Sistema de Trading de Tendência Inteligente, Multidimensional e Adaptativo

Visão Geral

Esta estratégia é um sistema de negociação inteligente que integra múltiplos indicadores técnicos, identificando oportunidades de mercado por meio de uma análise combinada de Fair Value Gap (FVG), sinais de tendência e ação de preço. O sistema utiliza um mecanismo de estratégia dupla, combinando características de acompanhamento de tendência e swing trading, otimizando o desempenho por meio de gerenciamento dinâmico de posição e mecanismos de saída multidimensionais. A estratégia prioriza o controle de risco, melhorando a qualidade dos sinais através de filtragem de volatilidade e confirmação de volume.

Princípios da Estratégia

A lógica central da estratégia baseia-se nas seguintes dimensões:

- Identificação do Gap FVG – calcula o tamanho dos gaps de preço para encontrar potenciais oportunidades de negociação.

- Sistema de Confirmação de Tendência – combina a média móvel de 200 períodos, o indicador SuperTrend e o MACD para confirmar a tendência do mercado.

- Confirmação de Capital Inteligente – utiliza sobrecompra/sobrevenda do RSI, anomalias de volume e padrões de ação de preço como condições de disparo.

- Gerenciamento Dinâmico de Posição – ajusta o tamanho da posição com base na volatilidade (ATR), garantindo exposição de risco consistente.

- Mecanismo de Saída em Múltiplos Níveis – combina stop-loss móvel e take-profit fixo para gerenciar a saída das operações.

Vantagens da Estratégia

- Alta Adaptabilidade – ajusta parâmetros e posições automaticamente conforme a volatilidade do mercado.

- Controle de Risco Robusto – gerencia riscos por meio de múltiplos filtros e gerenciamento rigoroso de posição.

- Sinais Confiáveis – aumenta a precisão dos sinais através da confirmação de indicadores multidimensionais.

- Flexibilidade Operacional – captura oportunidades tanto em tendências quanto em mercados laterais.

- Gestão de Capital Científica – utiliza gerenciamento de risco percentual para garantir uso racional do capital.

Riscos da Estratégia

- Sensibilidade a Parâmetros – a configuração de múltiplos parâmetros pode afetar o desempenho, exigindo otimização contínua.

- Dependência do Ambiente de Mercado – pode gerar sinais falsos de rompimento em certas condições de mercado.

- Impacto do Slippage – em mercados com baixa liquidez, pode haver grande derrapagem.

- Complexidade Computacional – o cálculo de múltiplos indicadores pode causar atraso nos sinais.

- Exigência de Capital Elevada – a implementação completa da estratégia requer um capital inicial significativo.

Direções de Otimização

- Otimização de Pesos dos Indicadores – pode-se introduzir aprendizado de máquina para ajustar dinamicamente os pesos de cada indicador.

- Melhoria da Adaptabilidade ao Mercado – adicionar mecanismos adaptativos de volatilidade do mercado.

- Aprimoramento da Filtragem de Sinais – incorporar mais indicadores de microestrutura do mercado.

- Otimização do Mecanismo de Execução – adicionar divisão inteligente de ordens para reduzir custos de impacto.

- Atualização do Controle de Risco – incluir sistema dinâmico de gerenciamento de orçamento de risco.

Resumo

Esta estratégia constrói um sistema de negociação completo através da aplicação integrada de múltiplos indicadores técnicos e técnicas de negociação. Sua vantagem reside na capacidade de se adaptar às mudanças do mercado, mantendo um controle de risco rigoroso. Embora existam espaços para otimização, no geral é uma estratégia quantitativa de trading bem projetada.

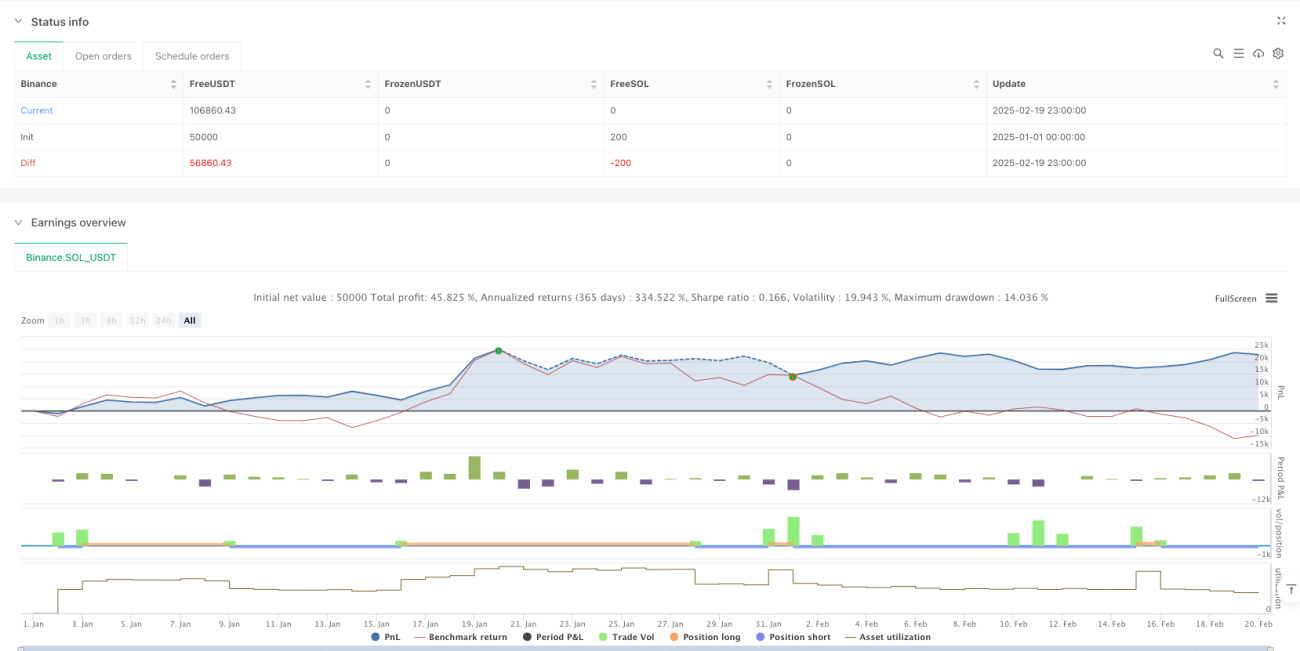

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1