Стратегия двусторонней торговли с длинными и короткими позициями на основе двухполосного осциллятора RSI

Обзор

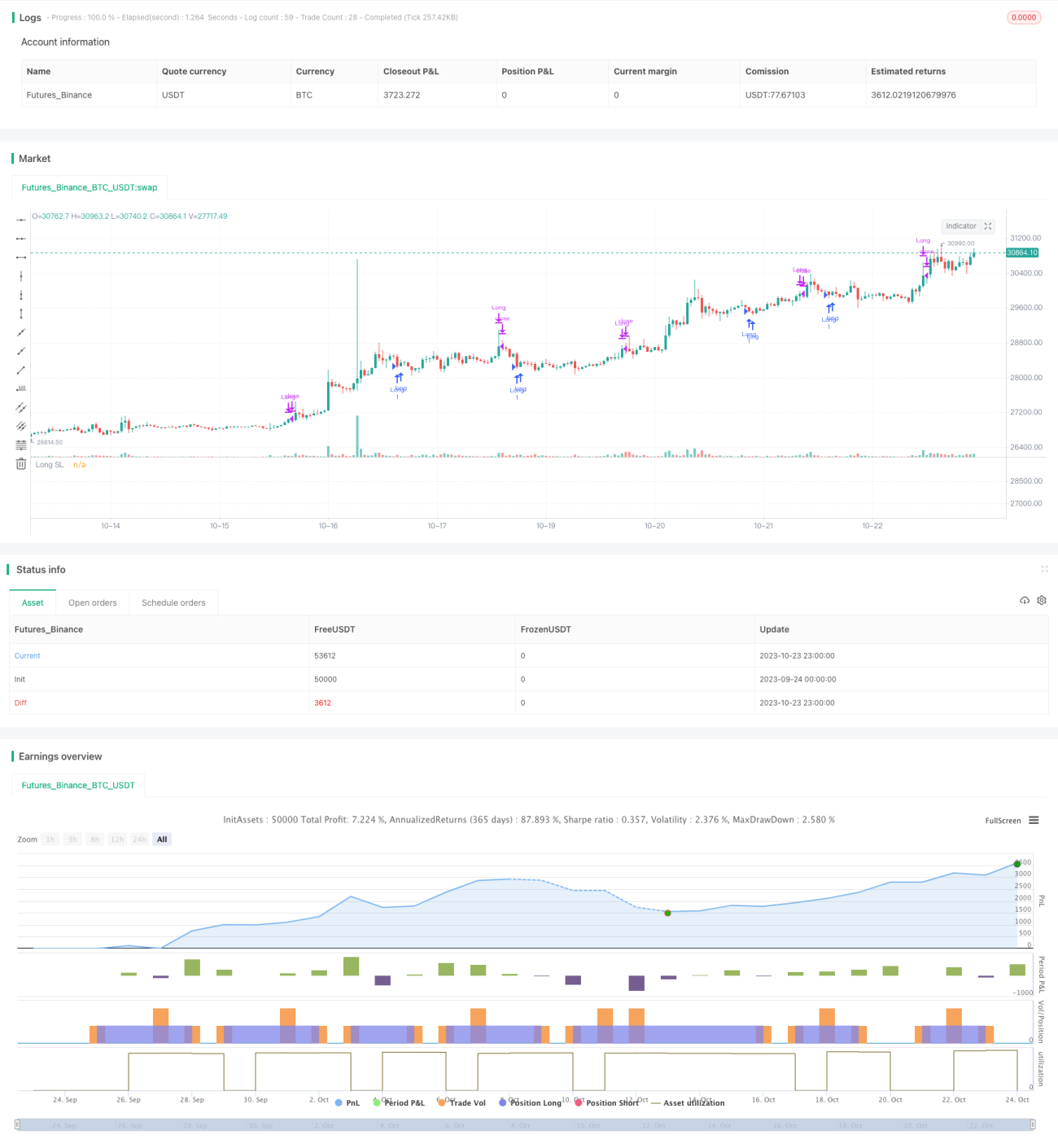

Стратегия двусторонней торговли с использованием RSI и двойных полос основана на применении индикатора RSI для открытия позиций как в длинную, так и в короткую сторону. Стратегия использует принципы перекупленности/перепроданности RSI в сочетании с настройками двойных полос и сигналами скользящих средних для эффективного открытия и закрытия позиций.

