Количественная стратегия «Ежедневное переплетение линии отвлечения»

Обзор

Количественная стратегия «Скользящая линия отвлечения внимания, обернутая день за днем» представляет собой краткосрочную количественную торговую стратегию, основанную на скользящих средних и индикаторах максимальной и минимальной цены. Она использует стрелки EXIT гибридного индикатора SSL для определения точек входа и выхода, фильтрует сигналы с помощью индикатора QQE и рассчитывает уровни стоп-лосса и позиции для частичного добавления с помощью индикатора ATR. Стратегия подходит для инвесторов, чувствительных к рыночной волатильности и строго контролирующих риски.

Принцип стратегии

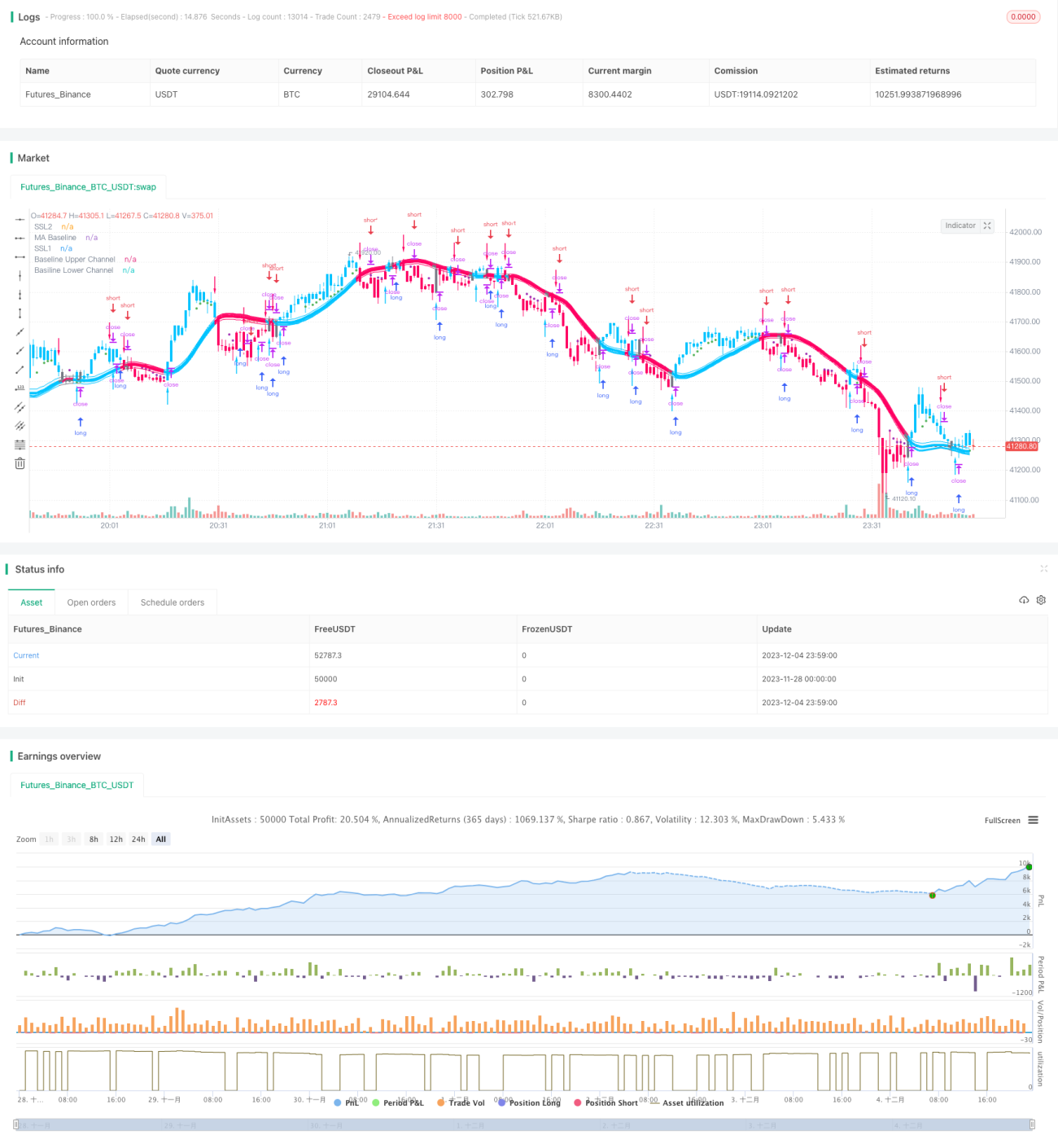

Стратегия использует стрелки EXIT гибридного индикатора SSL для определения точек входа. Стрелка EXIT имеет верхнюю точку (EXIT High) и нижнюю точку (EXIT Low). Когда цена закрытия пересекает EXIT High сверху вниз, генерируется сигнал на продажу; когда цена закрытия пересекает EXIT Low снизу вверх, генерируется сигнал на покупку.

Для повышения надежности сигналов в стратегию введен индикатор QQE в качестве вспомогательного фильтра. Сигналы, генерируемые стрелками EXIT, исполняются только при совпадении направления с индикатором QQE.

Для контроля риска стратегия использует множитель ATR для расчета уровней стоп-лосса и частичного добавления позиций. Стоп-лосс для короткой позиции: цена закрытия + ATR × 1,8. Стоп-лосс для длинной позиции: цена закрытия – ATR × 1,8. Добавление позиций происходит тремя частями, каждая часть составляет 10% от начального капитала. Уровни добавления: цена закрытия – ATR × 0,1, цена закрытия – ATR × 0,3, цена закрытия – ATR × 0,7.

Для каждой части добавления установлен отдельный стоп-лосс. Первая часть размером 20% от суммы закрывается при достижении стоп-уровня, остальные позиции удерживаются.

Преимущества стратегии

- Фиксация прибыли по стрелкам EXIT и своевременное ограничение убытков для эффективного контроля риска.

- Фильтрация сигналов с помощью QQE повышает точность сигналов.

