Estratégia de Rastreamento de Tendência de Múltiplas Médias Móveis com Filtro de Volatilidade Dinâmica

Visão Geral

Esta estratégia é um sistema de negociação inteligente que combina trend following (seguimento de tendência) com filtro de volatilidade. Ela identifica a tendência do mercado por meio da Média Móvel Exponencial (EMA), utiliza o True Range (TR) e um filtro dinâmico de volatilidade para determinar o momento de entrada, e gerencia o risco com mecanismos dinâmicos de take profit e stop loss baseados na volatilidade. A estratégia suporta dois modos de negociação: Scalp (curto prazo) e Swing (médio prazo), permitindo alternar de forma flexível conforme as diferentes condições de mercado e estilos de negociação.

Princípio da Estratégia

A lógica central da estratégia inclui os seguintes componentes-chave:

- Identificação de Tendência: Utiliza uma EMA de 50 períodos como filtro de tendência, operando comprado apenas quando o preço está acima da EMA e vendido quando está abaixo.

- Filtro de Volatilidade: Calcula a EMA do True Range (TR) e utiliza um coeficiente de filtro ajustável (padrão 1,5) para eliminar ruídos do mercado.

- Condições de Entrada: Combina a análise da formação de 3 velas consecutivas, exigindo que o movimento do preço apresente continuidade e aceleração.

- Take Profit e Stop Loss: No modo Scalp, são definidos com base no TR atual; no modo Swing, com base nos pontos máximos e mínimos anteriores, proporcionando gerenciamento dinâmico de risco.

Vantagens da Estratégia

- Alta Adaptabilidade: A combinação de filtro de volatilidade dinâmico com trend following permite adaptar-se a diferentes condições de mercado.

- Gestão de Risco Robusta: Oferece mecanismos dinâmicos de take profit e stop loss para dois modos de negociação, que podem ser escolhidos de acordo com as características do mercado.

- Boa Ajustabilidade de Parâmetros: Parâmetros-chave, como o coeficiente de filtro e o período da tendência, podem ser otimizados conforme as particularidades do ativo negociado.

- Boa Visualização: Fornece marcações claras de sinais de compra/venda e exibição dos níveis de take profit e stop loss, facilitando o monitoramento da negociação.

Riscos da Estratégia

- Risco de Reversão de Tendência: Podem ocorrer stop losses consecutivos em pontos de reversão da tendência.

- Risco de Falso Rompimento: A volatilidade repentina pode gerar sinais falsos.

- Sensibilidade a Parâmetros: Um coeficiente de filtro mal ajustado pode resultar em excesso ou escassez de sinais.

- Impacto do Slippage: Em mercados rápidos, pode haver slippage significativo, afetando o desempenho da estratégia.

Direções para Otimização da Estratégia

- Adicionar Filtro de Força da Tendência: Introduzir indicadores como ADX para avaliar a força da tendência, melhorando o acompanhamento da mesma.

- Otimizar Take Profit e Stop Loss: Considerar a implementação de stop loss móvel para proteger mais lucros.

- Aprimorar o Modo Swing: Adicionar mais condições de julgamento específicas para negociações de swing, aumentando a capacidade de manter posições de médio/longo prazo.

- Incluir Análise de Volume: Combinar variações de volume para confirmar a validade dos rompimentos.

Resumo

Esta estratégia constrói um sistema de negociação completo ao integrar trend following, filtro de volatilidade e gestão dinâmica de risco. Suas vantagens residem na forte adaptabilidade, risco controlável e amplo espaço para otimização. Com a configuração adequada dos parâmetros e a escolha correta do modo de negociação, a estratégia pode manter um desempenho estável em diferentes condições de mercado. Recomenda-se que os traders realizem backtests completos e otimizações de parâmetros antes de usar a estratégia ao vivo, ajustando-a de acordo com as características específicas do ativo negociado.

