Estratégia de Negociação Multi-Indicador de Momentum de Tendência e Preço-Alvo ATR

Visão Geral

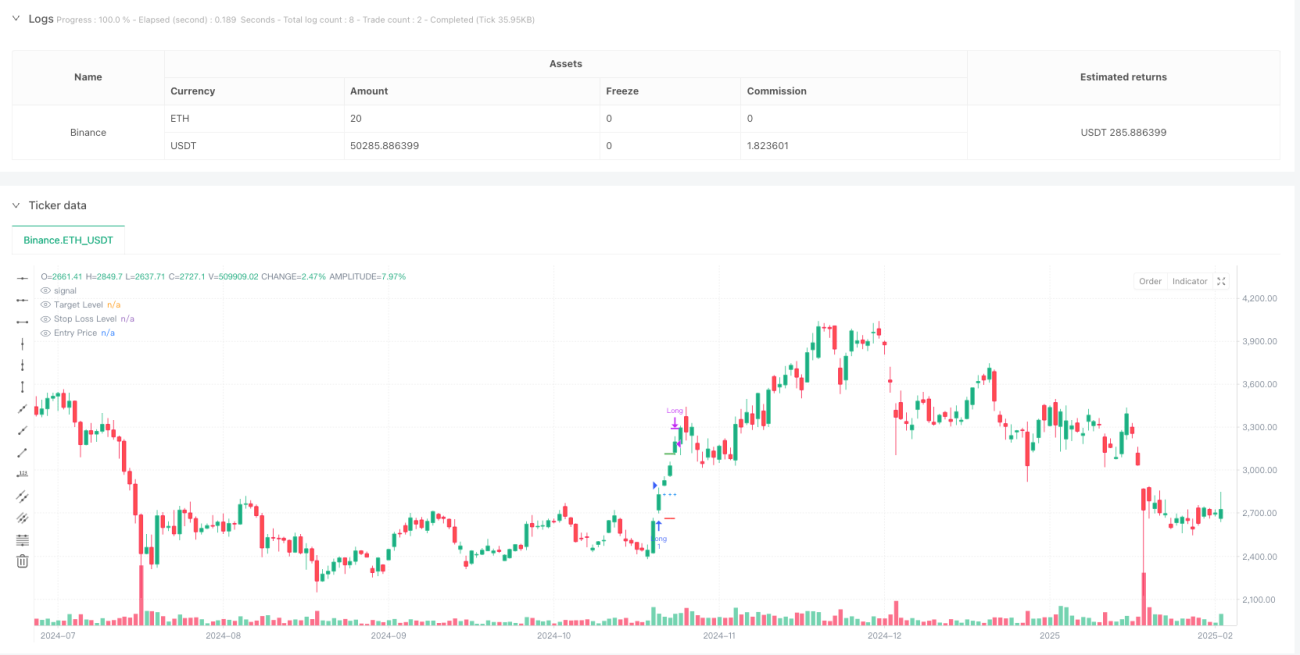

Esta estratégia é um sistema de negociação de acompanhamento de tendência e momentum baseado em múltiplos indicadores técnicos. Ela combina principalmente o Índice de Movimento Direcional Médio (ADX), o Índice de Força Relativa (RSI) e o Average True Range (ATR) para identificar potenciais oportunidades de compra, utilizando o ATR para definir níveis dinâmicos de lucro e stop loss. A estratégia é particularmente adequada para negociação de opções no timeframe de 1 minuto, aumentando a taxa de sucesso através de condições de entrada rigorosas e gerenciamento de risco.

Princípio da Estratégia

A lógica central da estratégia inclui os seguintes componentes principais:

- Confirmação de Tendência: Usar ADX > 18 e +DI maior que -DI para confirmar que o mercado está em tendência de alta.

- Verificação de Momentum: Exigir que o RSI ultrapasse 60 e esteja acima de sua média móvel de 20 períodos para validar o momentum do preço.

- Momento de Entrada: Quando as condições de tendência e momentum são simultaneamente atendidas, o sistema abre uma posição comprada no preço de fechamento atual.

- Gerenciamento de Metas: Definir uma meta de lucro dinâmica (2,5 vezes o ATR) e um stop loss (1,5 vezes o ATR) com base no valor do ATR no momento da entrada.

Vantagens da Estratégia

- Confirmação Multidimensional: Fornece sinais de negociação mais confiáveis ao combinar indicadores de tendência e momentum.

- Gerenciamento de Risco Dinâmico: Utiliza o ATR para ajustar dinamicamente os níveis de stop gain e stop loss, adaptando-se às mudanças na volatilidade do mercado.

- Regras de Negociação Claras: As condições de entrada e saída são explícitas, reduzindo a interferência de julgamentos subjetivos.

- Alta Adaptabilidade: Os parâmetros da estratégia podem ser otimizados e ajustados para diferentes ambientes de mercado e instrumentos negociados.

Riscos da Estratégia

- Risco de Falso Rompimento: O RSI ultrapassar 60 pode gerar sinais falsos, exigindo validação por outros indicadores.

- Impacto do Slippage: Em mercados rápidos no timeframe de 1 minuto, pode haver um risco significativo de slippage.

- Dependência do Ambiente de Mercado: A estratégia apresenta melhor desempenho em mercados com tendência clara; em mercados laterais, pode acionar stops com frequência.

- Sensibilidade a Parâmetros: A configuração de múltiplos parâmetros dos indicadores precisa ser equilibrada; combinações inadequadas podem afetar o desempenho da estratégia.

Direções de Otimização da Estratégia

- Otimização da Entrada: Adicionar um mecanismo de confirmação de volume para aumentar a confiabilidade dos sinais.

- Gerenciamento de Posição: Introduzir um sistema de gerenciamento de posição dinâmico, ajustando o tamanho da posição de acordo com a volatilidade do mercado.

- Mecanismo de Saída: Considerar a adição de uma função de stop loss móvel (trailing stop) para proteger melhor os lucros.

- Filtro de Horário: Adicionar um filtro de janela de negociação para evitar períodos com volatilidade excessiva ou liquidez insuficiente.

Resumo

Esta estratégia constrói um sistema de negociação completo através do uso integrado de múltiplos indicadores técnicos. Sua vantagem reside na combinação de análises de tendência e momentum, juntamente com uma abordagem dinâmica de gerenciamento de risco. Embora existam certos riscos, ela pode alcançar um desempenho estável em negociações reais por meio de otimização adequada de parâmetros e medidas de controle de risco. Recomenda-se que os traders realizem backtests e otimizações de parâmetros suficientes antes de usar a estratégia em conta real, e façam os ajustes adequados de acordo com as características específicas do instrumento negociado.

- 1