Visão Geral

Esta é uma estratégia de negociação intradiária baseada em múltiplos indicadores técnicos, utilizando principalmente canais EMA, sobrecompra/sobrevenda do RSI, confirmação de tendência do MACD e outros sinais múltiplos. A estratégia opera no período de 3 minutos, capturando tendências de mercado através da combinação das bandas superior e inferior da EMA com a confirmação de cruzamento do RSI e MACD, e possui stops dinâmicos baseados no ATR, take profit e um horário fixo de fechamento das posições.

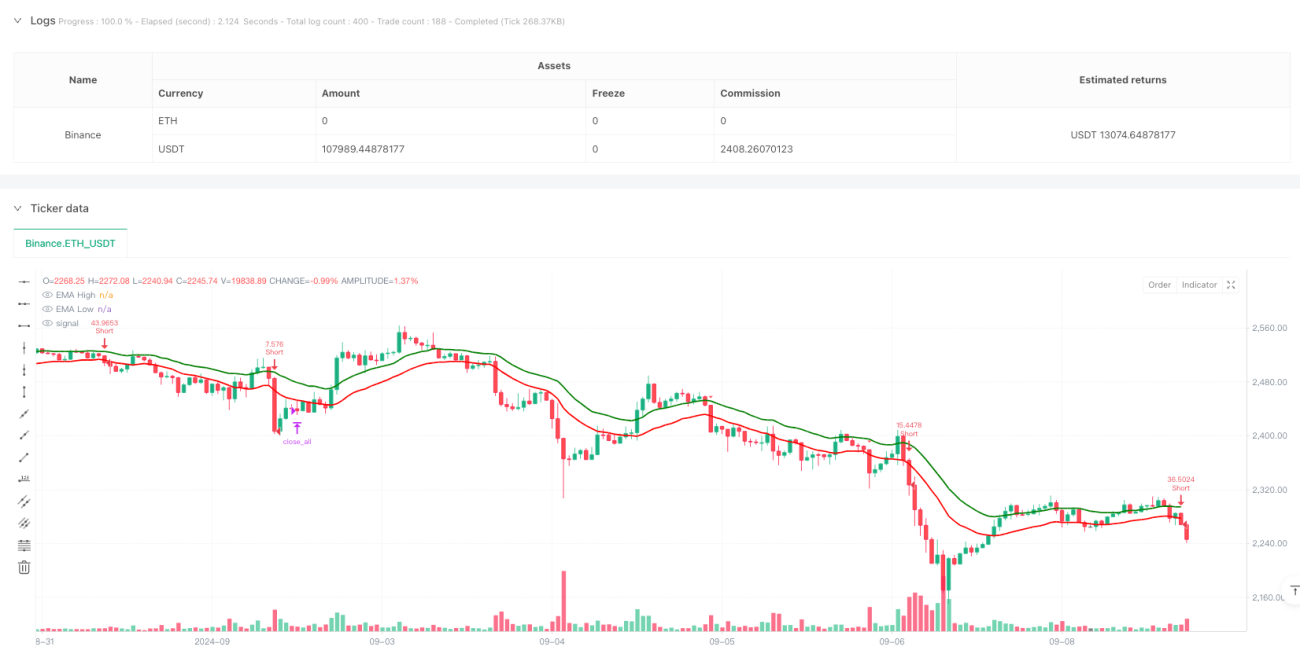

Princípio da Estratégia

A estratégia utiliza uma EMA de 20 períodos aplicada separadamente ao preço máximo e mínimo para formar um canal. Quando o preço rompe o canal e as seguintes condições são atendidas, ocorre a entrada:

- Entrada comprada: preço de fechamento cruza acima da banda superior da EMA, RSI entre 50-70, linha MACD cruza acima da linha de sinal.

- Entrada vendida: preço de fechamento cruza abaixo da banda inferior da EMA, RSI entre 30-50, linha MACD cruza abaixo da linha de sinal.

- Utiliza o ATR para calcular dinamicamente a posição do stop loss, com take profit definido com base em uma relação risco-retorno de 2,5x.

- O risco por operação é de 1% da conta, com o tamanho da posição calculado dinamicamente com base na distância do stop loss.

- Todas as posições são forçadas a fechar às 15:00, horário padrão da Índia.

Vantagens da Estratégia

- Múltiplos indicadores técnicos com validação cruzada, aumentando a confiabilidade dos sinais de negociação.

- Stop loss dinâmico baseado no indicador ATR, adaptando-se melhor à volatilidade do mercado.

- Relação de risco fixa e relação risco-retorno, controlando efetivamente o risco.

- Considera os custos de negociação, incluindo o cálculo de taxas.

- Proíbe o aumento de posição na mesma direção, evitando risco de exposição excessiva.

- Horário fixo de fechamento, evitando riscos overnight.

Riscos da Estratégia

- Múltiplos indicadores podem causar atraso nos sinais, afetando o momento da entrada.

- O canal EMA pode gerar falsos rompimentos frequentes em mercados laterais.

- A relação risco-retorno fixa pode não ser flexível o suficiente em diferentes condições de mercado.

- As faixas de RSI podem perder algumas grandes tendências de mercado.

- O fechamento forçado no horário fixo pode forçar a saída em momentos críticos.

Direções de Otimização

- Considerar adicionar o indicador de volume como confirmação auxiliar.

- Ajustar dinamicamente a relação risco-retorno com base nas características de volatilidade de diferentes períodos.

- Introduzir um indicador de volatilidade do mercado para ajustar dinamicamente os limites do RSI.

- Considerar a adição de um filtro de força de tendência para reduzir falsos rompimentos.

- Ajustar parâmetros com base nas características de diferentes períodos intradiários.

- Adicionar análise de volatilidade histórica para otimizar o gerenciamento de posições.

Resumo

Esta estratégia constrói um sistema de negociação relativamente completo através da combinação de múltiplos indicadores técnicos. Sua principal vantagem está no controle de risco bem elaborado, incluindo stop loss dinâmico, risco fixo e mecanismo de fechamento no horário determinado. Embora exista um certo risco de atraso, o desempenho pode ser melhorado através da otimização de parâmetros e da adição de indicadores auxiliares. A estratégia é especialmente adequada para mercados intradiários de alta volatilidade, buscando retornos estáveis por meio de controle de risco rigoroso e confirmação de múltiplos sinais.

- 1