- Использование ATR для расчета стоп-лосса и уровней добавления в зависимости от рыночной волатильности обеспечивает более точный риск-менеджмент.

- Частичное добавление позиций позволяет в полной мере использовать тренд для получения прибыли.

Риски стратегии

- Частичное закрытие прибыльной позиции может привести к тому, что оставшаяся часть позиции продолжит нести убытки. Возможно применение общего тейк-профита или тейк-профита на основе фундаментальных показателей самого актива.

- Чувствительность стрелок EXIT и индикатора QQE к рыночной волатильности может быть разной, что приведет к конфликтующим сигналам. Следует настроить параметры для уменьшения конфликтов.

- Слишком агрессивное добавление позиций может привести к покупке на пике и продаже на дне. Необходимо оценивать ситуацию и снижать уровень плеча.

Направления оптимизации

- Комбинирование с фундаментальными индикаторами самого актива для тейк-профита, например, установка разумных уровней тейк-профита на основе отношения цены к балансовой стоимости, коэффициента P/E, дивидендной доходности и т.д.

- Настройка параметров индикатора QQE для согласования сигналов со стрелками EXIT.

- Снижение доли добавления позиций в зависимости от рыночной активности, уменьшение добавления в боковом тренде.

- Тестирование наилучших комбинаций параметров на основе показателей максимальной просадки, коэффициента прибыли к убытку и т.д.

Заключение

Данная стратегия использует стрелки EXIT гибридного индикатора SSL в качестве основного сигнала, а индикаторы QQE и ATR — для фильтрации и стоп-лосса. Увеличение прибыли достигается за счет частичного добавления позиций. Это краткосрочная количественная стратегия, подходящая для отслеживания краткосрочных рыночных трендов. Стратегия обладает способностью контролировать просадки и риски, но также требует внимания к таким рискам, как конфликты сигналов и покупка на пике с продажей на дне. Если дополнить стратегию методами тейк-профита на основе фундаментальных показателей активов и более тщательно оценивать рыночные колебания при корректировке доли добавления, потенциал прибыли стратегии значительно возрастет.

- 1