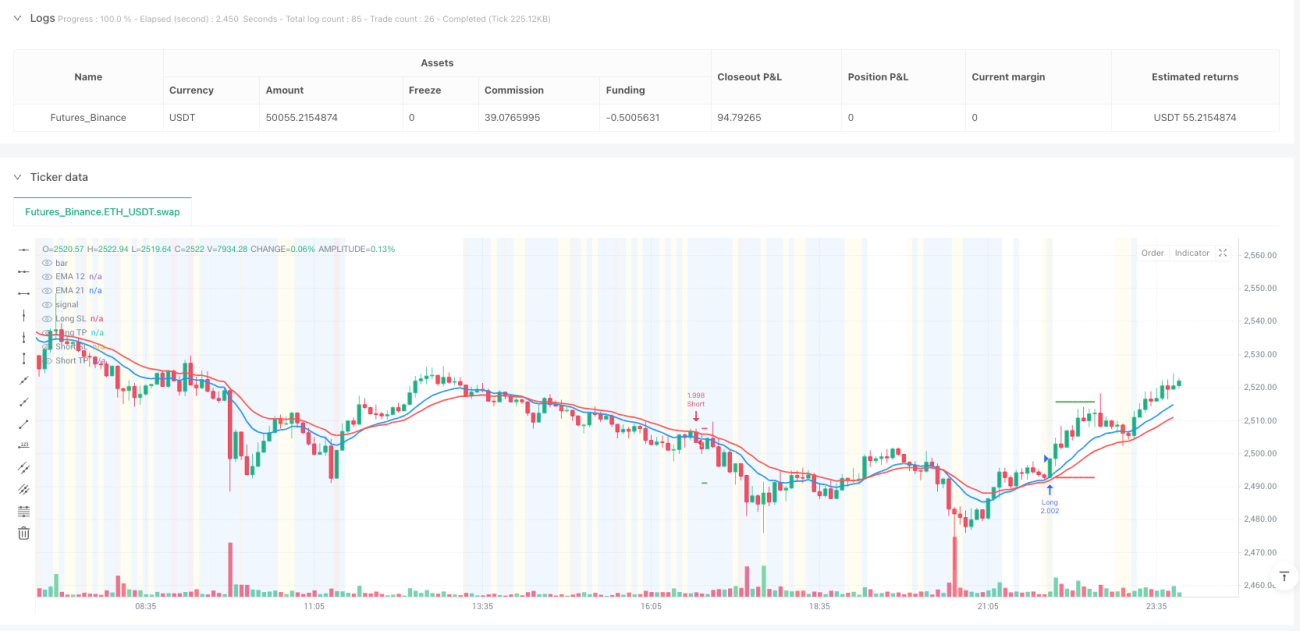

Visão Geral

Esta estratégia utiliza as bandas formadas por duas médias móveis exponenciais (EMA) para identificar oportunidades de reversão de alta probabilidade. Não se trata de uma simples estratégia de cruzamento de médias, mas sim de identificar momentos em que o preço ricocheteia nas bandas EMA e gera um momentum forte. A estratégia usa as EMAs de 12 e 21 períodos para construir a zona de negociação, combinando padrões de candlestick, consistência de tendência e um sistema de gestão de risco preciso para capturar o momentum do mercado.

Princípio da Estratégia

O princípio central da estratégia é identificar sinais de entrada ao detectar ricochetes do preço nas bandas EMA. Ela usa as EMAs de 12 e 21 períodos para criar faixas de negociação superior e inferior, determinando a direção da tendência do mercado com base na posição relativa das EMAs.

Quando EMA12 > EMA21, o mercado está em um ambiente de alta (faixa verde), e buscamos oportunidades de compra (long). As condições para compra incluem: a sombra inferior do preço toca a banda EMA; formação de um candle de alta forte (corpo maior que a sombra inferior); sombra superior minimizada (menor que 2% do range do candle); fechamento acima de ambas as EMAs; o candle anterior não fechou abaixo da banda inferior; e consistência de tendência de alta por vários candles consecutivos.

Quando EMA12 < EMA21, o mercado está em um ambiente de baixa (faixa vermelha), e buscamos oportunidades de venda (short). As condições para venda incluem: a sombra superior do preço toca a banda EMA; formação de um candle de baixa forte (corpo maior que a sombra superior); sombra inferior minimizada (menor que 2% do range do candle); fechamento abaixo de ambas as EMAs; o candle anterior não fechou acima da banda superior; e consistência de tendência de baixa por vários candles consecutivos.

A estratégia incorpora um sistema de gestão de risco com relação risco/retorno fixa, padrão de 3:1. O stop loss é definido no topo/fundo do candle anterior, e o take profit é calculado automaticamente com base na relação risco/retorno.

Vantagens da Estratégia

A estratégia apresenta várias vantagens significativas:

- Potencial de Alta Taxa de Acerto: Ao capturar movimentos de momentum fortes após um ricochete na banda EMA, a estratégia identifica oportunidades de negociação com alta probabilidade de sucesso.

