adapta-se às características de volatilidade em diferentes ambientes de mercado

- O mecanismo de controle de risco triplo oferece proteção abrangente para as negociações

- Alta flexibilidade na parametrização, facilitando a otimização conforme as características do mercado

- Alto grau de automação, reduzindo o impacto emocional da intervenção humana

Riscos da Estratégia

- O cruzamento de EMAs pode gerar atraso, podendo perder o ponto ideal de entrada em mercados com volatilidade extrema

- Stop loss percentual fixo pode ser inflexível em períodos de alta volatilidade

- Negociações frequentes podem resultar em custos elevados de comissões

- Em mercados laterais, podem ocorrer sinais falsos frequentes

- O trailing stop pode fechar a posição prematuramente durante recuos rápidos

Direções de Otimização da Estratégia

- Introduzir indicadores de volume para validar a eficácia da tendência

- Adicionar um mecanismo de identificação de ambiente de mercado, utilizando parâmetros diferentes em estados de mercado distintos

- Otimizar os múltiplos do ATR, estabelecendo um sistema de parâmetros dinâmicos adaptativos

- Combinar mais indicadores técnicos para filtrar sinais falsos

- Desenvolver um plano de gerenciamento de capital mais flexível

Resumo

Trata-se de uma estratégia de acompanhamento de tendência bem projetada e logicamente clara. Captura tendências por meio do cruzamento de médias móveis, controla riscos utilizando o ATR e conta com mecanismos de stop múltiplos, formando um sistema de negociação completo. A principal vantagem da estratégia reside no seu controle de risco abrangente e na alta customização. No entanto, em negociações ao vivo, deve-se atentar para os sinais falsos e os custos de transação. Com as direções de otimização sugeridas, a estratégia ainda possui espaço para melhorias adicionais.

/*backtest

start: 2024-12-29 00:00:00

end: 2025-01-05 00:00:00

period: 2m

basePeriod: 2m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © jesusperezguitarra89

//@version=6- 1