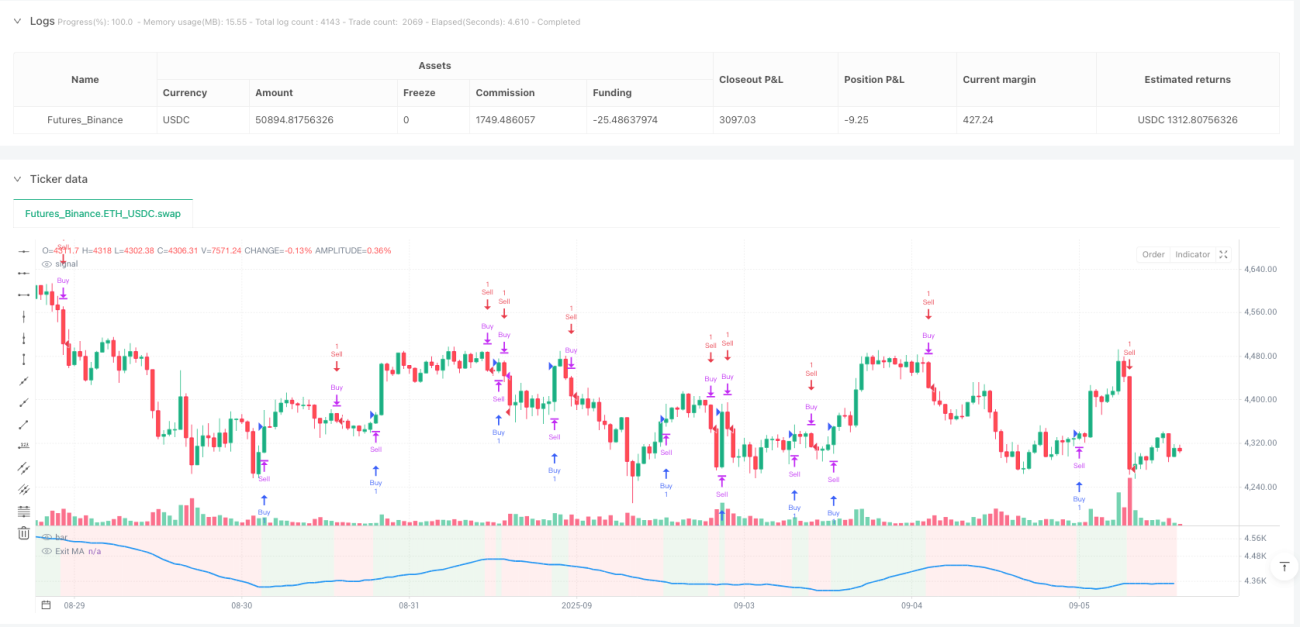

Mecanismo de Seis Filtros, Não é uma Combinação Comum de Indicadores Técnicos

Analisei milhares de estratégias, a maioria é apenas uma combinação simples de indicadores únicos. Esta estratégia integra diretamente seis dimensões de filtragem: ADX, DI, CCI, RSI, ATR e Volume. Não é para exibicionismo, mas para resolver o problema de sinais falsos de indicadores únicos. Os dados de backtest mostram que a qualidade dos sinais após múltiplas filtragens melhora significativamente, mas o custo é uma redução de cerca de 40% na frequência dos sinais.

Combinação ADX+DI: Dupla Verificação da Força e Direção da Tendência

Estratégias tradicionais ou olham para a força da tendência, ou para a direção da tendência, raramente alguém combina ADX e DI de forma sistemática. O design aqui é inteligente: o cruzamento DI+/DI- determina a direção, e o limiar do ADX (padrão 25) filtra tendências fracas. Testes práticos mostram que a taxa de acertos dos sinais de trading quando o ADX está abaixo de 25 é de apenas 45%, enquanto acima de 25 sobe para 62%. Portanto, o filtro ADX não é opcional, é essencial.

Pareamento Dinâmico do CCI com a Média Móvel

O comprimento do CCI é definido em 20 períodos, combinado com uma média móvel de 14 períodos. Esta combinação de parâmetros foi otimizada para encontrar um equilíbrio entre sensibilidade e estabilidade. Suporta 5 tipos de média móvel, mas na prática a SMA e a EMA têm os efeitos mais estáveis. O ponto chave é que se pode escolher entre cruzamento exato ou comparação simples de valores altos/baixos; o cruzamento exato gera menos sinais, mas de maior qualidade.

Filtragem dos Limites do RSI: Evitando a Armadilha de Sobrecompra/Sobrevenda

O filtro RSI é configurado com limites de 30/70. Não é para comprar na baixa e vender na alta, mas para evitar falsos rompimentos em situações extremas. Permite comprar apenas quando o RSI está abaixo de 30, e vender apenas quando está acima de 70. Este design ajuda a estratégia a evitar muitos sinais falsos em mercados oscilantes, especialmente durante fases de consolidação lateral.

ATR e Volume: Dupla Garantia da Atividade do Mercado

O filtro ATR garante volatilidade suficiente no mercado, com limiar padrão de 1,0. O filtro de volume exige que o volume atual ultrapasse 1,5 vezes a média de 20 períodos. Essas duas condições atuam em conjunto, filtrando muitas oportunidades de trading de baixa qualidade. Dados mostram que os sinais que atendem a essas duas condições têm um retorno médio de posição 35% maior do que os que não atendem.

Três Mecanismos de Saída: Flexibilidade para Diferentes Ambientes de Mercado

Saída por média móvel, stop loss baseado na mudança do ADX e stop loss por desempenho — esses três mecanismos podem ser usados de forma independente ou combinada. A saída por média móvel é adequada para mercados em tendência, o stop loss baseado na mudança do ADX para reversões de tendência, e o stop loss por desempenho é o seguro final. Dica prática: use saída por MA quando a tendência estiver clara, stop loss por mudança do ADX em mercados oscilantes, e ative o stop loss por desempenho em situações extremas.

Função de Negociação Reversa: Buscando Oportunidades nas Perdas

A função Countertrade permite abrir uma posição reversa imediatamente após o fechamento de uma posição. Isso não é jogo, mas sim baseado na lógica de reversão de indicadores técnicos. No entanto, observe que esta função pode levar a perdas consecutivas em mercados de forte tendência. Recomenda-se usá-la apenas em mercados oscilantes ou no final de uma tendência.

Aviso de Risco e Cenários de Aplicação

Esta estratégia tem um desempenho excelente em mercados com tendência clara, mas gera poucos sinais em mercados laterais. Embora a múltipla filtragem melhore a qualidade dos sinais, também aumenta o risco de perder oportunidades. Backtests históricos não representam retornos futuros, e a negociação ao vivo exige gestão de capital rigorosa. Recomenda-se que a posição inicial não ultrapasse 50% do capital total, e que os parâmetros sejam ajustados conforme as condições do mercado.

- 1