- Regras Claras de Entrada e Saída: A estratégia fornece condições de negociação claras, reduzindo a subjetividade e o impacto de decisões emocionais.

- Excelente Gestão de Risco: Utiliza uma relação risco/retorno fixa e definições automáticas de stop loss e take profit, garantindo que o risco de cada operação seja controlado.

- Vantagem de Seguir Tendência: A estratégia opera apenas na direção da tendência dominante, evitando os altos riscos de operar contra a tendência.

- Aplicável a Múltiplos Períodos: A estratégia pode ser executada eficazmente em vários períodos de tempo, oferecendo flexibilidade de negociação.

- Sistema de Alertas Abrangente: Inclui funcionalidades detalhadas de alerta de sinais de negociação, garantindo que nenhuma oportunidade seja perdida.

- Auxílio Visual: Através de mudanças na cor de fundo e dicas de etiquetas, exibe visualmente os sinais de negociação e o estado das condições.

Riscos da Estratégia

Apesar do bom design, a estratégia apresenta os seguintes riscos potenciais:

- Risco de Mercado Lateral (Range): Em mercados laterais ou sem tendência definida, as bandas EMA podem ficar estreitas, gerando sinais frequentes mas de baixa qualidade, resultando em stops consecutivos.

- Risco de Gap (Salto de Preço) em Eventos Extremos: Após notícias ou eventos importantes, o mercado pode abrir com gaps, tornando o stop loss ineficaz e causando perdas maiores que o esperado.

- Sobreajuste (Overfitting) de Parâmetros: A otimização excessiva dos parâmetros da estratégia pode levar ao ajuste de curvas (curve fitting), fazendo com que a estratégia tenha um desempenho fraco em negociações reais.

- Atraso na Identificação da Tendência: Sendo indicadores defasados, as EMAs podem reagir lentamente em pontos de virada de tendência, fazendo com que se perca o melhor ponto de entrada ou que a saída seja atrasada.

- Risco de Ativação do Stop Loss por Ruído: O ruído do mercado pode ativar o stop loss e, em seguida, o preço retornar na direção esperada, causando perdas desnecessárias.

As soluções incluem: pausar a negociação em mercados laterais; usar um filtro de volatilidade para evitar sinais de baixa qualidade; combinar com outros indicadores para confirmar a tendência; realizar backtests periódicos e otimizar parâmetros; considerar o uso de stop loss móvel (trailing stop).

Direções de Otimização da Estratégia

A estratégia pode ser otimizada nas seguintes direções:

- Gestão de Risco Dinâmica: Ajustar automaticamente a relação risco/retorno e o tamanho da posição com base na volatilidade do mercado, reduzindo a exposição ao risco em ambientes de alta volatilidade.

- Introdução de Filtros Avançados: Combinar com o indicador ATR (Average True Range) para filtrar sinais em períodos de baixa volatilidade; adicionar confirmação de volume para validar a eficácia do ricochete de preço.

- Análise Multitemporal: Integrar a direção da tendência de um período de tempo superior como condição de filtro extra, entrando apenas quando as tendências de múltiplos períodos estiverem alinhadas.

- Otimização com Machine Learning: Usar algoritmos de aprendizado de máquina para ajustar dinamicamente os parâmetros, adaptando-se a diferentes condições de mercado com a combinação ideal de parâmetros.

- Implementação de Trailing Stop: Após a operação atingir um certo nível de lucro, implementar um mecanismo de trailing stop para bloquear parte do lucro enquanto permite que a tendência continue.

- Estratégia de Realização Parcial de Lucros: Implementar uma estratégia de saída parcial, reduzindo gradualmente a posição em diferentes níveis de preço alvo para otimizar o desempenho geral de risco/retorno.

Essas direções de otimização podem melhorar a robustez, adaptabilidade e rentabilidade de longo prazo da estratégia.

Resumo

A Estratégia de Negociação de Momentum com Ricochete nas Bandas de Duas Médias Móveis Exponenciais é um sistema de negociação abrangente que combina análise técnica, reconhecimento de padrões de candlestick e gestão de risco rigorosa. Ela captura oportunidades de mercado com momentum explosivo ao identificar pontos de reversão de alta probabilidade onde o preço ricocheteia nas bandas EMA. O principal ponto forte da estratégia reside nas suas regras de negociação claras, na estrutura fixa de risco/retorno e na exigência de consistência de tendência, tornando-a adequada para vários ambientes de mercado e períodos de tempo.

Embora existam alguns riscos potenciais, ao implementar as medidas de otimização sugeridas, os traders podem melhorar ainda mais a robustez e a rentabilidade da estratégia. Esta estratégia é particularmente adequada para traders que buscam uma abordagem sistemática, disciplinada e com risco controlado, sejam eles investidores de curto prazo ou de médio/longo prazo.

/*backtest

start: 2025-05-26 00:00:00

end: 2025-06-02 00:00:00

period: 5m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced EMA Band Rejection Strategy", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input parameters- 1