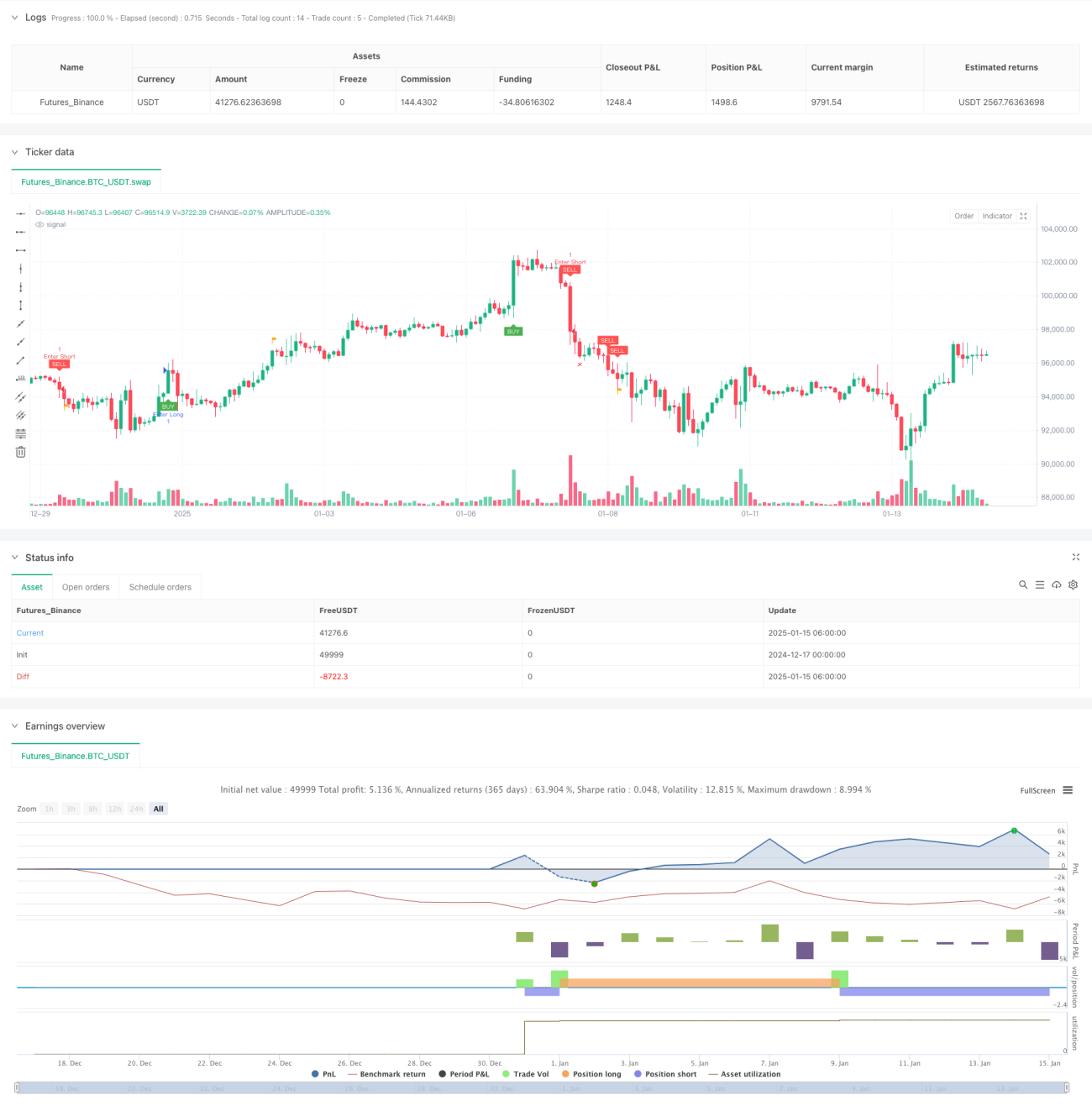

/*backtest

start: 2024-12-17 00:00:00

end: 2025-01-15 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Creativ3mindz

//@version=5- 1