Торговая стратегия на основе скользящей средней EMA

Обзор

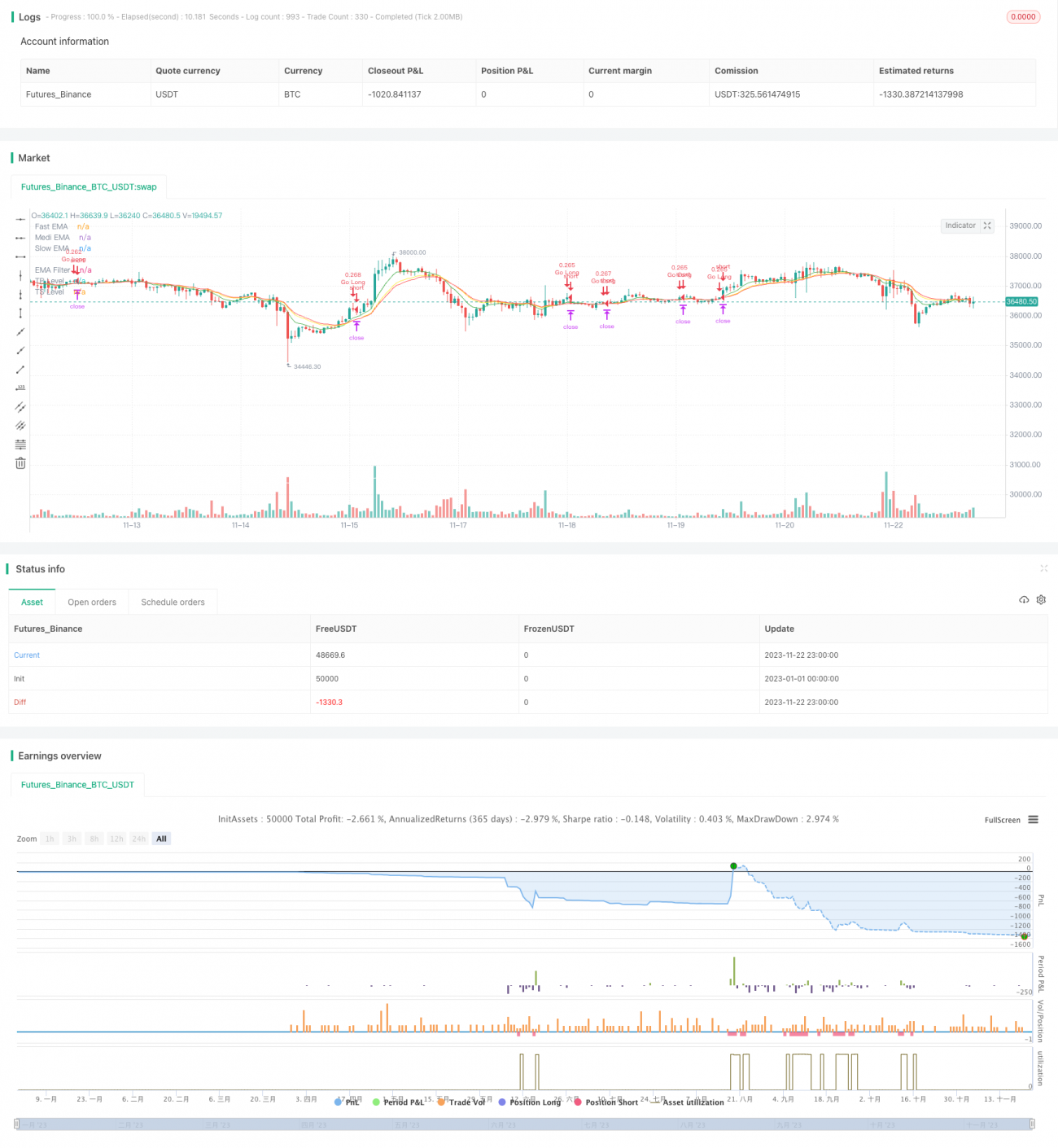

Данная стратегия использует 4 скользящие средние EMA с разными периодами и формирует торговые сигналы на основе их взаимного расположения, напоминая трёхцветный светофор (красный, жёлтый, зелёный). Поэтому стратегия называется «Светофорная торговая стратегия». Она комплексно оценивает рынок с точки зрения тренда и разворота, повышая точность торговых решений.

