Visão Geral

Esta é uma estratégia de trading quantitativo baseada na combinação de indicadores técnicos em múltiplas escalas de tempo. Através da análise integrada de médias móveis, Índice de Força Relativa Estocástico (SRI) e momentum de preço, busca-se uma entrada precisa no mercado e controle de risco. A estratégia visa capturar tendências de mercado enquanto gerencia efetivamente os riscos de trading, sendo adequada para traders quantitativos que buscam retornos estáveis.

Princípio da Estratégia

O núcleo da estratégia consiste em cinco indicadores técnicos principais:

-

Indicadores de Média Móvel:

- Médias Móveis Simples (SMA) de 5, 10, 50 e 100 períodos

- Determinação da direção da tendência do mercado através da posição relativa das médias móveis em múltiplas escalas de tempo

- Sinal de entrada baseado na relação entre o preço e as médias móveis

-

Índice de Força Relativa Estocástico (SRI):

- Cálculo do SRI utilizando escala de tempo de 1 minuto

- SRI abaixo de 70 como sinal de compra (long)

- SRI acima de 30 como sinal de venda (short)

-

Padrões de Candlestick:

- Análise da relação entre o preço de abertura e o fechamento do candle anterior

- Determinação do momentum atual de preço e sentimento do mercado

-

Mecanismo de Gerenciamento de Risco:

- Definição de pontos de Take Profit (TP) e Stop Loss (SL)

- Implementação de estratégia de Break-Even (BE)

- Ajuste dinâmico da posição de Stop Loss

Vantagens da Estratégia

-

Validação Multidimensional de Sinais

- Uso combinado de médias móveis, SRI e momentum de preço

- Redução significativa da probabilidade de sinais falsos

- Aumento da confiabilidade dos sinais de trading

-

Controle de Risco Flexível

- Pontos de Take Profit e Stop Loss predefinidos

- Mecanismo dinâmico de Break-Even

- Controle efetivo da perda máxima por negociação individual

-

Análise em Múltiplas Escalas de Tempo

- Combinação de médias móveis de diferentes períodos

- Captura abrangente das tendências de mercado

- Melhoria da adaptabilidade da estratégia

-

Ajustabilidade de Parâmetros

- Personalização dos pontos de Take Profit e Stop Loss

- Adaptação a diferentes ambientes de mercado e instrumentos negociados

Riscos da Estratégia

-

Risco de Sensibilidade a Parâmetros

- Os parâmetros de médias móveis e SRI impactam significativamente o desempenho da estratégia

- Necessidade de backtesting e otimização de parâmetros adequados

-

Risco de Volatilidade Extrema do Mercado

- A estratégia pode falhar em condições extremas de mercado

- Recomenda-se definir um limite máximo de drawdown

-

Risco de Excesso de Negociações

- Negociações frequentes podem aumentar os custos de trading

- Necessidade de ajuste considerando os custos reais de transação

-

Risco de Atraso dos Indicadores

- As médias móveis possuem certo atraso inerente

- Pode perder sinais de tendência em estágio inicial

Direções de Otimização da Estratégia

-

Introdução de Algoritmos de Aprendizado de Máquina

- Uso de algoritmos de aprendizado supervisionado para otimizar parâmetros

- Ajuste dinâmico dos pontos de Take Profit e Stop Loss

- Melhoria da capacidade adaptativa da estratégia

-

Adição de Filtros Suplementares

- Introdução de indicadores de volume

- Inclusão de indicadores de força de tendência

- Aumento da precisão dos sinais

-

Otimização para Adaptação a Múltiplos Ativos

- Desenvolvimento de mecanismo adaptativo de parâmetros genéricos

- Redução da intervenção manual

- Melhoria da universalidade da estratégia

Conclusão

Esta é uma estratégia de trading quantitativo baseada em análise de múltiplas escalas de tempo. Através da combinação de indicadores técnicos e mecanismos avançados de gerenciamento de risco, visa capturar tendências de mercado e controlar riscos de trading. A principal vantagem da estratégia reside na validação multidimensional dos sinais e no controle flexível de risco. Futuramente, através de aprendizado de máquina e combinações mais complexas de indicadores técnicos, busca-se aumentar ainda mais a estabilidade e a taxa de retorno da estratégia.

