Visão Geral

Esta estratégia é um sistema de negociação de swing baseado em múltiplos períodos, utilizando o Oscilador Estocástico (Stochastic Oscillator). Ela combina sinais do oscilador estocástico no período atual e em um período superior para identificar oportunidades de negociação, e emprega um sistema dinâmico de stop loss e take profit para gerenciar riscos. A estratégia é adequada para mercados voláteis, visando capturar flutuações de curto prazo nos preços para obter ganhos.

Princípio da Estratégia

A lógica central da estratégia baseia-se nos seguintes elementos-chave:

- Utiliza o oscilador estocástico em dois períodos (atual e superior) para confirmação de sinais.

- Busca sinais de cruzamento nas zonas de sobrecompra e sobrevenda.

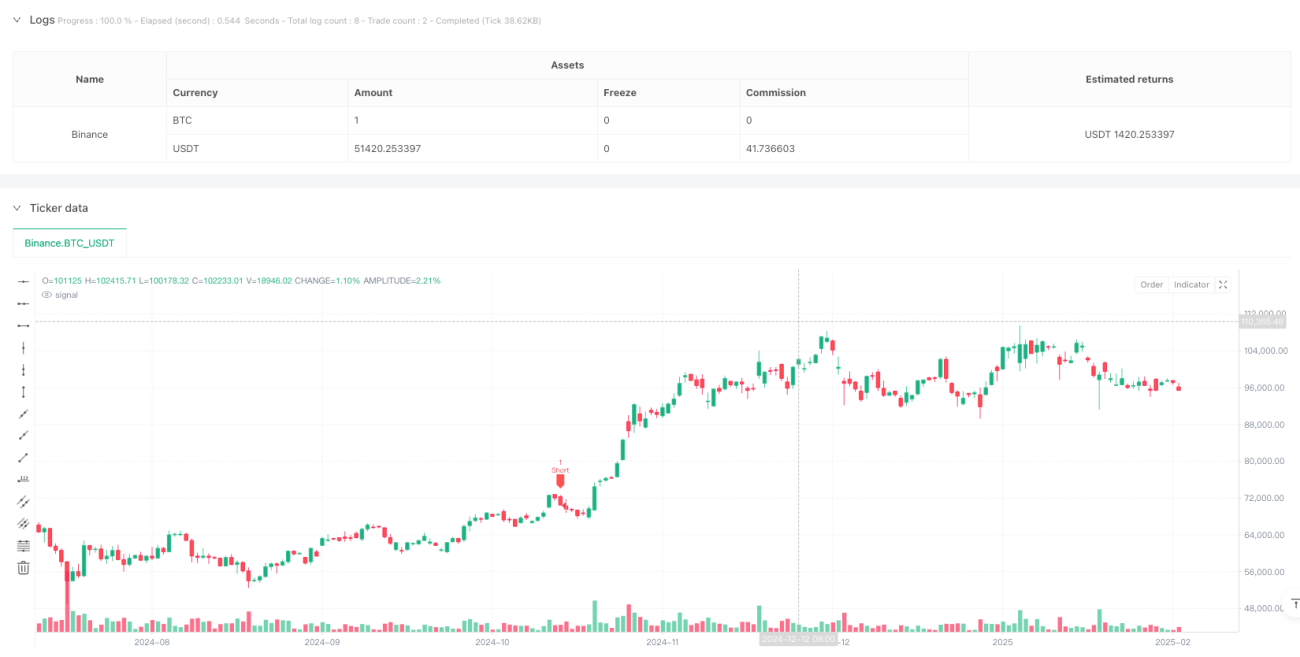

- Condição de compra: linha K do período atual cruza acima da linha D, com valor K < 20; no período superior, valor K < 20 e K > D.

- Condição de venda: linha K do período atual cruza abaixo da linha D, com valor K > 80; no período superior, valor K > 80 e K < D.

- Adota um sistema dinâmico de stop loss e take profit baseado no preço de entrada, com múltiplos ajustáveis.

Vantagens da Estratégia

- A confirmação de sinais em múltiplos períodos aumenta a confiabilidade das negociações, reduzindo efetivamente sinais falsos.

- Operar nas zonas de sobrecompra e sobrevenda aumenta a probabilidade de reversão de tendência.

- O sistema dinâmico de stop loss e take profit se ajusta automaticamente às oscilações do mercado, proporcionando maior flexibilidade no gerenciamento de capital.

- A interface gráfica exibe claramente os sinais de negociação e as posições de stop loss/take profit, facilitando a compreensão e operação do trader.

- Os parâmetros da estratégia são ajustáveis, adaptando-se a diferentes condições de mercado.

Riscos da Estratégia

- Em mercados com volatilidade extrema, podem ocorrer stops frequentes.

- A confirmação em dois períodos pode levar à perda de algumas oportunidades de negociação.

- Múltiplos fixos de stop loss e take profit podem não ser adequados para todos os ambientes de mercado.

- Em tendências fortes, pode ocorrer take profit prematuro.

- É necessário ajustar os parâmetros adequadamente para equilibrar retorno e risco.

Direções de Otimização

- Introduzir mecanismos adaptativos de stop loss e take profit, ajustando dinamicamente com base na volatilidade do mercado.

- Adicionar um filtro de tendência para ajustar a direção das negociações em tendências fortes.

- Incluir indicadores de volume como confirmação auxiliar de sinais.

- Desenvolver um sistema de gerenciamento de posição mais inteligente.

- Considerar a incorporação de indicadores de sentimento do mercado para otimizar o momento de entrada.

Resumo

Esta é uma estratégia de negociação completa que combina análise técnica e gerenciamento de riscos. Através da confirmação de sinais em múltiplos períodos e de um sistema dinâmico de stop loss e take profit, a estratégia oferece boa estabilidade e potencial de lucro. No entanto, o usuário deve otimizar os parâmetros de acordo com seu estilo de negociação e as condições do mercado, mantendo sempre um rigoroso controle de risco.

- 1