Estratégia de Trend Following com Cruzamento de Médias Móveis Duplas e Sistema Avançado de Gerenciamento de Risco

Visão Geral da Estratégia

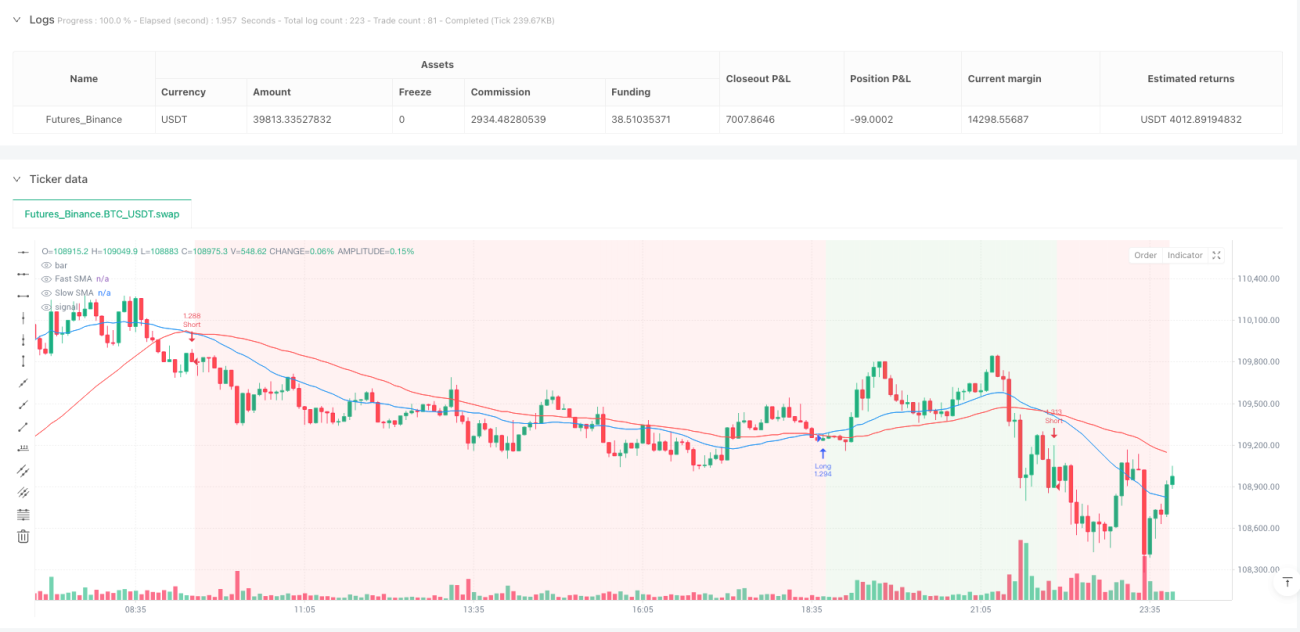

A estratégia de rastreamento de tendência com cruzamento de médias móveis duplas é um sistema de negociação quantitativo que combina análise técnica com gestão de risco abrangente. O núcleo da estratégia utiliza sinais de cruzamento entre a Média Móvel Simples rápida (Fast SMA) e a Média Móvel Simples lenta (Slow SMA) para identificar mudanças na tendência do mercado, e garante a segurança do capital por meio de múltiplos mecanismos de controle de risco. A estratégia é implementada na plataforma Pine Script e é adequada para negociação de rastreamento de tendência em diversos instrumentos de negociação.

Princípio da Estratégia

A estratégia toma decisões de negociação com base na interação entre duas médias móveis simples:

-

Mecanismo de geração de sinais:

- Sinal de compra (long): Quando a SMA rápida (padrão 24 períodos) cruza acima da SMA lenta (padrão 48 períodos)

- Sinal de venda (short): Quando a SMA rápida cruza abaixo da SMA lenta

- Sinal de fechamento: Quando ocorre um sinal de cruzamento oposto

-

Controle de tempo de execução:

A estratégia executa todas as decisões de negociação no fechamento da vela, evitando viés de antecipação (look-ahead bias) e garantindo a confiabilidade e realismo dos resultados do backtest. -