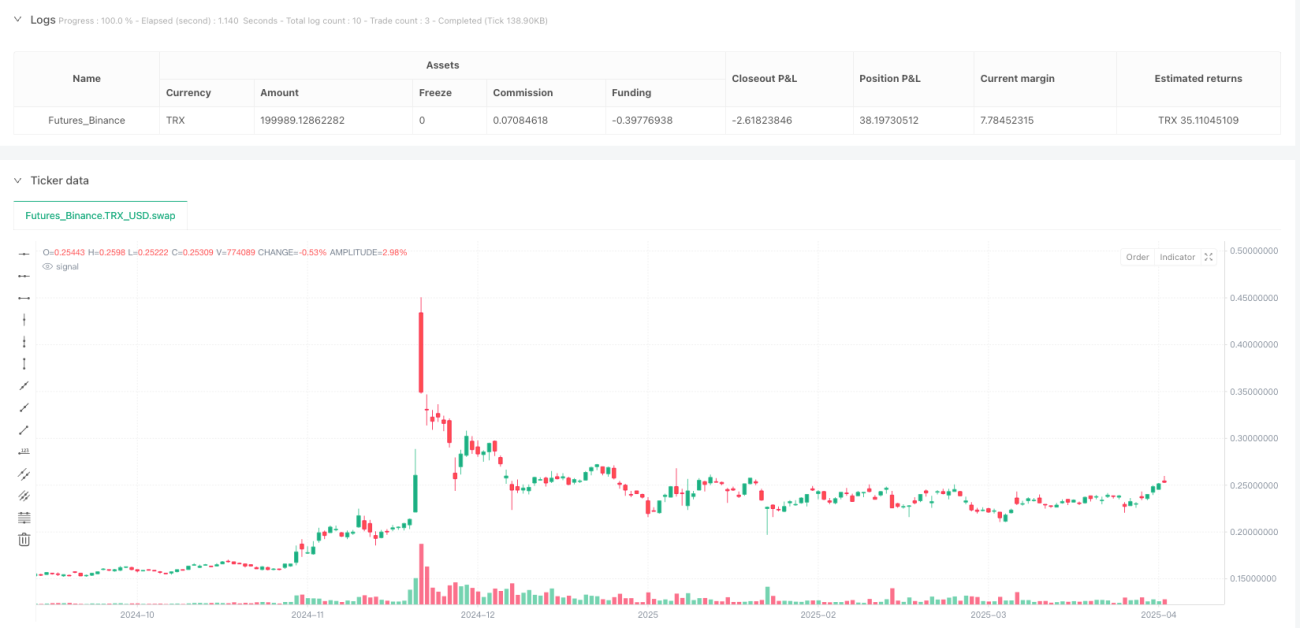

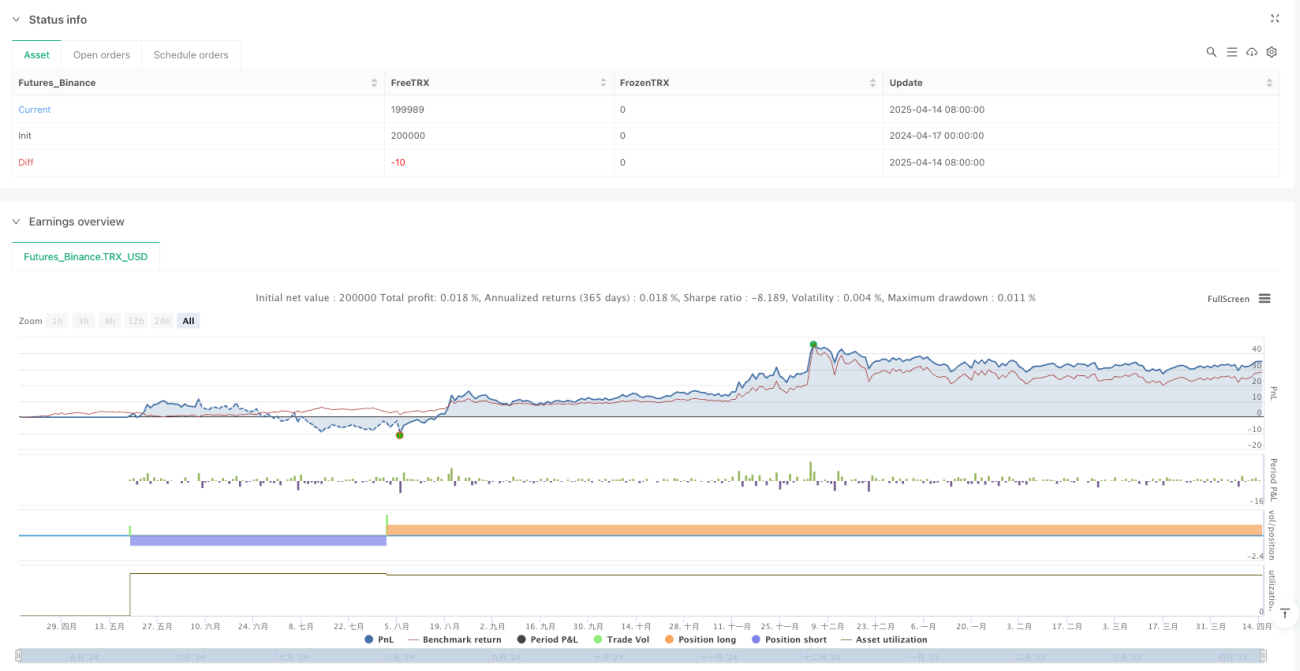

/*backtest

start: 2024-04-17 00:00:00

end: 2025-04-15 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"TRX_USD"}]

*/

//@version=6

strategy("Strategia LONG & SHORT con TP, SL e BE", overlay=true, default_qty_type=strategy.fixed, default_qty_value=1)

// === INPUT === //- 1