Адаптивная стратегия тейк-профита и стоп-лосса на основе двойного таймфрейма и индикатора импульса

Обзор

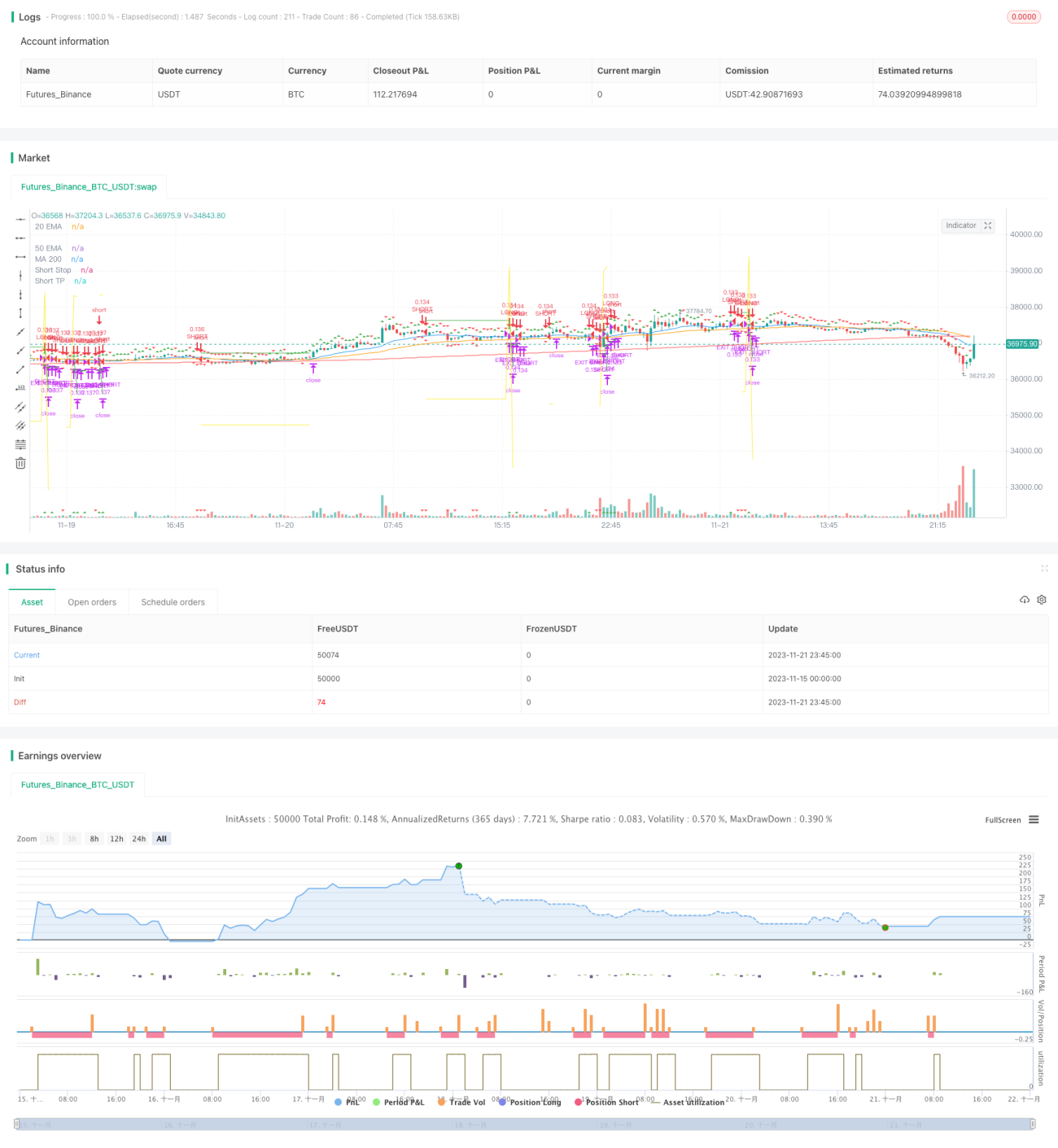

Данная стратегия использует комбинацию двух таймфреймов и импульсных индикаторов для реализации адаптивного тейк-профита и стоп-лосса. Основной таймфрейм отслеживает направление тренда, а вспомогательный используется для подтверждения сигналов. Когда направления обоих таймфреймов совпадают, генерируется торговый сигнал. После входа в позицию применяется прогрессивное обновление уровней тейк-профита и стоп-лосса.

Принцип стратегии

-

На основном таймфрейме используется линейный регрессионный индикатор Squeeze Momentum (SQM) для определения тренда, а на вспомогательном — комбинация EMA того же индикатора для фильтрации ложных сигналов.

-

Когда на основном графике SQM пробивает вверх, а на вспомогательном также растёт — открывается длинная позиция; когда на основном графике SQM пробивает вниз, а на вспомогательном также идёт вниз — открывается короткая позиция.

-

После входа в позицию устанавливаются начальные уровни тейк-профита и стоп-лосса на основе входных параметров. При достижении ценой уровня тейк-профита эти уровни обновляются: тейк-профит увеличивается на заданный процент, а стоп-лосс уменьшается, реализуя прогрессивный выход.

Преимущества стратегии

-

Двойной таймфрейм фильтрует ложные сигналы, обеспечивая их точность.

-

Индикатор SQM определяет направление тренда, избегая влияния рыночного шума.

-

Адаптивный механизм тейк-профита и стоп-лосса позволяет максимально фиксировать прибыль и эффективно контролировать риски.

Анализ рисков

-

Неправильная настройка параметров индикатора SQM может привести к пропуску точек разворота тренда и к убыткам.

-

Неудачный выбор таймфрейма для вспомогательного графика не позволит эффективно отфильтровать шум, что приведёт к ошибочным сделкам.

-

Слишком широкий диапазон стоп-лосса может привести к значительным потерям по одной сделке.

Направления оптимизации

-

Параметры индикатора SQM необходимо корректировать под разные рынки для обеспечения его чувствительности.

-

Таймфрейм вспомогательного графика также следует протестировать на различных периодах, чтобы определить, какой из них даёт наилучшую фильтрацию.

-

Вместо фиксированного значения стоп-лосса можно установить диапазон волатильности, чтобы настраивать его в зависимости от рыночных колебаний.

Заключение

В целом стратегия очень практична: два таймфрейма в сочетании с импульсным индикатором определяют тренд, а адаптивные тейк-профит и стоп-лосс обеспечивают стабильную прибыль. Оптимизация параметров SQM, периода вспомогательного графика и величины стоп-лосса позволит улучшить результаты стратегии, что делает её достойной применения и доработки в реальной торговле.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1