Sistema de gestão de capital:

- Controle de risco por negociação: Por padrão, o risco máximo de cada negociação é limitado a 2,0% do capital total da conta

- Cálculo automático do tamanho da posição: Ajustado dinamicamente com base na distância do stop loss e no valor de risco, garantindo que o limite de risco predefinido não seja excedido

-

Controle de risco em múltiplos níveis:

- Stop Loss fixo: Stop loss percentual fixo (padrão 0,8%) definido imediatamente após a entrada, limitando a perda por operação

- Take Profit: Calculado automaticamente com base na relação risco-retorno (padrão 2,0), por exemplo, stop loss de 0,8% combinado com relação risco-retorno de 2,0 resulta em um take profit de 1,6%

- Trailing Stop Loss avançado:

- Condição de ativação: Começa a ser ativado quando o lucro atinge uma porcentagem predefinida (padrão 1,0%)

- Mecanismo de rastreamento: Uma vez ativado, o preço do stop loss rastreia o preço máximo (para posições compradas) ou o preço mínimo (para posições vendidas), mantendo uma distância especificada (padrão 0,5%)

- Garantia de segurança: Garante que o trailing stop nunca fique abaixo do nível de stop loss inicial, protegendo o capital enquanto permite que os lucros continuem a crescer

Esta estratégia captura tendências através do cruzamento de médias móveis e utiliza medidas abrangentes de gerenciamento de risco para garantir a segurança e sustentabilidade das negociações.

Vantagens da Estratégia

-

Mecanismo robusto de identificação de tendências:

- O sistema de cruzamento de médias móveis duplas é um indicador clássico de rastreamento de tendências, com eficácia e estabilidade historicamente comprovadas

- Ajustando os períodos das médias móveis rápida e lenta, pode-se adaptar às características de tendência de diferentes ambientes de mercado e períodos de tempo

-

Gestão precisa de capital:

- Alocação dinâmica de risco com base no patrimônio líquido da conta, garantindo que o risco de cada negociação permaneça sempre dentro de limites controláveis

- O tamanho da posição é ajustado automaticamente com base na distância real do stop loss, evitando problemas de alavancagem excessiva ou posições muito pequenas

- O sistema possui mecanismos de verificação de segurança integrados para evitar erros de cálculo em condições extremas

-

Proteção de risco em múltiplas camadas:

- Stop loss fixo fornece proteção básica, limitando a perda máxima

- Configuração de take profit baseada na relação risco-retorno garante que o lucro médio exceda a perda média

- Mecanismo avançado de trailing stop protege os lucros já realizados sem afetar o potencial de ganhos com a continuação da tendência

-

Controle temporal da execução das negociações:

- Todas as decisões de negociação são executadas estritamente com base no preço de fechamento da vela, evitando viés de antecipação

- Uso do parâmetro

process_orders_on_close=truepara garantir que o processamento das ordens reflita um ambiente de negociação real - A lógica de negociação é baseada em sinais da vela anterior, evitando o uso de dados futuros

-

Sistema de trailing stop adaptativo:

- O trailing stop só é ativado após a negociação atingir um nível de lucro predefinido, evitando ativação prematura

- O nível de stop loss é ajustado automaticamente conforme o preço se move, travando parte do lucro enquanto permite que a tendência continue a se desenvolver

- Mecanismo de proteção integrado garante que o trailing stop não caia abaixo do nível de stop loss inicial, fornecendo proteção contínua contra riscos

Riscos da Estratégia

-

Atraso na identificação de tendências:

- As médias móveis são inerentemente indicadores defasados, podendo reagir com atraso em pontos de inflexão da tendência

- Em mercados laterais, podem gerar sinais falsos frequentes, causando o efeito "serrote" (Whipsaw)

- Mitigação: Considere adicionar condições de filtro adicionais, como indicadores de volatilidade ou confirmação de força da tendência

-

Problemas de adaptação com parâmetros fixos:

- A eficácia dos períodos padrão da SMA (24 e 48) pode variar em diferentes mercados e períodos de tempo

