Visão Geral

A estratégia de rastreamento de volatilidade dinâmica multiciclo é um sistema de negociação de curto prazo que combina o cruzamento de médias móveis exponenciais (EMA) rápidas/lentas com um filtro de Índice de Força Relativa (RSI). A estratégia foca em encontrar oportunidades de pullback dentro da tendência de curto prazo dominante, reduzindo o ruído das negociações por meio de múltiplos mecanismos de confirmação. Suas características principais incluem controle de risco baseado no Average True Range (ATR), stop loss adaptativo, ajuste de stop baseado em volume e três níveis de alvo de lucro parcial. Além disso, a estratégia utiliza uma verificação de RSI em um timeframe superior como mecanismo de saída antecipada, evitando permanecer em tendências desfavoráveis.

Princípio da Estratégia

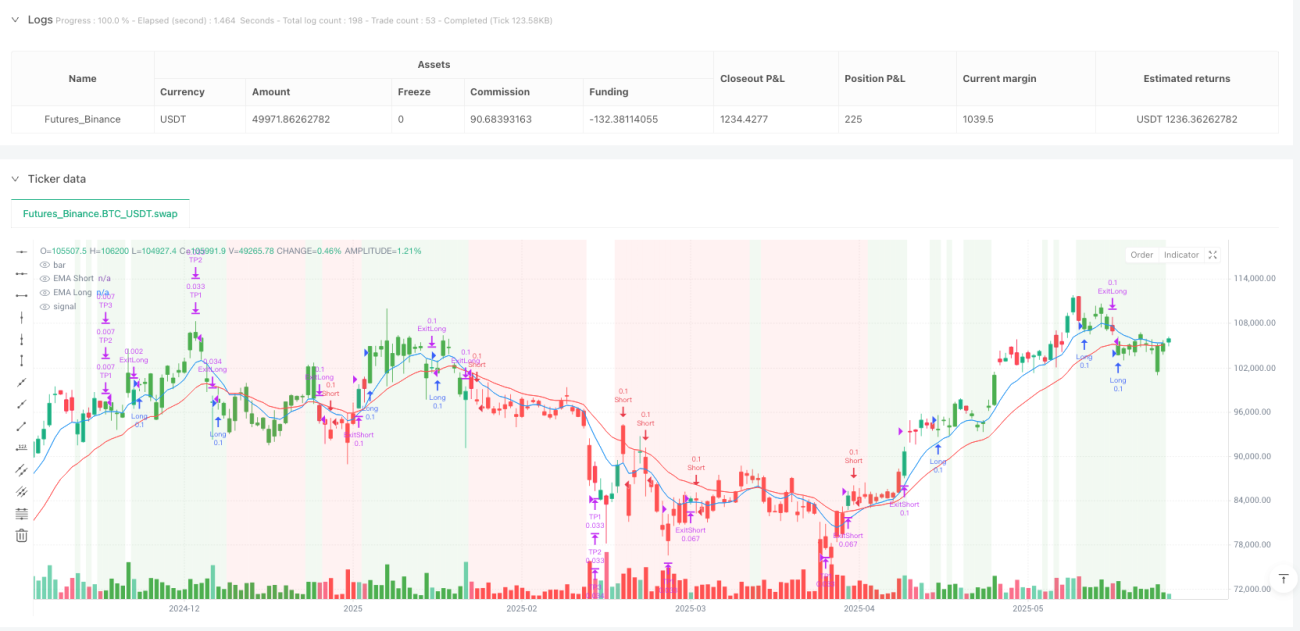

A estratégia opera com base em uma arquitetura de pilha de sinais em múltiplas camadas:

- Identificação de Tendência: Através do cruzamento entre EMA rápida e EMA lenta para determinar a direção micro da tendência. Quando a EMA rápida está acima da EMA lenta, identifica-se tendência de alta; caso contrário, tendência de baixa.

