🎯 Que estratégia divina é essa? 20 indicadores trabalhando juntos!

Sabia que essa estratégia é como ter um assistente de IA super inteligente para suas negociações? Ela monitora simultaneamente 20 sinais diferentes do mercado, e só dá uma recomendação de negociação quando a maioria dos indicadores diz "pode ir". É como comprar uma casa: você avalia localização, preço, planta, transporte... só fecha negócio quando tudo está satisfatório!

Destaque! Esta não é uma estratégia comum de um único indicador, mas sim um "Sistema de Ressonância Multidimensional". Imagine: se apenas um amigo disser que uma ação é boa, você pode ficar na dúvida; mas se 20 amigos especialistas disserem que é boa, você não fica muito mais confiante?

📊 Grande Revelação do Arsenal Principal

Os Três Mosqueteiros da Identificação de Tendência 🗡️

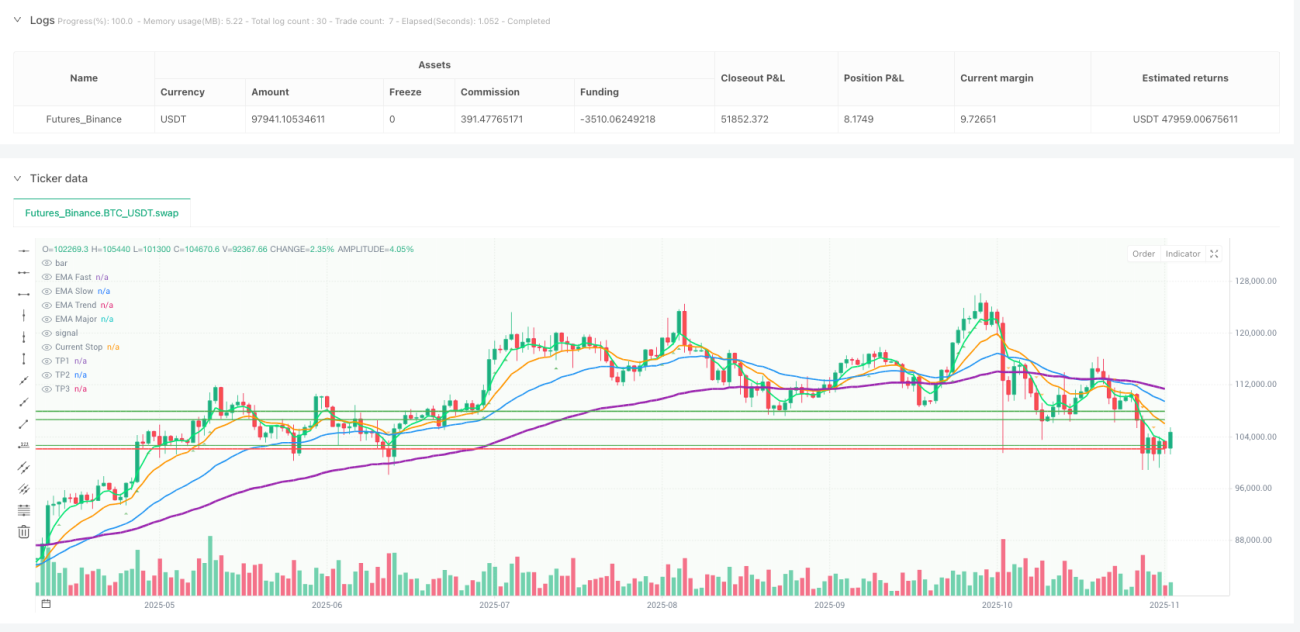

- EMA Rápida (5) vs EMA Lenta (13): Capturam as viradas de tendência de curto prazo

- EMA de Filtro de Tendência (34): Confirmam a direção de médio prazo

- EMA de Tendência Principal (89): Definem a direção geral, sem se deixar enganar por pequenas flutuações

Análise de Múltiplos Timeframes ⏰

Essa função é fantástica! A estratégia analisa simultaneamente as tendências de 1 hora e 4 horas, como quando você dirige: olha tanto a estrada à frente quanto a rota geral no navegador. Evita aquela situação embaraçosa de "o timeframe menor está otimista, mas o maior está pessimista"!

Gerenciamento de Risco Inteligente 🛡️

- Ajuste Dinâmico de Posição: Altera automaticamente o tamanho da aposta com base na volatilidade do mercado

- Realização Parcial de Lucro: Sem ganância, realiza uma parte quando está bom

- Stop Móvel: Uma ferramenta poderosa para proteger os lucros

🔥 A Lógica de Negociação com 20 Seguros

Para sinal de COMPRA, é necessário:

- Tendência de alta: Todas as EMAs estão em alinhamento de alta

- Momentum suficiente: RSI, MACD, RSI Estocástico dão sinal verde

- Confirmação de volume: Alta com volume é uma alta verdadeira

- Estrutura de mercado saudável: Máximas cada vez mais altas

- Suporte de liquidez: Níveis de suporte chave intactos

Para sinal de VENDA, é exatamente o oposto!

Guia para Evitar Armadilhas ⚠️: A estratégia também tem uma "Detecção de Compressão das Bandas de Bollinger". Quando o mercado está muito calmo, ela pausa as negociações para evitar leva-e-traz em mercados laterais!

💰 O Segredo para Maximizar os Lucros

Estratégia de Realização Parcial de Lucro 📈

- Primeira realização: Vende 30% da posição quando o risco-retorno é de 2x

- Segunda realização: Vende mais 40% quando atinge 3.5x

- Posição restante: Protegida com stop móvel, deixando o lucro correr

Upgrade do Stop Inteligente 🎯

Após atingir 2.5x de lucro, o stop é automaticamente movido para o preço de custo, garantindo que essa negociação pelo menos não dê prejuízo. É como comprar um seguro para o seu lucro!

Stop Móvel Dinâmico 🏃♂️

Quando o lucro atinge um certo nível, o stop segue o preço como uma sombra, protegendo o lucro mas deixando espaço para a alta continuar.

🚀 Por que essa estratégia é tão poderosa?

- Cobertura Completa: Análise técnica, gestão de capital e controle de risco, nenhum item fica de fora

- Filtro Inteligente: 20 condições que selecionam rigorosamente, aumentando muito a taxa de sucesso

- Alta Adaptabilidade: Análise de múltiplos timeframes, adequada para diferentes ambientes de mercado

- Design Humanizado: Execução automatizada, evitando negociações emocionais

Essa estratégia é como colocar uma equipe de traders experientes dentro de um código, trabalhando 24 horas por dia sem parar para encontrar as melhores oportunidades de negociação para você!

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1