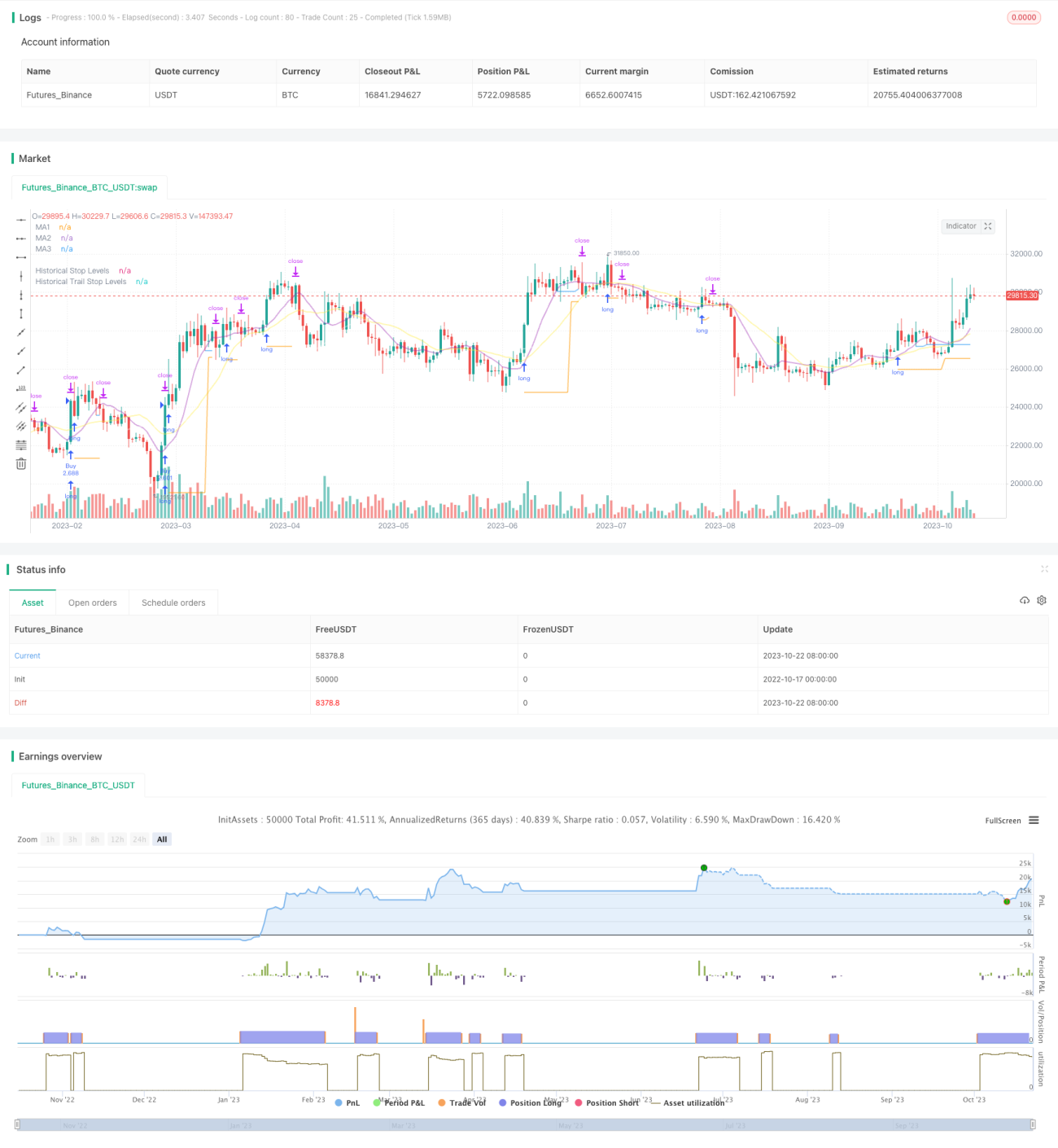

Стратегия прорыва с трейлинг-стопом V2

Обзор

Данная стратегия объединяет преимущества стратегии прорыва и стратегии трейлинг-стопа по тренду, направлена на捕捉 сигналов пробоя уровней поддержки и сопротивления на длинных таймфреймах, одновременно используя скользящие средние для трейлинг-стопа, что позволяет получать прибыль в направлении долгосрочного тренда, контролируя риски.