- Filtro de Saúde do Momentum: Evita perseguir movimentos excessivamente estendidos. Permite comprar apenas quando o RSI está abaixo do nível de sobrecompra; permite vender apenas quando o RSI está acima do nível de sobrevenda.

- Mecanismo de Confirmação por Candlestick: Exige que as condições do sinal sejam válidas por múltiplos candles consecutivos, filtrando efetivamente o ruído do mercado.

- Disparo de Entrada: Emite uma ordem a mercado quando o candle que completa a janela de confirmação aparece.

- Stop Loss Inicial: Ajustado pela volatilidade baseada no ATR e dinamicamente ajustado conforme o volume relativo.

- Lógica de Stop Loss Móvel: Combina pontos pivô e o stop loss baseado no ATR para otimizar o travamento de lucros.

- Monitoramento de RSI em Timeframe Superior: Fornece um sinal de saída de contexto de mercado, evitando negociar contra a tendência.

- Metas de Lucro Gradual: Define três níveis de alvo baseados no ATR para realizar reduções progressivas da posição.

- Limitador de Negociações: Restringe o número máximo de negociações por fase de tendência, evitando overtrading.

A inovação chave da estratégia é a integração orgânica de múltiplos indicadores técnicos com indicadores de comportamento de mercado (como volume e volatilidade), formando um sistema de negociação adaptativo que ajusta automaticamente os parâmetros em diferentes condições de mercado.

Vantagens da Estratégia

- Alta Adaptabilidade: Através do stop e metas ajustados pelo ATR, a estratégia se adapta a diferentes condições de volatilidade do mercado, sem necessidade de reotimização frequente dos parâmetros.

- Gestão de Risco Multicamadas: Combina stop loss inicial, stop móvel, lucro parcial e filtro RSI em múltiplos períodos, formando um sistema completo de controle de risco.

- Mecanismo de Filtragem de Ruído: A exigência de confirmação por múltiplos candles consecutivos reduz efetivamente sinais falsos, melhorando a qualidade das negociações.

- Sensibilidade à Liquidez: Ajusta o nível do stop loss através da proporção de volume, apertando automaticamente a exposição ao risco em ambientes de baixa liquidez.

- Monitoramento da Maturidade da Tendência: À medida que a tendência se desenvolve, reduz automaticamente o número de negociações permitidas, evitando excessos no final da tendência.

- Mecanismo Flexível de Lucro: A estratégia de lucro parcial em três níveis permite travar parte dos lucros enquanto mantém potencial de alta quando o movimento é favorável.

- Análise Interciclos: O monitoramento do RSI em timeframe superior fornece uma perspectiva mais ampla do contexto de mercado, evitando insistir em sinais micro durante reversões de tendência importantes.

- Facilidade de Execução: Através da integração com o PineConnector, é possível automatizar facilmente a estratégia, reduzindo a interferência humana e o impacto emocional.

Riscos da Estratégia

- Risco de Drawdown: Apesar das múltiplas camadas de controle de risco, em condições extremas de mercado (como gaps ou flash crashes), a estratégia pode enfrentar drawdowns acima do esperado. A mitigação envolve reduzir o tamanho da posição ou aumentar o múltiplo do ATR.

- Sensibilidade a Parâmetros: Alguns parâmetros chave, como comprimento da EMA e limiares do RSI, têm impacto significativo no desempenho da estratégia. Otimização excessiva pode levar a overfitting. Recomenda-se usar testes forward progressivos, em vez de otimização in-sample.

- Custos de Negociação de Alta Frequência: Como estratégia de curto prazo, a frequência de negociação é alta, e os custos acumulados (spread, comissões) podem impactar significativamente os lucros reais. Os custos reais de negociação devem ser considerados nos backtests.

- Risco de Latência: A latência de execução do PineConnector (cerca de 100-300 ms) pode aumentar o slippage em mercados de alta volatilidade. Não é recomendado para mercados extremamente voláteis ou com baixa liquidez.

