Visão Geral

A Estratégia de Negociação Inteligente com Múltiplos Indicadores Ponderados é um sistema de negociação quantitativo abrangente que gera decisões de negociação integrando sinais de múltiplos indicadores técnicos e atribuindo pesos diferentes a eles. A estratégia combina várias ferramentas de análise técnica, como MACD, RSI Estocástico, EMA, Super Trend e Cruzamento de Médias Móveis, formando um quadro de negociação completo. O sistema não apenas suporta mecanismos de take profit em múltiplos níveis e stop loss dinâmico, mas também ajusta automaticamente os parâmetros de negociação de acordo com as condições do mercado, mantendo alta adaptabilidade em diferentes ambientes de mercado. Essa estratégia é particularmente adequada para traders de médio a longo prazo, tornando as decisões de negociação mais robustas e confiáveis por meio de um sistema de ponderação.

Princípio da Estratégia

O núcleo da estratégia está em seu sistema de sinais ponderados, que gera sinais de negociação por meio de cinco subestratégias diferentes:

-

Estratégia MACD: Utiliza o cruzamento da linha MACD com a linha de sinal para determinar a direção da tendência do mercado. Quando a linha MACD cruza acima da linha de sinal, gera um sinal de compra; quando cruza abaixo, gera um sinal de venda.

-

Estratégia RSI Estocástico: Combina as vantagens do RSI e do oscilador estocástico para monitorar as condições de sobrecompra e sobrevenda do mercado. Quando o RSI Estocástico fica abaixo do limite de sobrevenda definido, gera um sinal de compra; quando fica acima do limite de sobrecompra, gera um sinal de venda.

-

Estratégia EMA de Sobrecompra/Sobrevenda: Usa a EMA para identificar o grau de desvio do preço em relação à média. Quando o RSI fica abaixo do limite de sobrevenda definido, gera um sinal de compra; quando fica acima do limite de sobrecompra, gera um sinal de venda.

-

Estratégia Super Trend: Define um canal de preços com base em múltiplos do ATR e determina a direção da negociação por meio de mudanças na tendência. Quando o indicador Super Trend muda de negativo para positivo, gera um sinal de compra; quando muda de positivo para negativo, gera um sinal de venda.

-

Estratégia de Cruzamento de Médias Móveis: Utiliza o cruzamento de duas médias móveis com períodos diferentes para determinar a tendência do mercado. Quando a média móvel de curto prazo cruza acima da média de longo prazo, gera um sinal de compra; quando cruza abaixo, gera um sinal de venda.

A estratégia calcula ponderações dos sinais de cada subestratégia por meio de um sistema de pesos personalizável, executando a negociação apenas quando a soma ponderada excede o limite definido. Além disso, a estratégia inclui um mecanismo de identificação de topos e fundos potenciais, permitindo ajustar as posições quando o mercado pode reverter.

Esse mecanismo de confirmação de sinais em múltiplas camadas reduz efetivamente os sinais falsos, melhorando a confiabilidade do sistema de negociação, enquanto as configurações flexíveis de parâmetros permitem que a estratégia se adapte a diferentes instrumentos de negociação e períodos de tempo.

Vantagens da Estratégia

-

Confirmação Múltipla de Sinais: Os sinais gerados por cinco indicadores técnicos independentes são ponderados, reduzindo os enganos que um único indicador poderia causar e melhorando a qualidade e confiabilidade dos sinais de negociação.

-

Sistema de Pesos Adaptável: Cada subestratégia pode receber pesos diferentes, permitindo que o trader ajuste o foco da estratégia com base em sua confiança em cada indicador e no desempenho histórico, aumentando a flexibilidade da estratégia.

-

Gerenciamento de Risco Completo: A estratégia incorpora mecanismos de controle de risco em múltiplos níveis, incluindo stop loss, take profit em múltiplos níveis e ajuste dinâmico do stop loss, garantindo que os riscos possam ser controlados rapidamente em movimentos desfavoráveis do mercado.

-

Identificação Automática de Topos e Fundos Potenciais: Por meio da análise combinada de RSI, volume de negociação e movimento de preços, a estratégia pode identificar topos e fundos potenciais do mercado, fechando parcialmente as posições no momento adequado para travar lucros ou reduzir perdas.

-

Alta Personalização: Quase todos os parâmetros podem ser ajustados, incluindo períodos de cálculo de cada indicador, valores de pesos, percentuais de take profit/stop loss, etc., permitindo que o trader otimize a estratégia de acordo com seu estilo pessoal e diferentes condições de mercado.