Принцип стратегии

-

Сначала стратегия рассчитывает несколько групп скользящих средних с разными параметрами, которые используются для определения тренда, уровней поддержки/сопротивления и трейлинг-стопа.

-

Затем находятся максимальные и минимальные точки за указанный период, которые служат зонами поддержки/сопротивления для входа. Когда цена пробивает эти уровни, генерируется сигнал.

-

Стратегия использует пробой максимума как сигнал на покупку (long), а пробой минимума — как сигнал на продажу (short).

-

После входа позиция удерживается со стоп-лоссом на уровне пробойного минимума.

-

Когда позиция переходит в прибыль, стоп-лосс заменяется на трейлинг по скользящей средней. Если цена пробивает скользящую среднюю вниз, стоп устанавливается на минимуме этой свечи.

-

Таким образом фиксируется прибыль, при этом позиция имеет достаточное пространство для следования за трендом.

-

Стратегия также использует средний истинный диапазон (ATR), чтобы гарантировать, что вход происходит только при прорыве в подходящем диапазоне, избегая чрезмерно растянутых пробоев.

Анализ преимуществ стратегии

-

Сочетает преимущества стратегии прорыва и стратегии трейлинг-стопа по тренду.

-

Позволяет входить в прорывы в направлении долгосрочного тренда, увеличивая вероятность прибыли.

-

Стоп-стратегия как защищает позицию, так и даёт ей достаточно пространства для движения.

-

Включение фильтра волатильности позволяет избежать неблагоприятных прорывов с чрезмерным растяжением.

-

Автоматизированная торговля, подходит для частичного копирования сделок.

-

Возможность настройки скользящих средних с разными периодами.

-

Гибкая настройка метода трейлинг-стопа.

Анализ рисков стратегии

-

Стратегия прорыва подвержена риску ложных пробоев. Можно ослабить требования к подтверждению пробоя.

-

Для генерации сигналов прорыва требуется достаточная волатильность; на неустойчивых рынках стратегия может быть неэффективна.

-

Некоторые пробои могут быть слишком короткими, чтобы их можно было захватить. Можно снизить таймфрейм для поиска большего числа возможностей.

-

Трейлинг-стоп может слишком часто срабатывать на колебательных рынках. Можно увеличить расстояние стопа.

-

Фильтр волатильности может пропустить часть возможностей. Можно снизить параметры фильтра.

Направления оптимизации стратегии

-

Тестирование различных комбинаций параметров скользящих средних для поиска оптимальных.

-

Тестирование различных механизмов подтверждения пробоя, таких как каналы, формации свечей и т.д.

-

Попробовать различные методы трейлинг-стопа для поиска наилучшего стопа.

-

Оптимизация стратегии управления капиталом, например, использование позиционного скоринга.

-

Включение статистических технических индикаторов для фильтрации, повышение точности фильтрации.

-

Тестирование стратегии на разных инструментах.

-

Внедрение алгоритмов машинного обучения для улучшения эффективности стратегии.

Заключение

Данная стратегия объединяет идеи прорыва и трейлинг-стопа по тренду. При правильном определении долгосрочного тренда она позволяет оптимизировать пространство для прибыли. Ключевым моментом является поиск оптимальной комбинации параметров в сочетании с хорошей стратегией управления капиталом, чтобы воспользоваться долгосрочными возможностями и одновременно контролировать риски. Данная стратегия может стать достаточно надёжной долгосрочной трендовой стратегией после дальнейшей оптимизации.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1