- Redesenho de Pontos Pivô: Em gráficos de timeframe muito curto (abaixo de minutos), os pontos pivô podem ser redesenhados durante a formação do candle em tempo real, afetando a precisão do stop.

- Atraso na Identificação de Tendência: A identificação de tendência baseada no cruzamento de EMAs possui atraso inerente, podendo perder parte do movimento no início da tendência.

- Risco de Alavancagem Excessiva: Se o multiplicador de posição for muito grande, uma única negociação pode expor a um risco muito alto, esgotando rapidamente o capital da conta.

Direções de Otimização da Estratégia

- Otimização por Machine Learning: Introduzir algoritmos de aprendizado de máquina para ajustar dinamicamente os parâmetros da EMA e do RSI, adaptando-se a diferentes condições de mercado. Isso resolve o problema de adaptabilidade insuficiente de parâmetros fixos em diferentes fases do mercado.

- Classificação do Estado do Mercado: Adicionar análise de cluster de volatilidade para classificar o mercado em estados de alta, média e baixa volatilidade, utilizando parâmetros diferenciados para cada estado. Isso melhora a adaptabilidade em mercados em transição.

- Mecanismo de Consenso de Múltiplos Indicadores: Integrar outros indicadores de momentum e tendência (como MACD, Bandas de Bollinger, KDJ) para formar um sistema de consenso, gerando sinais apenas quando a maioria dos indicadores concorda. Isso reduz sinais falsos.

- Filtro Inteligente de Horário: Incluir análise de horários de mercado e padrões de volatilidade, evitando períodos ineficientes e eventos de alta volatilidade conhecidos (como divulgação de dados econômicos importantes).

- Proporção Dinâmica de Lucro Parcial: Ajustar automaticamente a porcentagem de lucro parcial e a distância do alvo com base na volatilidade e na força da tendência, retendo mais posição em tendências fortes e realizando lucros mais agressivamente em tendências fracas.

- Reforço do Controle de Drawdown: Introduzir um mecanismo de risco adaptativo baseado em padrões históricos de drawdown, reduzindo automaticamente a frequência de negociação ou aumentando a distância do stop quando são detectados precursores de grandes drawdowns semelhantes aos históricos.

- Aprimoramento com Dados de Alta Frequência: Quando possível, integrar dados de tick para otimizar a entrada, reduzindo slippage e melhorando o preço de entrada.

- Análise de Correlação entre Mercados: Adicionar análise de correlação com mercados relacionados, utilizando relações de liderança-arrasto entre mercados para melhorar a qualidade dos sinais.

Resumo

A estratégia de rastreamento de volatilidade dinâmica multiciclo é um sistema de negociação de curto prazo que combina ferramentas clássicas de análise técnica com métodos modernos de gestão de risco quantitativa. Através de uma arquitetura de pilha de sinais em múltiplas camadas, combinando identificação de tendência por EMA, filtro de momentum por RSI, mecanismo de confirmação por múltiplos candles consecutivos, ajuste de volatilidade por ATR e análise multiciclo, ela constrói um framework abrangente de tomada de decisão. A característica mais marcante da estratégia é sua adaptabilidade — ela ajusta automaticamente parâmetros e medidas de controle de risco com base na volatilidade, volume e maturidade da tendência.

Embora existam riscos inerentes, como sensibilidade a parâmetros, custos de negociação de alta frequência e riscos de latência, eles podem ser controlados através de gestão de capital adequada e otimização contínua. As direções futuras de otimização concentram-se principalmente em otimização de parâmetros por machine learning, classificação de estado do mercado, mecanismo de consenso de múltiplos indicadores e gestão de risco dinâmica.

Para traders que desejam capturar oportunidades de pullback dentro de tendências de curto prazo, esta estratégia oferece um framework estruturado que equilibra a captura de oportunidades de negociação com o controle de risco. No entanto, como toda estratégia de negociação, deve ser testada exaustivamente em conta demo antes da aplicação real, com ajustes de parâmetros conforme a tolerância pessoal ao risco e o tamanho do capital.

- 1