- A configuração de porcentagens fixas para stop loss e take profit pode não ser adequada para todos os ambientes de volatilidade

- Mitigação: Recomenda-se ajustar os parâmetros com base nas características específicas do instrumento de negociação e na volatilidade histórica, ou introduzir mecanismos de parâmetros adaptativos

-

Momento de ativação do trailing stop:

- Se o nível de lucro para ativar o trailing stop (padrão 1,0%) for muito alto, pode perder a oportunidade de travar lucros

- Se for muito baixo, pode ser ativado prematuramente, limitando o lucro potencial

- Mitigação: Defina os parâmetros do trailing stop com base na proporção do Average True Range (ATR) do instrumento alvo, tornando-o mais adaptativo

-

Risco de gestão de capital:

- Para instrumentos com volatilidade muito baixa, um stop loss percentual fixo pode resultar em posições excessivamente grandes

- Em condições extremas de mercado (como gaps ou flash crashes), a execução no preço de stop loss predefinido pode não ser possível

- Mitigação: Considere definir limites máximos de posição ou ajustar dinamicamente os parâmetros de risco com base em indicadores de volatilidade (como ATR)

-

Limitações de implementação técnica:

- A lógica alternativa quando o percentual de stop loss é zero ou negativo pode levar a riscos inesperados

- Não são considerados custos de transação e slippage no desempenho real da estratégia

- Mitigação: Aprimore o tratamento de erros, adicione mais verificações de segurança e inclua fatores de custo de negociação nos backtests

Direções de Otimização da Estratégia

-

Otimização do mecanismo de geração de sinais:

- Introduzir períodos de média móvel adaptativos: Ajustar dinamicamente os períodos das médias rápidas e lentas com base na volatilidade do mercado, melhorando a adaptabilidade a diferentes ambientes

- Adicionar indicadores auxiliares de confirmação: Combinar indicadores como Índice de Força Relativa (RSI), Estocástico ou MACD para filtrar sinais de baixa qualidade

- Considerar análise de estrutura de preços: Integrar fatores como suporte e resistência, reconhecimento de padrões de preços, para melhorar a qualidade dos sinais

-

Aprimoramento do sistema de gerenciamento de riscos:

- Stop loss adaptativo à volatilidade: Definir dinamicamente a distância do stop loss com base em indicadores de volatilidade como ATR, em vez de porcentagens fixas

- Estratégia de trailing stop em estágios: Implementar trailing stop em múltiplos níveis, apertando gradualmente a distância de rastreamento à medida que o lucro aumenta

- Controle de drawdown máximo: Adicionar um mecanismo de ajuste de risco baseado na proporção máxima de drawdown da conta, reduzindo automaticamente o risco em condições de mercado desfavoráveis

-

Otimização da entrada:

- Filtro de força da tendência: Executar sinais de negociação apenas quando a força da tendência atinge um determinado limiar

- Filtro de janela de volatilidade: Executar negociações em condições de volatilidade adequadas, evitando mercados excessivamente voláteis ou com baixa volatilidade

- Melhor preço de execução: Pesquisar o momento e nível de preço ótimos para entrada após a geração do sinal

-

Estrutura de backtest e avaliação:

- Consistência em múltiplos períodos de tempo: Verificar a consistência e robustez da estratégia em diferentes períodos de tempo

- Análise de sensibilidade: Testar exaustivamente o impacto de variações de parâmetros no desempenho da estratégia, encontrando a combinação mais estável

- Simulação de Monte Carlo: Avaliar a distribuição de probabilidade e robustez da estratégia através de resultados de negociação aleatorizados

-

Melhorias na implementação técnica:

- Aprimorar o tratamento de erros: Reforçar o tratamento de casos extremos, garantindo a operação estável da estratégia em vários ambientes de mercado

