Estratégia de Rompimento/Reversão Ponderada por Volume Baseada em Pontos de Pivô

Visão Geral

Esta estratégia combina quebra/reversão de suporte/resistência (S/R), filtro de volume e um sistema de alerta, visando capturar pontos de inflexão críticos no mercado. A estratégia identifica sinais de quebra ou reversão de preço e os confirma com volume anormal, aumentando a confiabilidade dos sinais de negociação. A gestão de risco é feita com um stop loss fixo de 2% e uma relação de take profit ajustável (padrão de 3%).

Princípio da Estratégia

- Identificação de Suporte/Resistência: Utiliza as funções

ta.pivothigh()eta.pivotlow()para identificar níveis de preço chave em um período especificado (pivotLen). O sinal é gerado quando o preço rompe a resistência (alta de 1%) ou se recupera do suporte (após testar e fechar acima). - Filtro de Volume: Calcula a SMA do volume (período volSmaLength). Quando o volume atual excede o volMultiplier multiplicado pela SMA (padrão 1,5x), é considerada uma confirmação válida.

- Lógica de Compra e Venda:

- Condição de Compra: Preço rompe a zona de resistência (close > resZone*1,01) com volume elevado, ou o preço se aproxima da zona de suporte (dentro de ±1%) e ocorre um "falso rompimento para baixo" (low ≤ supZone, mas o fechamento se recupera) com volume aumentado.

- Condição de Venda: Preço rompe a zona de suporte (close < supZone*0,99) com volume elevado, ou o preço se aproxima da zona de resistência (dentro de ±1%) e ocorre um "falso rompimento para cima" (high ≥ resZone, mas o fechamento recua) com volume aumentado.

- Gestão de Risco: Stop loss fixo de 2% e take profit ajustável (padrão 3%) implementados por meio de

strategy.exit().

Análise de Vantagens

- Validação Multi-fatorial: Combina estrutura de preços (S/R), volume e comportamento de mercado (falso rompimento), reduzindo significativamente a probabilidade de sinais falsos.

- Adaptabilidade Dinâmica: Atualiza automaticamente os níveis de suporte e resistência, acompanhando as mudanças do mercado.

- Controle de Risco Rigoroso: Stop loss fixo evita perdas excessivas em uma única operação, e a relação de take profit é ajustável para diferentes volatilidades do mercado.

- Visualização Clara: Desenha linhas de suporte/resistência em tempo real e marca os sinais de negociação de forma evidente.

- Integração de Alertas: Pode ser conectado a sistemas de negociação automatizados, adequado para diferentes cenários de trading.

Análise de Riscos

- Risco de Mercado Lateral: Em mercados sem tendência, podem ocorrer rompimentos falsos frequentes, gerando múltiplos stop losses. Solução: Adicionar um filtro de tendência, como ADX ou EMA.

- Sensibilidade a Parâmetros: Os parâmetros pivotLen e volMultiplier precisam ser ajustados conforme o mercado. Solução: Realizar otimização de parâmetros e testes walk-forward.

- Atraso do Volume: O volume anormal pode aparecer após o movimento de preço. Solução: Incorporar dados de book de ofertas ou reduzir o volSmaLength.

- Risco de GAP: Gaps de abertura podem pular o stop loss. Solução: Usar ordens limite ou evitar períodos de alta volatilidade.

Direções de Otimização

- Filtro de Tendência: Adicionar condição ADX>25 ou direção da EMA200 para evitar negociações contra a tendência.

- Parâmetros Dinâmicos: Ajustar automaticamente pivotLen e volMultiplier com base na volatilidade do mercado (ex.: ATR).

- Take Profit em Etapas: Configurar dois níveis de take profit (ex.: 2% para fechar metade da posição e trailing stop para o restante), melhorando a relação risco-retorno.

- Otimização com Machine Learning: Treinar um modelo com dados históricos para otimizar os parâmetros volMultiplier e tpPerc.

- Confirmação de Múltiplos Períodos: Introduzir a confirmação de S/R em timeframes maiores para aumentar a qualidade dos sinais.

Resumo

Esta estratégia cria um framework de negociação de alta probabilidade por meio de tripla validação (posição de preço, volume e ação de preço), sendo especialmente adequada para capturar o início de tendências. Sua principal vantagem está na lógica transparente e no risco controlado, mas é necessário estar atento às suas limitações em mercados laterais. Otimizações futuras podem focar na adaptação de parâmetros e filtros de tendência para aumentar ainda mais a estabilidade.

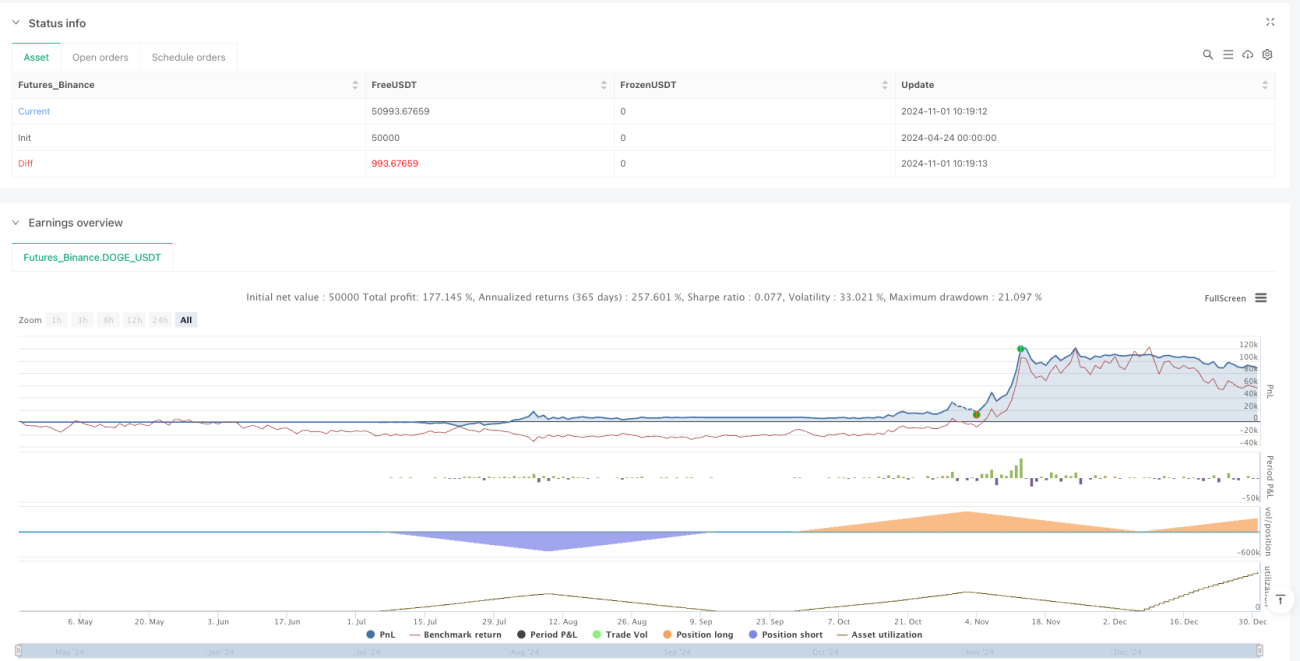

/*backtest

start: 2024-04-24 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=5

strategy("S/R Breakout/Reversal + Volume + Alerts", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===- 1