Принцип стратегии

Основой стратегии является принятие торговых решений на основе принципов перекупленности/перепроданности индикатора RSI. Сначала вычисляется значение RSI (vrsi), а также верхняя полоса (sn) и нижняя полоса (ln) двойного канала. Когда RSI пересекает нижнюю полосу ln вниз, генерируется сигнал на покупку (лонг). Когда RSI пересекает верхнюю полосу sn вверх, генерируется сигнал на продажу (шорт).

Стратегия также отслеживает изменения свечей (рост/падение), дополнительно генерируя сигналы на покупку и продажу. Конкретно, когда свеча пробивает вверх, формируется сигнал на покупку (longLogic), а когда свеча пробивает вниз — сигнал на продажу (shortLogic). Кроме того, предусмотрены параметры-переключатели, позволяющие торговать только в длинную, только в короткую или инвертировать сигналы.

После генерации сигналов на покупку/продажу стратегия подсчитывает количество сигналов и контролирует число открываемых позиций. Настройки позволяют задать различные правила добавления позиций (мартингейл). Условия закрытия позиций включают фиксацию прибыли, стоп-лосс, трейлинг-стоп и другие, с возможностью установки различных процентов тейк-профита и стоп-лосса.

В целом, стратегия комплексно использует RSI, пересечения скользящих средних, статистическое добавление позиций, тейк-профит и стоп-лосс для автоматической двусторонней торговли.

Преимущества стратегии

- Использует принцип перекупленности/перепроданности RSI для открытия позиций в лонг и шорт в подходящих точках.

- Двойные полосы помогают избежать ложных сигналов. Верхняя полоса предотвращает преждевременное закрытие длинных позиций, нижняя — преждевременное закрытие коротких.

- Сигналы на основе скользящих средних отфильтровывают ложные пробои. Сигнал генерируется только при пробое ценой скользящей средней, что уменьшает количество ложных срабатываний.

- Контроль количества сигналов и числа добавлений позиций для управления рисками.

- Возможность настройки процентов тейк-профита и стоп-лосса, контролируемый профит/риск.

- Трейлинг-стоп для дальнейшей фиксации прибыли.

- Возможность торговать только в лонг, только в шорт или инвертировать сигналы, адаптируясь к разным рыночным условиям.

- Автоматизированная торговая система снижает затраты на ручное управление.

Риски стратегии

- Риск неудачного разворота RSI. Даже при входе в зоны перекупленности/перепроданности разворот может не произойти.

- Фиксированные уровни тейк-профита и стоп-лосса могут привести к преждевременному закрытию или попаданию в ловушку при неправильной настройке.

- Зависимость от технических индикаторов несёт риск неправильного подбора параметров, что влияет на эффективность стратегии.

- Одновременное срабатывание нескольких условий может привести к пропуску сигналов.

- Риск ошибок в автоматизированной системе.

Для минимизации этих рисков можно оптимизировать параметры, настроить стратегию стоп-лосса/тейк-профита, добавить фильтр по ликвидности, улучшить логику генерации сигналов, усилить мониторинг ошибок.

Направления оптимизации

- Тестирование различных временных периодов и параметров RSI.

- Тестирование разных настроек процентов тейк-профита и стоп-лосса.

- Добавление фильтра по объёму или доходности для избежания низколиквидных инструментов.

- Оптимизация логики генерации сигналов, улучшение способа пересечения скользящих средних.

- Проведение многопериодного бэктестинга для проверки стабильности.

- Рассмотрение добавления других индикаторов для улучшения сигналов.

- Внедрение стратегии управления позициями (мани-менеджмент).

- Усиление мониторинга аномальных ошибок.

- Оптимизация алгоритма трейлинг-стопа.

- Рассмотрение применения машинного обучения для улучшения стратегии.

Заключение

Стратегия двусторонней торговли с использованием RSI и двойных полос (RSI双轨震荡线长短双向交易策略) объединяет индикатор RSI, статистическое открытие позиций и стоп-лосс для автоматической двусторонней торговли. Стратегия обладает высокой степенью настройки: пользователи могут адаптировать параметры под различные рыночные условия. В то же время стратегия имеет потенциал для улучшения путём оптимизации параметров, управления рисками, логики генерации сигналов и т.д., что сделает её более стабильной и надёжной. В целом, эта стратегия представляет собой достаточно эффективное решение для количественной торговли.

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1