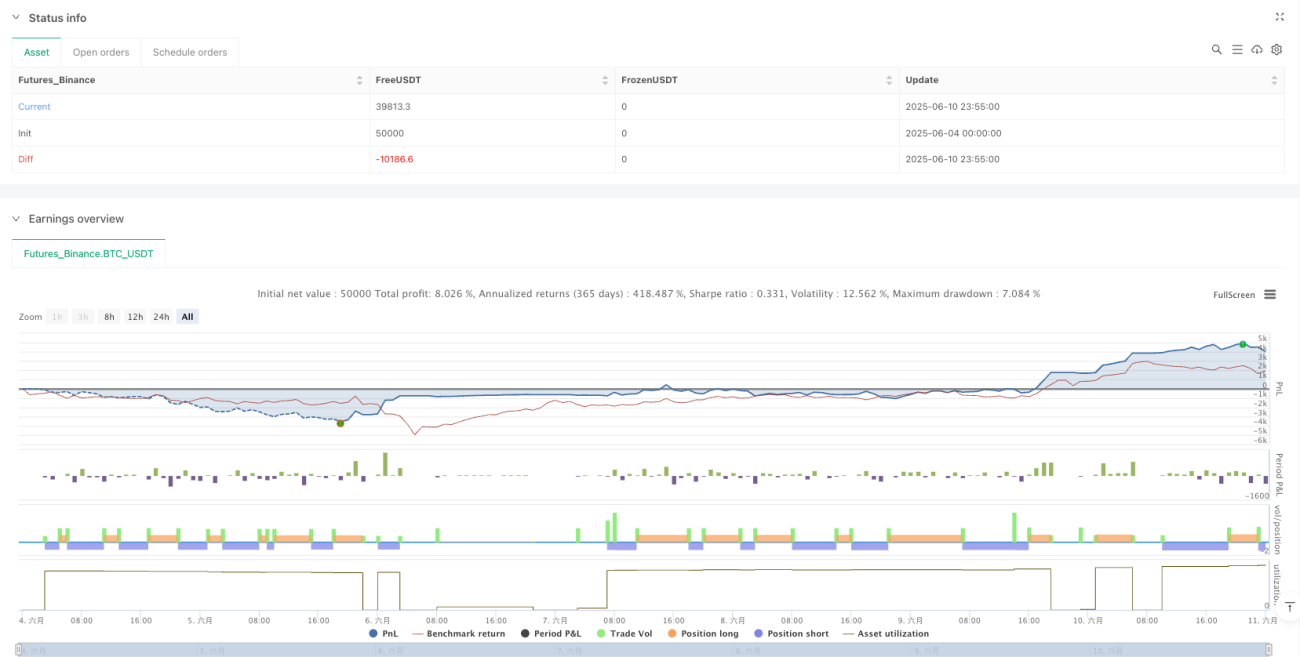

- Adicionar monitoramento de indicadores de desempenho: Acompanhar em tempo real indicadores-chave de desempenho, como Índice de Sharpe, drawdown máximo, etc.

- Visualização do estado da estratégia: Melhorar a interface gráfica para exibir intuitivamente o estado da estratégia, posições e níveis de risco

Resumo

A estratégia de rastreamento de tendência com cruzamento de médias móveis duplas é um sistema de negociação completo que combina métodos clássicos de análise técnica com conceitos modernos de gerenciamento de risco. Sua principal vantagem reside no mecanismo claro e simples de identificação de tendências combinado com um sistema de controle de risco em múltiplas camadas, especialmente sua gestão precisa de capital e mecanismo avançado de trailing stop, que oferecem um bom potencial de retorno ajustado ao risco.

No entanto, a estratégia também enfrenta desafios como o atraso inerente das médias móveis e a adaptabilidade dos parâmetros. Com a introdução de parâmetros adaptativos, a melhoria dos mecanismos de filtragem de sinais e o aperfeiçoamento do sistema de gerenciamento de risco, o desempenho da estratégia pode ser ainda mais aprimorado.

No geral, esta é uma estrutura de estratégia quantitativa bem estruturada e logicamente clara, adequada como base para sistemas de rastreamento de tendência de médio a longo prazo, especialmente em mercados com características de tendência pronunciadas. Para os traders, compreender e dominar seus conceitos de gerenciamento de risco é mais importante do que simplesmente copiar os parâmetros da estratégia — esta é a parte mais valiosa da estratégia.

- 1