-

Mecanismo de Atraso Incorporado: Para evitar entrar em negociações prematuramente ou com base em sinais de ruído, a estratégia adota um mecanismo de confirmação com atraso, garantindo que apenas sinais sustentados acionem negociações, reduzindo o impacto das flutuações de curto prazo.

-

Filtro Temporal: A estratégia permite definir datas de início e término das negociações, permitindo que o trader teste o desempenho em períodos específicos com base em dados históricos ou evite períodos de volatilidade anormal conhecida.

Riscos da Estratégia

-

Risco de Sobreajuste de Parâmetros: Devido ao grande número de parâmetros, existe o risco de sobreajuste aos dados históricos, o que pode levar a um desempenho insatisfatório em negociações ao vivo. A solução é realizar testes em múltiplos períodos de tempo e instrumentos, adotar configurações de parâmetros relativamente robustas e evitar otimização excessiva para dados históricos específicos.

-

Risco de Mudança nas Condições de Mercado: O desempenho da estratégia pode diferir entre mercados de tendência e mercados laterais; mudanças repentinas nas condições de mercado podem reduzir sua eficácia. A solução é introduzir um mecanismo de identificação do ambiente de mercado, ajustando parâmetros ou pausando negociações em diferentes estados do mercado.

-

Risco de Conflito de Sinais: O uso simultâneo de múltiplos indicadores pode gerar sinais contraditórios, causando confusão nas decisões. A solução é definir pesos razoáveis para cada indicador, enfatizando os mais confiáveis, e garantir que os limites dos sinais sejam definidos adequadamente para reduzir a probabilidade de conflitos.

-

Risco de Gerenciamento Inadequado de Capital: Embora a estratégia inclua mecanismos de stop loss, um gerenciamento inadequado de capital ainda pode levar ao esgotamento rápido dos fundos. A solução é controlar rigorosamente a proporção de capital alocado por negociação, garantindo que o risco máximo por operação esteja dentro de limites aceitáveis.

-

Risco de Falha Técnica: Sistemas de negociação automatizados podem enfrentar problemas técnicos como interrupção de rede ou atraso de dados. A solução é configurar mecanismos de intervenção manual, monitorar regularmente o estado operacional do sistema e lidar prontamente com anomalias.

Direções de Otimização da Estratégia

-

Adicionar Filtro de Ambiente de Mercado: Desenvolver um indicador que identifique se o mercado atual é de tendência ou lateral, ajustando dinamicamente os pesos das subestratégias de acordo com o estado do mercado, fortalecendo as estratégias de acompanhamento de tendência em mercados de tendência e as estratégias oscilantes em mercados laterais.

-

Introduzir Otimização por Machine Learning: Utilizar técnicas de aprendizado de máquina para ajustar automaticamente os parâmetros e pesos de cada indicador, permitindo que a estratégia aprenda e se adapte continuamente aos dados de mercado mais recentes, melhorando sua capacidade de adaptação dinâmica.

-

Aumentar a Análise de Volume de Negociação: Incorporar mudanças no volume de negociação como um sinal de confirmação adicional, executando negociações apenas com o suporte de volume esperado, aumentando a credibilidade dos sinais.

-

Otimizar o Algoritmo de Identificação de Topos e Fundos Potenciais: Aprimorar a lógica atual de identificação de topos e fundos, adicionando mais fatores de confirmação, como padrões de preço e confirmação em múltiplos períodos, melhorando a precisão da identificação.

-

Adicionar Indicadores de Sentimento: Integrar indicadores de sentimento do mercado, como o índice de medo (VIX) e a relação de opções de compra/venda, ajustando a estratégia ou pausando negociações em momentos de sentimento extremo para evitar negociações excessivas em períodos de alta volatilidade.

-

Desenvolver Mecanismo de Take Profit/Stop Loss Dinâmico: Ajustar automaticamente os níveis de take profit e stop loss com base na volatilidade do mercado, ampliando as faixas de stop loss em mercados de alta volatilidade e reduzindo-as em mercados de baixa volatilidade, tornando o gerenciamento de risco mais flexível e eficaz.

-

Otimização de Períodos de Tempo: Adicionar funcionalidade de análise em múltiplos períodos de tempo, exigindo que períodos de tempo superiores e inferiores confirmem sinais simultaneamente para reduzir falsos rompimentos e sinais falsos.

