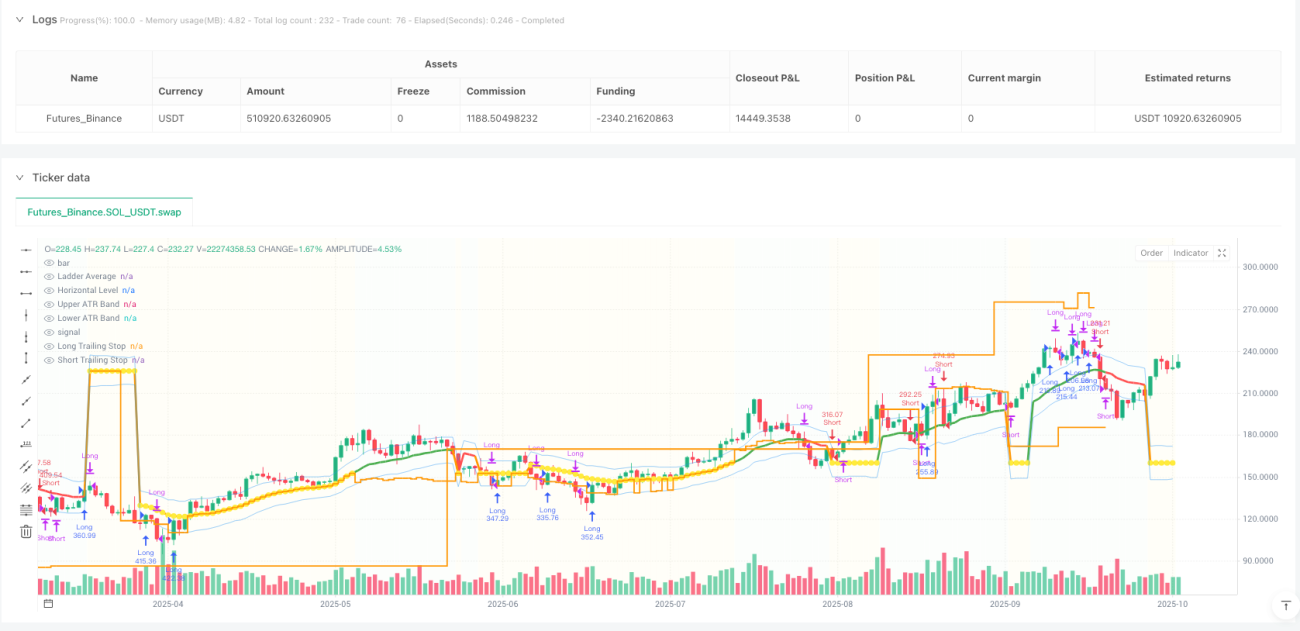

Estratégia de Média Escalonada de Tendência: Como "Relaxar" Elegantemente Quando o Mercado Está Lateral?

Por que as estratégias tradicionais de seguimento de tendência frequentemente "fracassam" em mercados laterais?

Como profissional de trading quantitativo, frequentemente me perguntam: por que estratégias que se saem bem em mercados de tendência começam a sofrer grandes drawdowns assim que o mercado entra em range?

A resposta é simples: a maioria das estratégias de seguimento de tendência sofre de "obsessão por tendência" — elas sempre tentam manter negociações de alta frequência em qualquer condição de mercado, ignorando um fato básico: 70% do tempo o mercado está em oscilação lateral.

A estratégia "Média de Degraus de Tendência" que analisaremos hoje justamente aborda esse ponto fraco com uma solução interessante: seguir ativamente em mercados de tendência, e "descansar elegantemente" em mercados laterais.

O que é "média de degraus"? Como esse conceito redefine o seguimento de tendência?

As estratégias tradicionais de média móvel têm uma falha fatal: elas estão sempre mudando. Quer o mercado esteja em forte tendência ou em oscilação lateral, a média se ajusta constantemente às flutuações de preço, gerando muitos sinais falsos.

A ideia central da "média de degraus" é: congelar a média móvel sob condições específicas.

A lógica de implementação é a seguinte:

-

Detecção do estado da tendência: Usar o indicador ADX para avaliar a força da tendência

- ADX > 25: Mercado de forte tendência

- Inclinação da média móvel < 0,3%: Mercado lateral

-

Troca dinâmica de média móvel:

- Em forte tendência: acompanhamento normal da EMA(21)

- Em mercado lateral: a média "congela" em posição horizontal, formando suporte/resistência

A engenhosidade desse design está em: fazer a estratégia exibir diferentes "personalidades" em diferentes ambientes de mercado — sensível em tendência, estável em oscilação.