Принцип стратегии

-

Устанавливаются 3 скользящие средние EMA: быстрая (период 8), средняя (период 14) и медленная (период 16), а также одна длинная EMA (период 100) в качестве фильтра.

-

На основе взаимного расположения трёх быстрых/средних/медленных EMA и их пересечений с фильтром определяются моменты для открытия длинных и коротких позиций:

-

Когда быстрая EMA пересекает среднюю EMA снизу вверх или средняя EMA пересекает медленную EMA снизу вверх, формируется сигнал на открытие длинной позиции.

-

Когда средняя EMA пересекает быструю EMA сверху вниз, формируется сигнал на закрытие длинной позиции.

-

Когда быстрая EMA пересекает среднюю EMA сверху вниз или средняя EMA пересекает медленную EMA сверху вниз, формируется сигнал на открытие короткой позиции.

-

Когда средняя EMA пересекает быструю EMA снизу вверх, формируется сигнал на закрытие короткой позиции.

-

-

Порядок расположения трёх EMA (быстрой, средней, медленной) позволяет определить направление и силу тренда, а пересечения с фильтром указывают на точки разворота. Таким образом достигается сочетание следования за трендом и ловли разворотов.

Преимущества стратегии

Стратегия объединяет достоинства трейд-следования и разворотной торговли, что позволяет лучше использовать рыночные возможности. Основные преимущества:

- Использование нескольких групп EMA повышает точность оценки и снижает количество ложных сигналов.

- Гибкие условия для открытия длинных и коротких позиций позволяют не упускать торговые возможности.

- Комплексное применение скользящих средних разных периодов обеспечивает всесторонний анализ.

- Возможность настраивать условия тейк-профита и стоп-лосса обеспечивает надёжный контроль рисков.

После оптимизации параметров стратегия может адаптироваться к большему числу инструментов и демонстрирует высокую прибыльность и стабильность на исторических данных.

Анализ рисков

Основные риски стратегии:

- При хаотичном расположении нескольких EMA возрастает сложность принятия решений, что может вызывать задержки в торговле.

- Невозможность эффективно отфильтровать ложные сигналы при аномальных рыночных колебаниях, что может приводить к убыткам, например, в период высокой волатильности.

- При неправильной настройке параметров условия тейк-профита и стоп-лосса могут оказаться слишком мягкими или жёсткими, что приведёт к упущенной прибыли или чрезмерным убыткам.

Рекомендуется повышать стабильность стратегии и контролировать риски за счёт оптимизации параметров, установки уровней стоп-лосса и осторожного управления.

Направления оптимизации

Основные направления оптимизации стратегии:

- Настройка периодов EMA для адаптации к большему числу инструментов.

- Добавление других индикаторов-фильтров, таких как MACD, полосы Боллинджера и т.д., для повышения точности сигналов.

- Оптимизация соотношения тейк-профита и стоп-лосса для достижения наилучшего баланса между риском и доходностью.

- Внедрение адаптивного стоп-лосса, например, на основе ATR, для дальнейшего снижения рисков снижения.

Путём многопараметрических настроек и внедрения методов контроля рисков можно постоянно улучшать стабильность и прибыльность стратегии.

Заключение

Данная светофорная торговая стратегия объединяет трендовое следование и разворотный анализ, использует 4 группы EMA для формирования торговых сигналов. Благодаря оптимизации параметров она адаптируется ко многим инструментам и демонстрирует высокую прибыльность на исторических тестах. В дальнейшем, за счёт усиления контроля рисков и добавления дополнительных индикаторов, стратегия может стать стабильной и эффективной системой для алгоритмической торговли.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1