Resumo

A Estratégia de Negociação Inteligente com Múltiplos Indicadores Ponderados constrói um sistema de negociação abrangente e flexível ao integrar várias ferramentas de análise técnica e atribuir pesos diferentes a elas. A estratégia não apenas possui confirmação múltipla de sinais, sistema de pesos adaptável e gerenciamento de risco completo, mas também inclui um mecanismo automático de identificação de topos e fundos potenciais, demonstrando forte adaptabilidade em mercados complexos e voláteis.

Embora existam riscos potenciais como sobreajuste de parâmetros, mudanças nas condições de mercado e conflitos de sinais, eles podem ser controlados efetivamente por meio de configurações razoáveis de parâmetros, identificação do ambiente de mercado e gerenciamento rigoroso de capital. As direções futuras de otimização incluem a adição de filtros de ambiente de mercado, introdução de técnicas de machine learning, fortalecimento da análise de volume de negociação e otimização do algoritmo de identificação de topos e fundos potenciais; essas melhorias aumentarão ainda mais a estabilidade e a lucratividade da estratégia.

Para investidores que buscam métodos de negociação sistemáticos, essa estratégia de negociação inteligente com múltiplos indicadores ponderados oferece um quadro digno de consideração. Ela não apenas reduz a influência de fatores emocionais nas decisões de negociação, mas também otimiza continuamente o desempenho de negociação de forma orientada por dados. Ao implementar esta estratégia, recomenda-se começar com configurações de parâmetros conservadoras, ajustar gradualmente e monitorar de perto o desempenho da estratégia para encontrar a configuração mais adequada à tolerância pessoal ao risco e às condições de mercado.

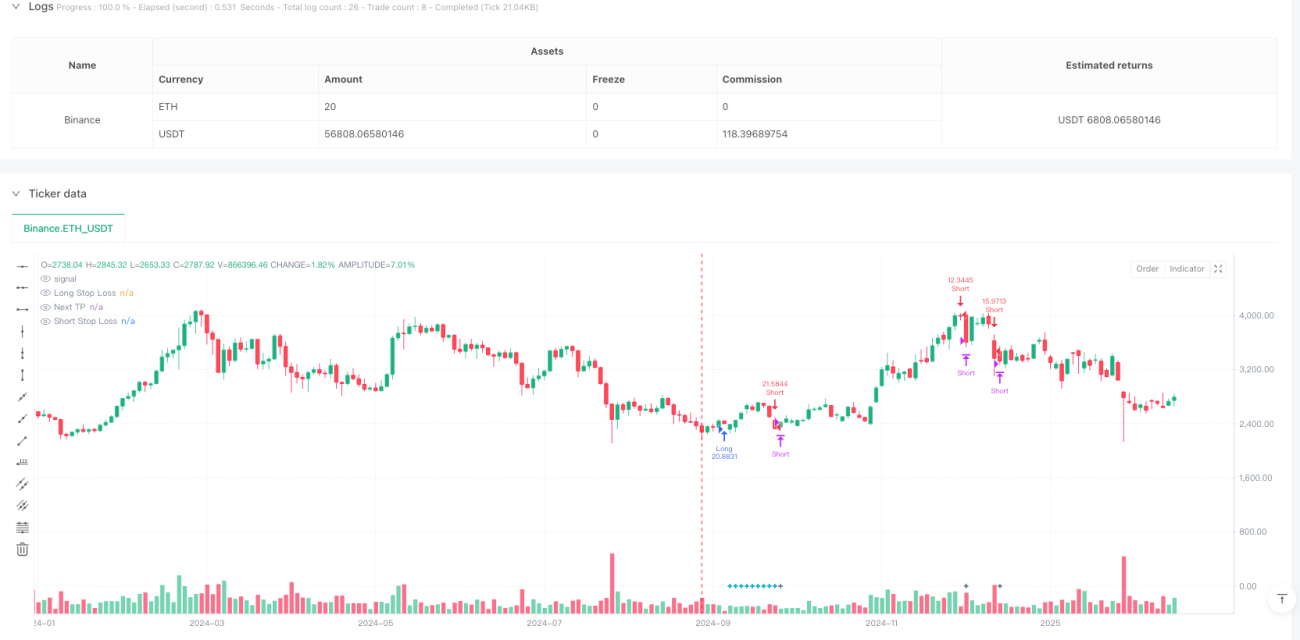

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1