Como implementar o sistema de "captura de tendência"?

Além do mecanismo básico de média de degraus, a estratégia integra um módulo de "captura de tendência", que considero a parte mais inovadora:

Mecanismo de reversão rápida:

- Quando uma forte tendência contrária aparece logo após o fechamento de uma posição

- Abrir rapidamente uma nova posição em até 3 períodos

- Condições: ADX > 30 e diferença entre DI+ e DI- > 10

Esse design resolve um problema importante das estratégias tradicionais: como ajustar rapidamente a posição no início de uma reversão de tendência.

Imagine o cenário: você acabou de fechar uma posição comprada devido ao stop loss, e o mercado imediatamente inicia uma forte tendência de queda. Estratégias tradicionais podem esperar por novos sinais de confirmação, mas esse sistema de "captura de tendência" consegue abrir uma posição vendida em até 3 períodos.

Gerenciamento de risco: por que distinguir os estados do mercado?

O aspecto mais digno de aprendizado desta estratégia é seu mecanismo diferenciado de gerenciamento de risco:

Controle de risco em mercado lateral:

- Ajustar o stop loss próximo à média de degraus

- Reduzir o múltiplo do ATR, apertando o stop

- Definir metas mais conservadoras

Controle de risco em mercado de tendência:

- Usar stop loss padrão baseado em múltiplo do ATR

- Ativar stop loss móvel em degraus

- Permitir maior espaço de flutuação de preço

Esse design reflete uma filosofia importante de trading: diferentes ambientes de mercado exigem diferentes apetites ao risco. Em mercados laterais, devemos ser mais cautelosos; em mercados de tendência, precisamos dar mais espaço para os lucros correrem.

Stop loss móvel em degraus: como equilibrar proteção de lucros e seguimento de tendência?

O stop loss móvel tradicional costuma ser muito mecânico: ou muito apertado, causando saída precoce, ou muito frouxo, não protegendo os lucros adequadamente. O stop loss móvel em degraus desta estratégia oferece uma solução mais inteligente:

Lógica de configuração dos degraus:

- Calcular dinamicamente o espaçamento dos degraus baseado no ATR

- Máximo de 5 níveis de degraus

- A cada vez que um degrau é rompido, o stop loss é ajustado para cima

A vantagem desse design é: ele consegue proteger os lucros enquanto dá espaço suficiente para a tendência se desenvolver.

O que observar na aplicação prática?

Com base na minha experiência operacional, ao usar esse tipo de estratégia, preste atenção aos seguintes pontos:

-

Armadilha da otimização de parâmetros: Não otimize excessivamente o limiar do ADX; valores entre 25-30 costumam ser estáveis na maioria dos mercados.

-

Adaptabilidade ao mercado: A estratégia é mais adequada para mercados com volatilidade moderada; em condições extremas, pode ser necessário ajustar o múltiplo do ATR.

-

Gerenciamento de capital: Recomenda-se que cada posição não exceda 10% do capital total, especialmente ao ativar a função de captura de tendência.

-

Armadilha de backtest: Prestar atenção especial ao impacto do slippage e das comissões, especialmente em negociações frequentes em mercados laterais.

Qual é o valor inovador desta estratégia?

Do ponto de vista do desenvolvimento de estratégias quantitativas, esta estratégia representa uma importante direção evolutiva: a transição de lógica única para adaptação multiestado.

Estratégias tradicionais muitas vezes tentam usar uma lógica fixa para lidar com todas as condições de mercado, enquanto esta estratégia demonstra a sabedoria de "agir conforme as circunstâncias":

- Em mercados de tendência, comporta-se como um agressivo seguidor de tendência

- Em mercados laterais, comporta-se como um trader conservador de range

Esse tipo de pensamento tem importante valor inspirador para desenvolvedores de estratégias: devemos dotar as estratégias de capacidade de "percepção de mercado", em vez de executar cegamente uma lógica fixa.

Por fim, é importante enfatizar que nenhuma estratégia é universal. Embora essa estratégia de média de degraus seja teoricamente elegante, na prática ainda precisa ser ajustada conforme o ambiente de mercado específico e a tolerância ao risco pessoal. Lembre-se: a melhor estratégia é sempre aquela que mais se adequa a você.

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1